Any interested party in an estate of a decedent generally has the right to make objections to the accounting of the executor, the compensation paid or

proposed to be paid, or the proposed distribution of assets. Such objections must be filed within within a certain period of time from the date of service of the Petition for approval of the accounting.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

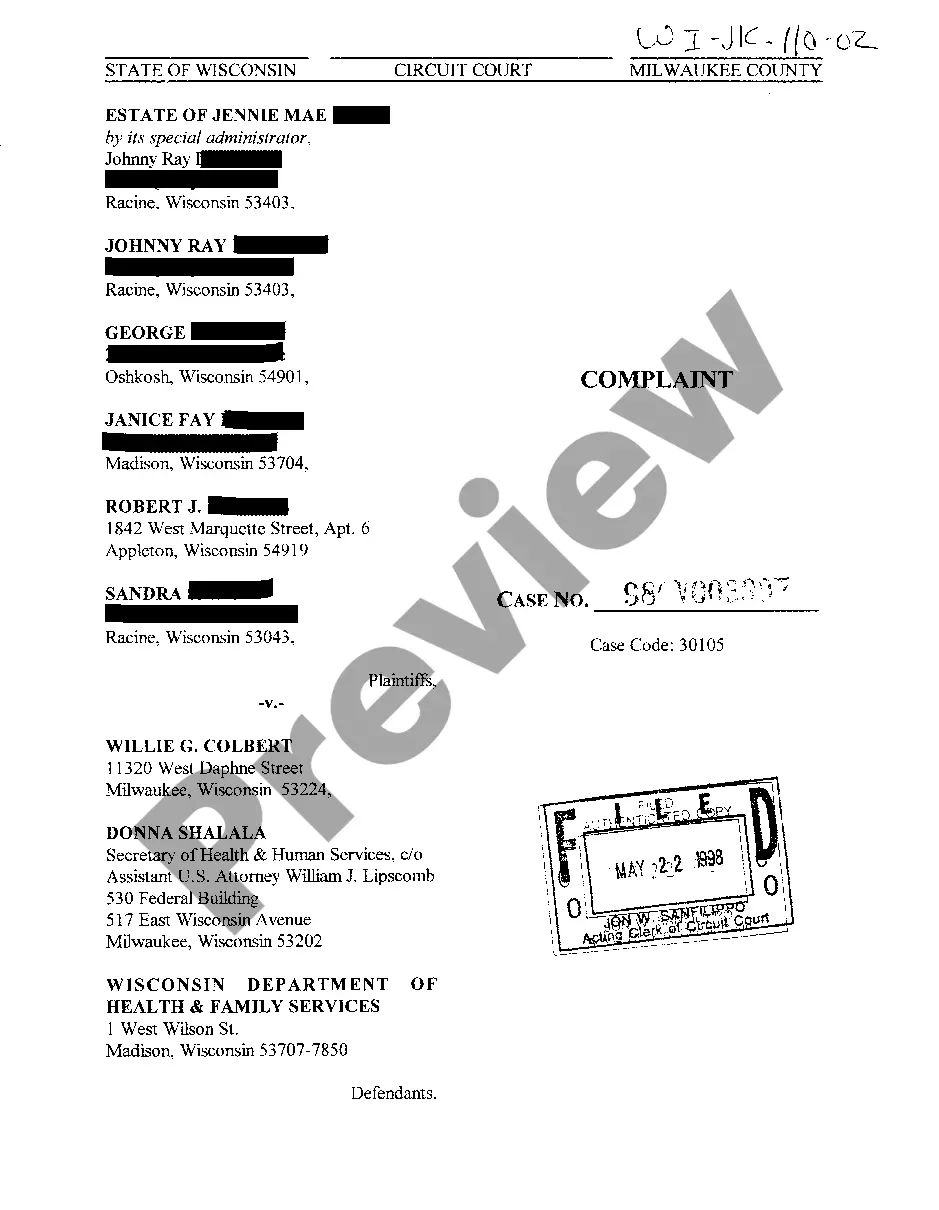

Keywords: Wisconsin, objection to allowed claim, accounting, detailed description Wisconsin Objection to Allowed Claim in Accounting refers to the process through which a party disputes or contests a claim that has been approved or accepted by an accounting authority in the state of Wisconsin. This objection is raised when there are concerns or disagreements regarding the validity, accuracy, or value of a claim submitted for accounting purposes. There are various types of objections to allowed claims in accounting in Wisconsin, including: 1. Material Misstatement Objection: This type of objection is raised when the claimant believes that there are significant errors or misstatements in the financial information or documents submitted as part of the claim. It typically argues that the claim does not accurately represent the financial position or transactions of the party involved. 2. Fraudulent Claim Objection: This objection is raised when there is suspicion or evidence indicating that the submitted claim is fraudulent or deceptive. Parties may object to such claims if they can present proof or demonstrate that the information provided is misleading, false, or fictitious. 3. Valuation Objection: This objection is made when there is a disagreement about the valuation of assets, liabilities, or other financial components included in the claim. Parties may challenge the claimed value by presenting alternative calculations or assessing different market factors influencing the valuation. 4. Procedural Objection: This type of objection is based on challenges to the process followed or the legal requirements adhered to during the claim assessment or approval. Parties may argue that the claimant did not adhere to specified timelines, procedural rules, or disclosure requirements, which could impact the validity of the claim. 5. Jurisdictional Objection: This objection arises when the party contests the jurisdiction or authority of the accounting body or organization overseeing the claim. It questions whether the body has the necessary jurisdiction and competence to assess the claim, particularly in cases where cross-border transactions or complex legal frameworks are involved. When a Wisconsin objection to an allowed claim is raised, it initiates a formal process that typically involves a detailed review, examination, and analysis of the claim and related evidence. The accounting authority responsible for reviewing the objection will carefully consider the arguments presented by both the objector and the claimant before rendering a decision. It is important to note that each objection to an allowed claim in accounting in Wisconsin may have its unique characteristics, depending on the specific circumstances and nature of the claim. Objectors must follow the designated procedures, provide substantial evidence to support their objections, and engage in fair and transparent discussions with the relevant accounting authority to seek resolution.