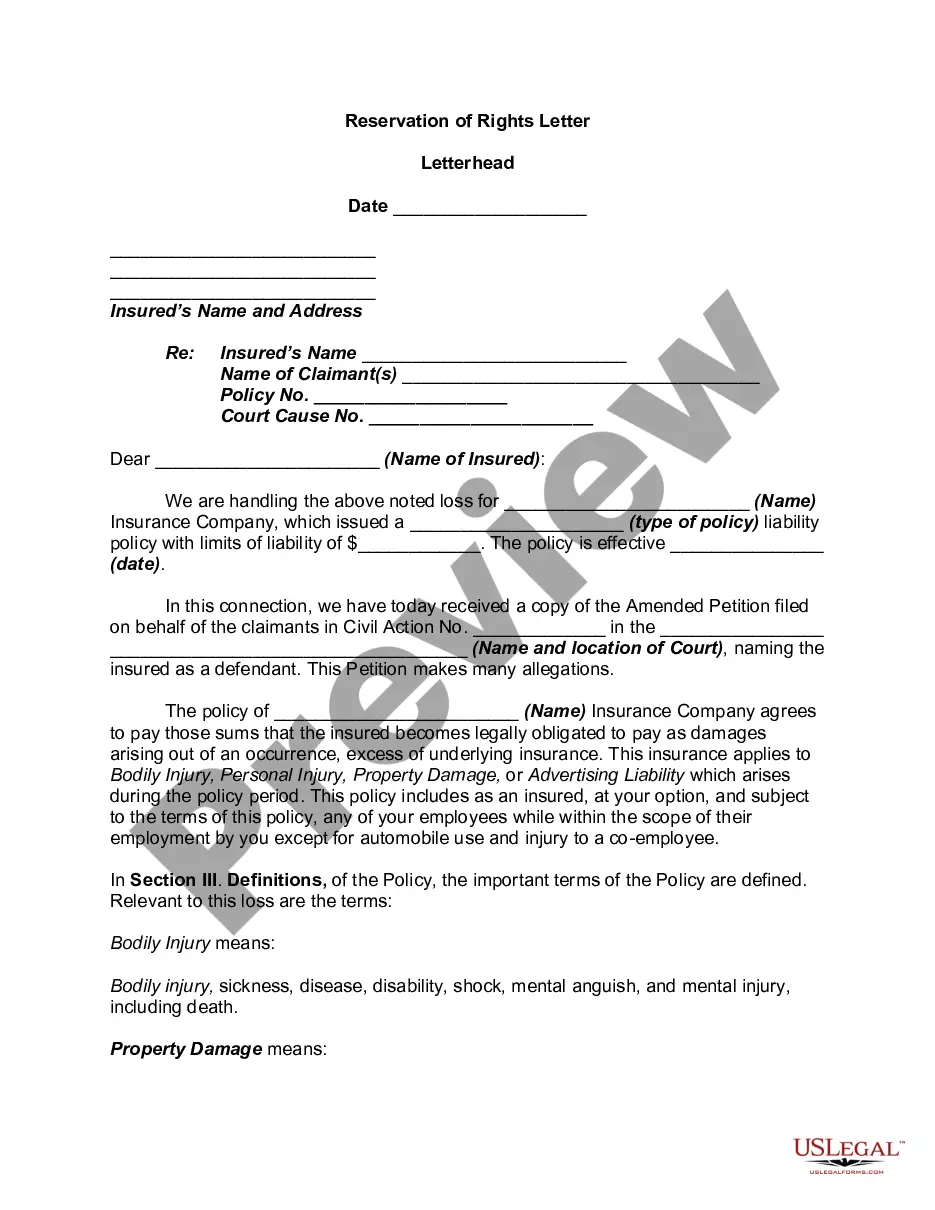

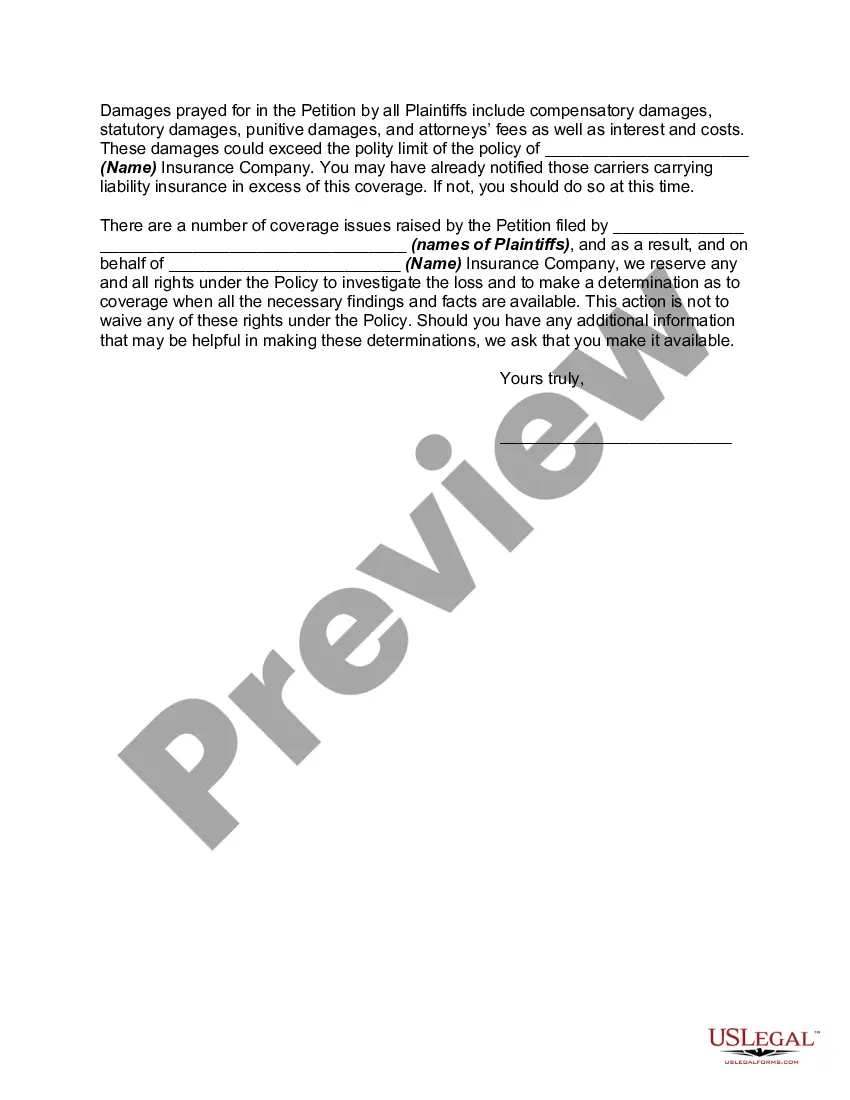

A reservation of rights defense is a means by which a liability insurance carrier agrees to protect and defend its insured against a claim or suit while reserving the right to further evaluate and perhaps even deny coverage for some or all of the claim. It is most commonly used when the claim or suit contains both covered and non-covered allegations, when the allegations are in excess of policy limits, or when the insurer is still investigating its defense and coverage obligations. For the insurer, a reservation of rights provides the flexibility to satisfy its duty to defend without committing to coverage. For the business owner who ultimately may have to pay for an adverse judgment, it requires careful monitoring and attention.

Wisconsin Reservation of Rights Letter is a legal document that an insurance company sends to an insured party to inform them that certain policy provisions may potentially exclude coverage for a specific claim or situation. It serves as a precautionary measure for the insurance company to retain their rights in case the claim falls outside the policy's terms and conditions. This letter outlines the specific policy provisions being invoked and provides an explanation of the potential reasons for coverage denial. In Wisconsin, different types of Reservation of Rights Letters may be issued depending on the circumstances. Some common types include: 1. General Reservation of Rights Letter: This letter notifies the insured party that the insurance company reserves its rights under the policy, generally due to policy exclusions, limitations, or possibly insufficient information regarding the claim. 2. Reservation of Rights for Late Notice: This letter is sent when the insured party failed to promptly notify the insurance company about a claim or occurrence that may be covered. It allows the insurance company to investigate the situation while reserving the right to deny coverage if the delay prejudiced their ability to investigate or evaluate the claim. 3. Reservation of Rights for Misrepresentation or Fraud: If the insurance company discovers that the insured party has misrepresented facts or committed fraud in relation to the policy or claim, this letter is sent. It notifies the insured party that coverage might be denied due to the misrepresentation or fraud committed. 4. Reservation of Rights due to Conflict of Interest: In some cases, an insurance company may have a conflict of interest when representing multiple insured parties involved in the same claim. This letter informs the insured party about the conflict and states that the insurance company will continue to handle the claim but reserves its rights to take actions that may not be in the insured party's best interest. It is important for the insured party to carefully review the Reservation of Rights Letter to understand the potential impact on their coverage and to seek legal advice if needed. The insured party can respond to the letter to address any concerns or present additional information to support their claim.