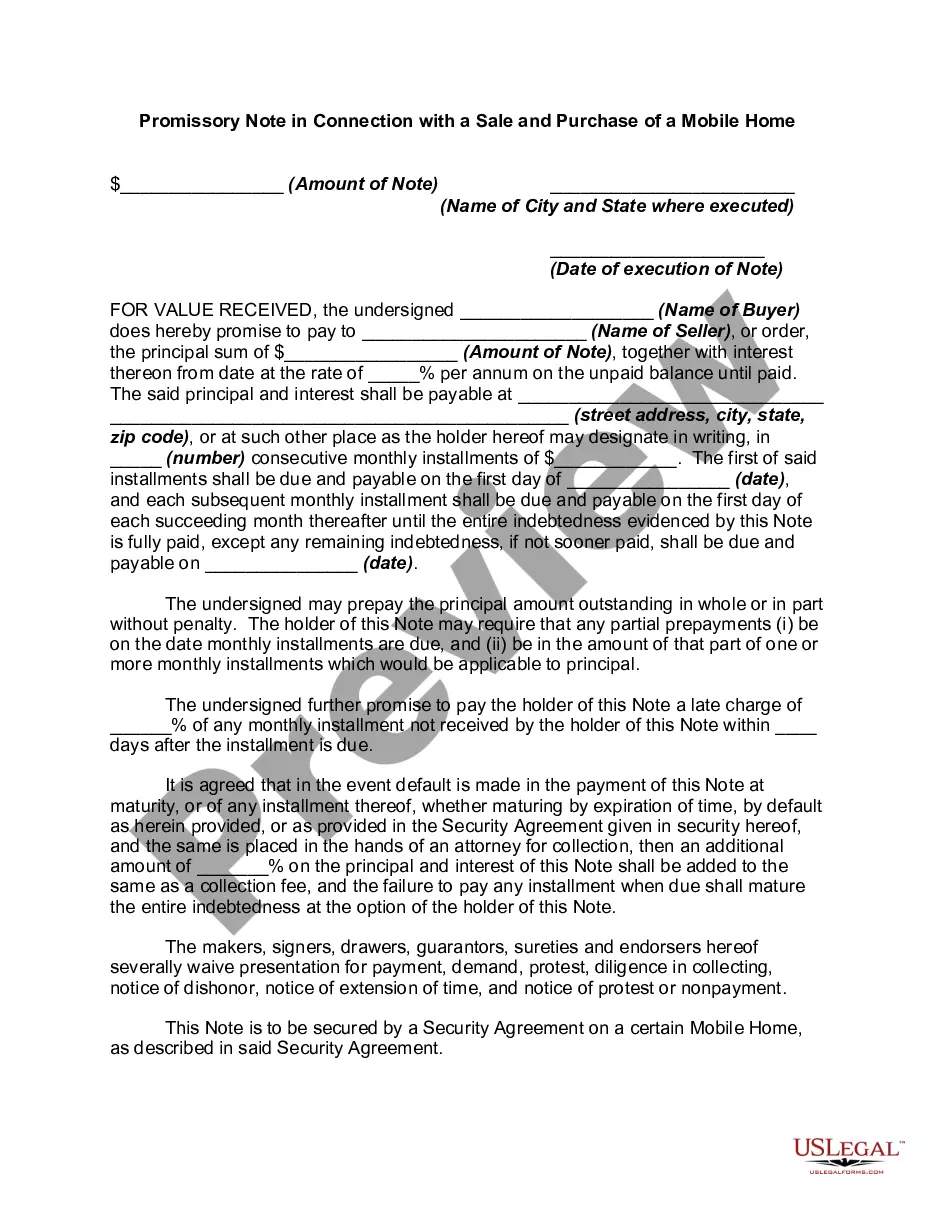

A Wisconsin Promissory Note in connection with a sale and purchase of a mobile home is a legally binding document that outlines the terms and conditions of a loan agreement between a buyer and a seller. It serves as a promissory note to evidence the borrower's promise to repay the loan amount, plus any interest, in scheduled installments. In Wisconsin, there are several types of Promissory Notes available for sale and purchase transactions of mobile homes: 1. Simple Promissory Note: This is the most common type used in Wisconsin, where the borrower agrees to make regular payments of principal and interest until the loan is fully repaid. 2. Secured Promissory Note: In some cases, a seller may require collateral to secure the loan. In this type of note, the mobile home itself serves as security for the loan, and if the borrower defaults, the seller has the right to repossess the property. 3. Balloon Promissory Note: This specific type involves payment of smaller periodic installments for a set term, followed by a larger final payment called a "balloon payment". It allows the borrower to make smaller payments initially and a lump sum payment at the end. 4. Installment Promissory Note: With this type, the loan amount is divided into equal installments over a specific period. The borrower is required to make fixed payments on a monthly basis, which includes both principal and interest. When drafting a Wisconsin Promissory Note in connection with a sale and purchase of a mobile home, some essential provisions must be included: 1. Identification of the parties: The note identifies the buyer (borrower) and the seller (lender) involved in the transaction, including their legal names and addresses. 2. Loan amount and interest: The note clearly states the principal amount being borrowed and the agreed interest rate that will be charged on the loan. 3. Repayment terms: It details the schedule for installment payments, including the frequency of payments (monthly, quarterly, etc.), the due date, and the number of payments required to fulfill the loan agreement. 4. Late fees and penalties: The note should specify the consequences for late or missed payments, such as additional fees or interest charges. 5. Default provisions: This outlines the actions the lender can take if the borrower fails to make payments as agreed, including the right to repossess the mobile home or pursue legal remedies. 6. Governing law: It states that the note is governed by Wisconsin state laws, ensuring that any legal disputes will be resolved according to Wisconsin regulations. It is important to consult with a legal professional when drafting or executing a Wisconsin Promissory Note in connection with a sale and purchase of a mobile home to ensure compliance with all relevant laws and to protect the interests of both parties involved.

Wisconsin Promissory Note in Connection with a Sale and Purchase of a Mobile Home

Description

How to fill out Wisconsin Promissory Note In Connection With A Sale And Purchase Of A Mobile Home?

If you wish to complete, acquire, or print out legitimate document web templates, use US Legal Forms, the biggest collection of legitimate forms, that can be found on the Internet. Make use of the site`s simple and hassle-free research to find the files you will need. Numerous web templates for organization and person uses are categorized by groups and suggests, or keywords. Use US Legal Forms to find the Wisconsin Promissory Note in Connection with a Sale and Purchase of a Mobile Home in just a handful of click throughs.

In case you are currently a US Legal Forms client, log in in your profile and click on the Down load switch to have the Wisconsin Promissory Note in Connection with a Sale and Purchase of a Mobile Home. You can even access forms you in the past acquired within the My Forms tab of your profile.

Should you use US Legal Forms for the first time, refer to the instructions under:

- Step 1. Ensure you have selected the shape for the correct metropolis/country.

- Step 2. Use the Review solution to examine the form`s content material. Never neglect to read the explanation.

- Step 3. In case you are unsatisfied with the type, utilize the Research field at the top of the monitor to locate other models in the legitimate type web template.

- Step 4. Upon having identified the shape you will need, click on the Buy now switch. Opt for the prices program you favor and add your accreditations to sign up for an profile.

- Step 5. Approach the financial transaction. You can utilize your charge card or PayPal profile to perform the financial transaction.

- Step 6. Pick the format in the legitimate type and acquire it in your device.

- Step 7. Full, change and print out or signal the Wisconsin Promissory Note in Connection with a Sale and Purchase of a Mobile Home.

Every legitimate document web template you get is the one you have for a long time. You have acces to each type you acquired in your acccount. Select the My Forms portion and select a type to print out or acquire again.

Compete and acquire, and print out the Wisconsin Promissory Note in Connection with a Sale and Purchase of a Mobile Home with US Legal Forms. There are thousands of skilled and condition-distinct forms you can utilize for your personal organization or person requires.