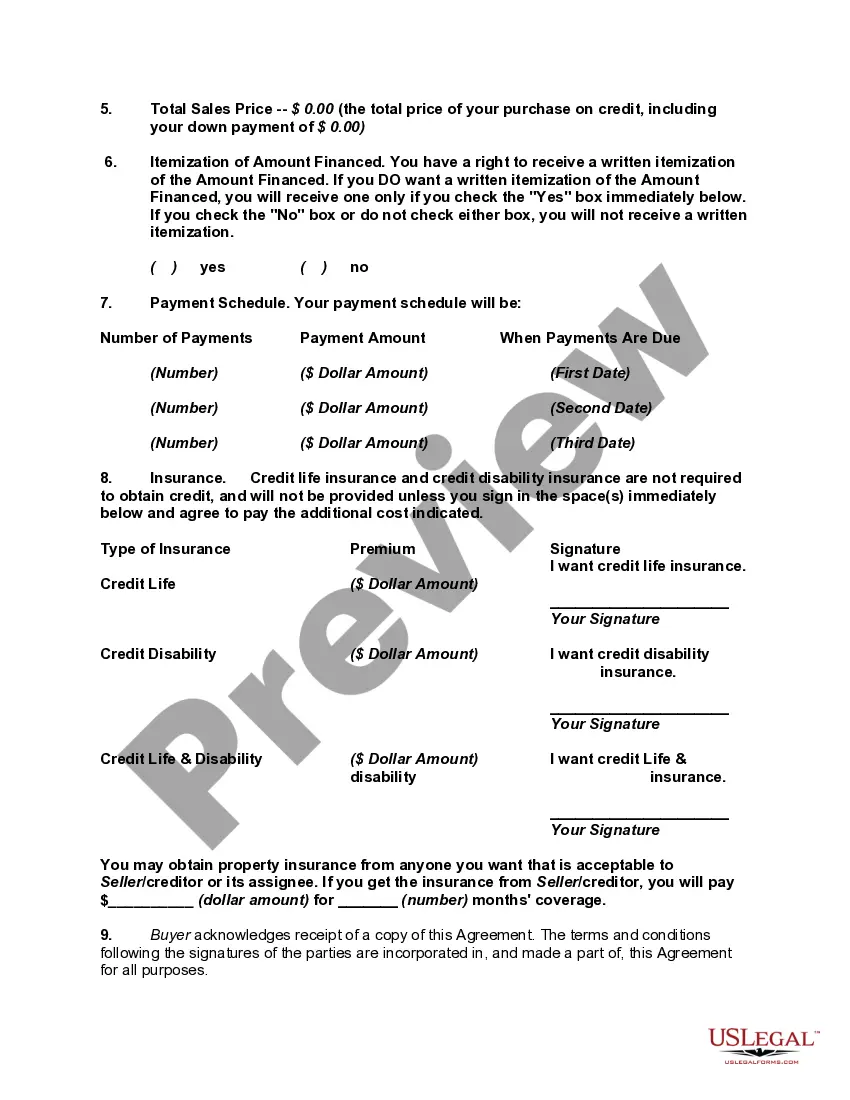

Disclosure of credit terms should have the content and form required under the federal Truth in Lending Act (15 U.S.C.A. §§ 1601 et seq.) and applicable regulations (Regulation Z, 12 C.F.R. § 226), and under state consumer credit laws to the extent that they differ from the federal Act. In connection with specified installment sales and other consumer credit transactions, these enactments require written disclosure and advice as to finance charges, annual percentage rates and other matters relating to credit. Under the federal Act, the disclosures may be set forth in the contract document itself or in a separate statement or statements.

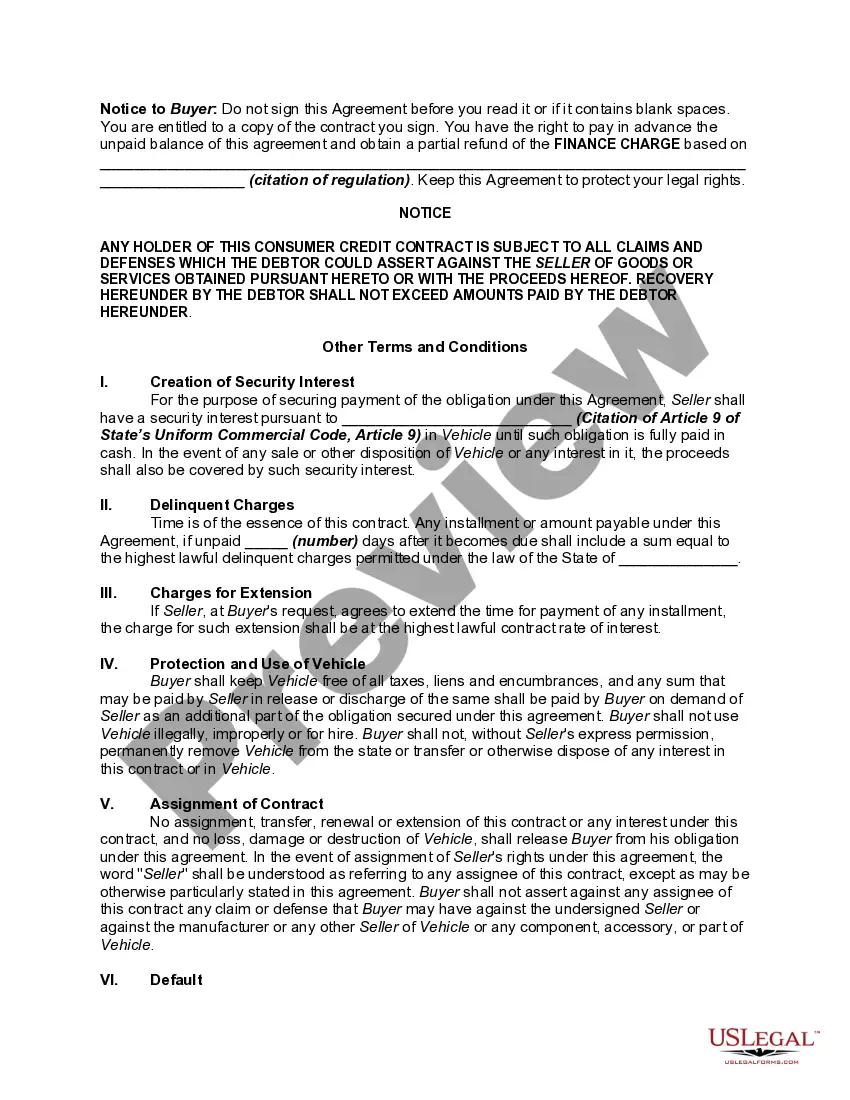

A federal notice regarding preservation of the consumer's claims and defenses is required on all consumer credit contracts by Federal Trade Commission regulation. 16 C.F.R. § 433.2. The notice must appear in 10-point bold type or print and must be worded as set forth in the above form.

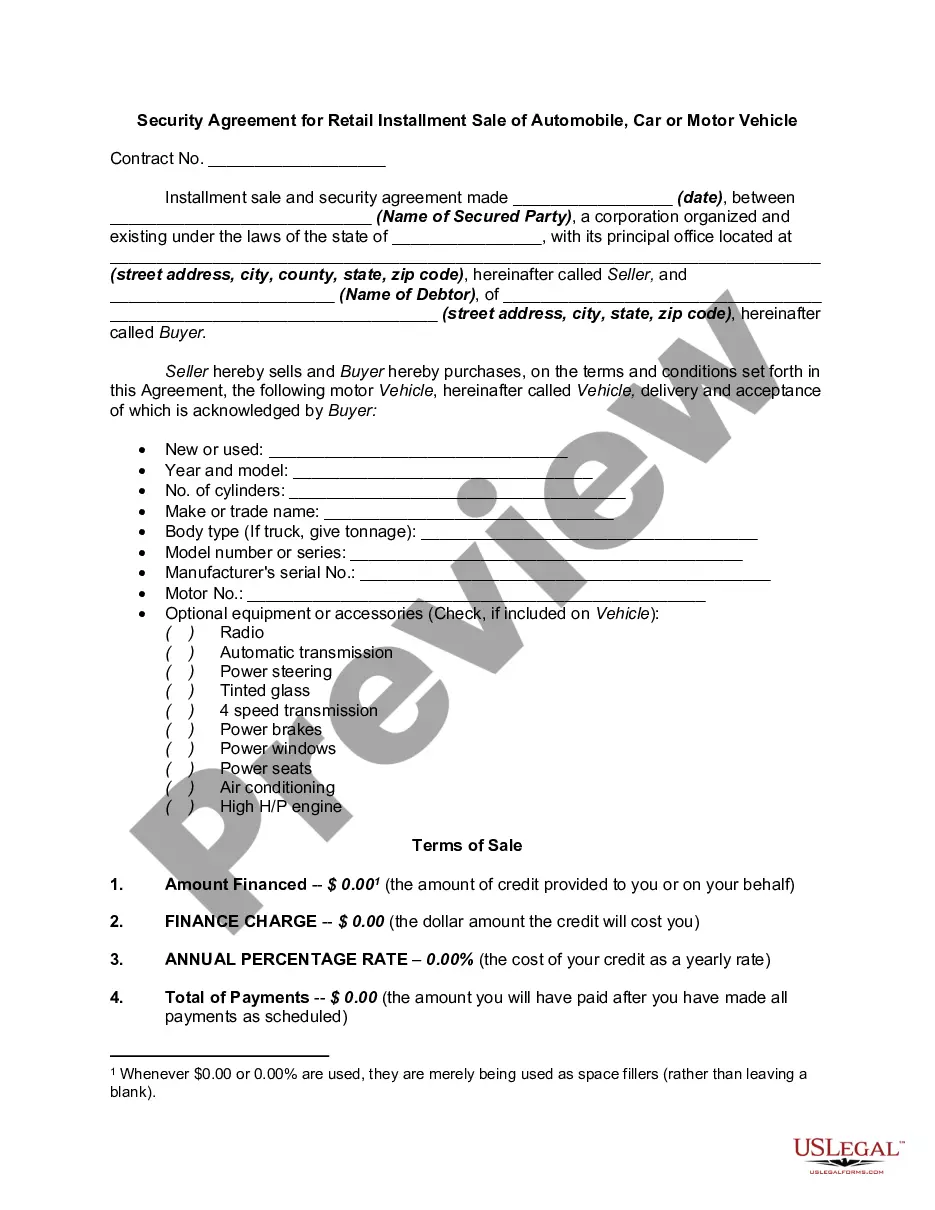

The Wisconsin Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle is a legally binding document that outlines the terms and conditions of financing a vehicle purchase in the state of Wisconsin. This agreement serves as a security measure for the lender, ensuring that they have a legal claim to the vehicle until the borrower completes payment obligations. Keywords: Wisconsin Security Agreement, Retail Installment Sale, Automobile, Car, Motor Vehicle, Financing, Lender, Borrower, Payment Obligations. There are different types of Wisconsin Security Agreements for Retail Installment Sale of Automobile, Car, or Motor Vehicle, depending on the specific needs and circumstances of the transaction. Below are some common variations: 1. Traditional Security Agreement: This type of security agreement is typically used for standard vehicle purchase financing. It defines the terms, repayment schedule, and interest rates associated with the loan, as well as the consequences of default or non-payment. 2. Balloon Payment Security Agreement: In some cases, borrowers may opt for a balloon payment arrangement, where smaller monthly installments are made throughout the loan term, with a large final payment at the end. This type of agreement includes specific provisions for the balloon payment and corresponding terms. 3. Adjustable-Rate Security Agreement: An adjustable-rate security agreement provides the lender with the option to adjust the interest rate periodically. This allows the interest rate to fluctuate based on an agreed-upon index, such as the prime rate or the treasury bill rate. 4. Subprime Security Agreement: Subprime security agreements are designed for borrowers with low credit scores or poor credit histories. These agreements often come with higher interest rates and stricter terms to mitigate the increased lending risk. 5. Joint Security Agreement: A joint security agreement is utilized when multiple individuals or entities are involved in financing the vehicle purchase. This agreement clarifies the responsibilities of each party involved and establishes the order of priority in case of default or repossession. Irrespective of the type, a Wisconsin Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle sets out the rights and obligations of both the lender and the borrower. It serves as a crucial legal document that protects the interests of all parties involved in the financing arrangement, ensuring transparency and compliance with Wisconsin state laws.The Wisconsin Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle is a legally binding document that outlines the terms and conditions of financing a vehicle purchase in the state of Wisconsin. This agreement serves as a security measure for the lender, ensuring that they have a legal claim to the vehicle until the borrower completes payment obligations. Keywords: Wisconsin Security Agreement, Retail Installment Sale, Automobile, Car, Motor Vehicle, Financing, Lender, Borrower, Payment Obligations. There are different types of Wisconsin Security Agreements for Retail Installment Sale of Automobile, Car, or Motor Vehicle, depending on the specific needs and circumstances of the transaction. Below are some common variations: 1. Traditional Security Agreement: This type of security agreement is typically used for standard vehicle purchase financing. It defines the terms, repayment schedule, and interest rates associated with the loan, as well as the consequences of default or non-payment. 2. Balloon Payment Security Agreement: In some cases, borrowers may opt for a balloon payment arrangement, where smaller monthly installments are made throughout the loan term, with a large final payment at the end. This type of agreement includes specific provisions for the balloon payment and corresponding terms. 3. Adjustable-Rate Security Agreement: An adjustable-rate security agreement provides the lender with the option to adjust the interest rate periodically. This allows the interest rate to fluctuate based on an agreed-upon index, such as the prime rate or the treasury bill rate. 4. Subprime Security Agreement: Subprime security agreements are designed for borrowers with low credit scores or poor credit histories. These agreements often come with higher interest rates and stricter terms to mitigate the increased lending risk. 5. Joint Security Agreement: A joint security agreement is utilized when multiple individuals or entities are involved in financing the vehicle purchase. This agreement clarifies the responsibilities of each party involved and establishes the order of priority in case of default or repossession. Irrespective of the type, a Wisconsin Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle sets out the rights and obligations of both the lender and the borrower. It serves as a crucial legal document that protects the interests of all parties involved in the financing arrangement, ensuring transparency and compliance with Wisconsin state laws.