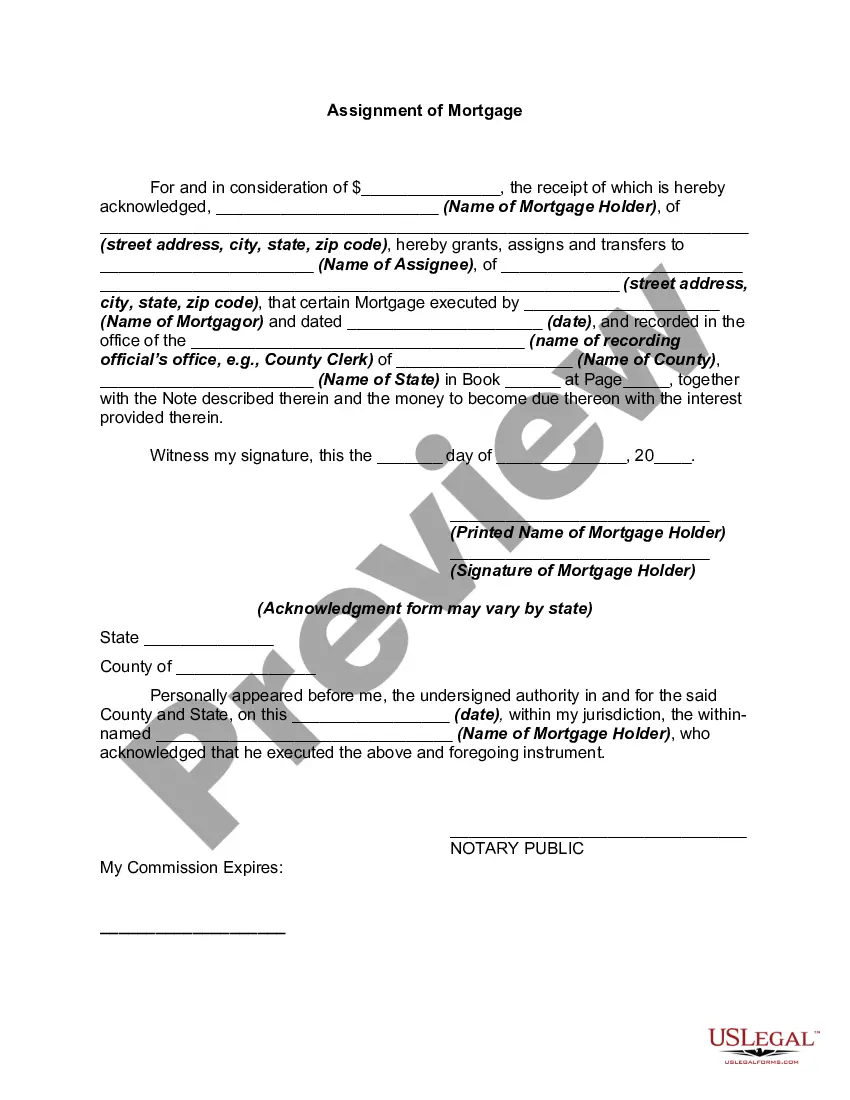

The Wisconsin Assignment of Mortgage is a legal document used to transfer the rights and interest of a mortgage from one party to another. When a borrower obtains a mortgage loan, they sign a promissory note and a mortgage securing the loan. The mortgage is a lien on the property, and if the borrower fails to repay the loan according to the agreed terms, the lender has the right to foreclose on the property and sell it to recover their investment. However, mortgage lenders often sell their loans or transfer the servicing rights to another financial institution. In such cases, an assignment of mortgage is necessary to legally transfer the mortgage from the original lender to the new entity responsible for collecting mortgage payments and enforcing the terms of the loan. This assignment ensures that the new lender or service has the legal authority to take action in case of default. The Wisconsin Assignment of Mortgage is governed by specific laws and regulations to ensure a transparent and lawful transfer process. It requires certain information to be included, such as the names of the assignor (original lender) and assignee (new lender or service), the date of assignment, the original mortgage details, and the property information being secured by the mortgage. In Wisconsin, there are no specific types of assignment of mortgage. However, variations can occur based on the type of loan being assigned or the nature of the transaction. For example, if a mortgage loan is being sold in the secondary market, an assignment may be executed to transfer the rights from the original lender (often a bank) to an investor or another financial institution. Alternatively, an assignment may be used when a mortgage loan is being refinanced, and the original lender transfers the mortgage to a new lender that provides better terms or a lower interest rate. Keywords: Wisconsin Assignment of Mortgage, transfer of rights, mortgage lien, promissory note, mortgage loan, foreclosure, servicing rights, financial institution, default, laws and regulations, assignor, assignee, property information, secondary market, investor, refinancing.

Wisconsin Assignment of Mortgage

Description

How to fill out Wisconsin Assignment Of Mortgage?

Are you in the situation in which you need papers for both company or personal reasons just about every day time? There are a variety of legal document themes accessible on the Internet, but locating kinds you can trust is not easy. US Legal Forms provides a large number of kind themes, like the Wisconsin Assignment of Mortgage, which can be composed to satisfy state and federal demands.

In case you are previously informed about US Legal Forms internet site and also have your account, merely log in. After that, you can obtain the Wisconsin Assignment of Mortgage template.

Unless you offer an accounts and would like to begin to use US Legal Forms, adopt these measures:

- Obtain the kind you want and ensure it is for the right town/area.

- Take advantage of the Preview button to examine the form.

- Read the description to ensure that you have chosen the right kind.

- When the kind is not what you`re seeking, use the Lookup industry to obtain the kind that meets your requirements and demands.

- Whenever you obtain the right kind, just click Purchase now.

- Select the rates program you need, submit the specified information to generate your account, and buy your order with your PayPal or charge card.

- Choose a convenient document file format and obtain your backup.

Get all of the document themes you have purchased in the My Forms food list. You can aquire a more backup of Wisconsin Assignment of Mortgage any time, if needed. Just select the necessary kind to obtain or printing the document template.

Use US Legal Forms, probably the most considerable selection of legal forms, in order to save some time and stay away from faults. The assistance provides expertly made legal document themes that you can use for a variety of reasons. Make your account on US Legal Forms and initiate making your way of life a little easier.