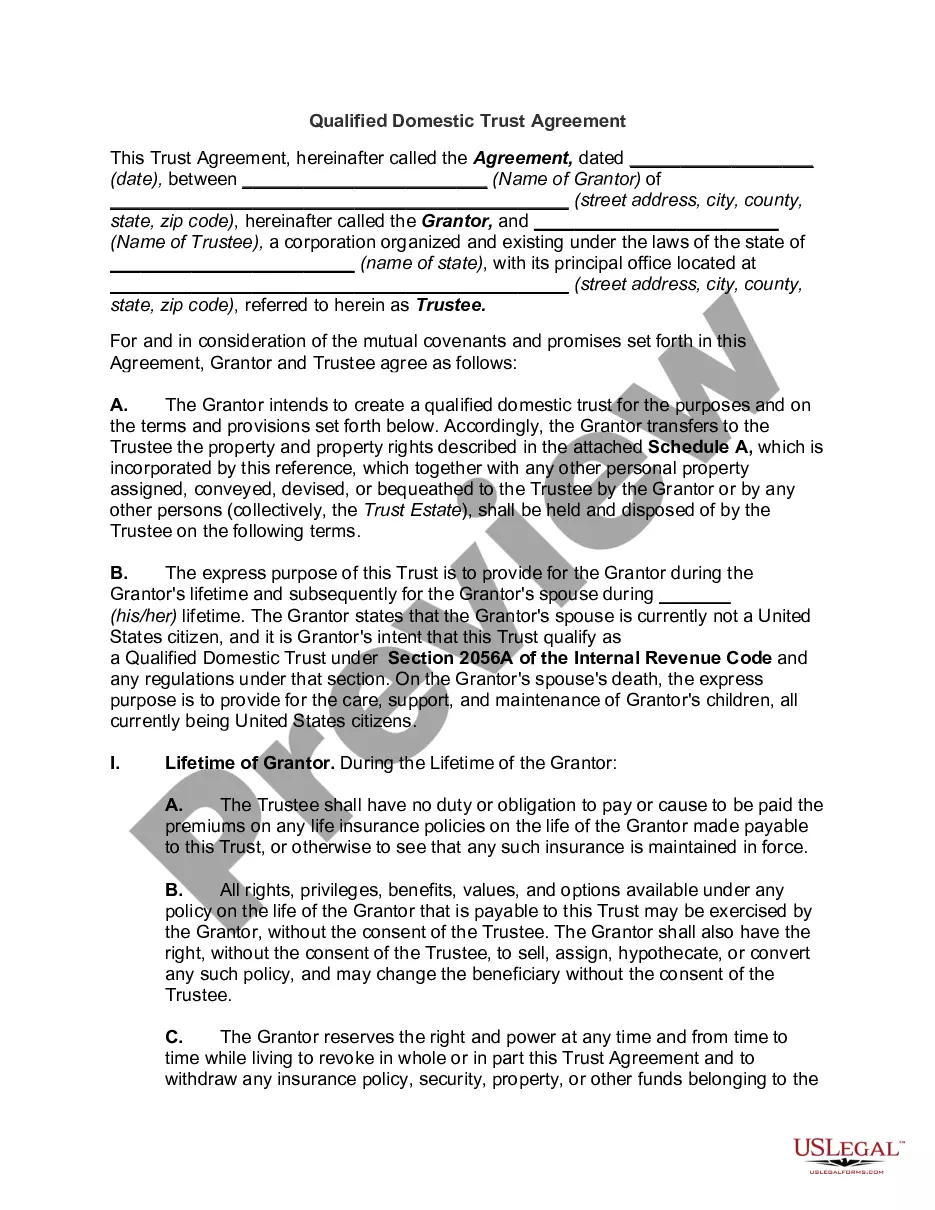

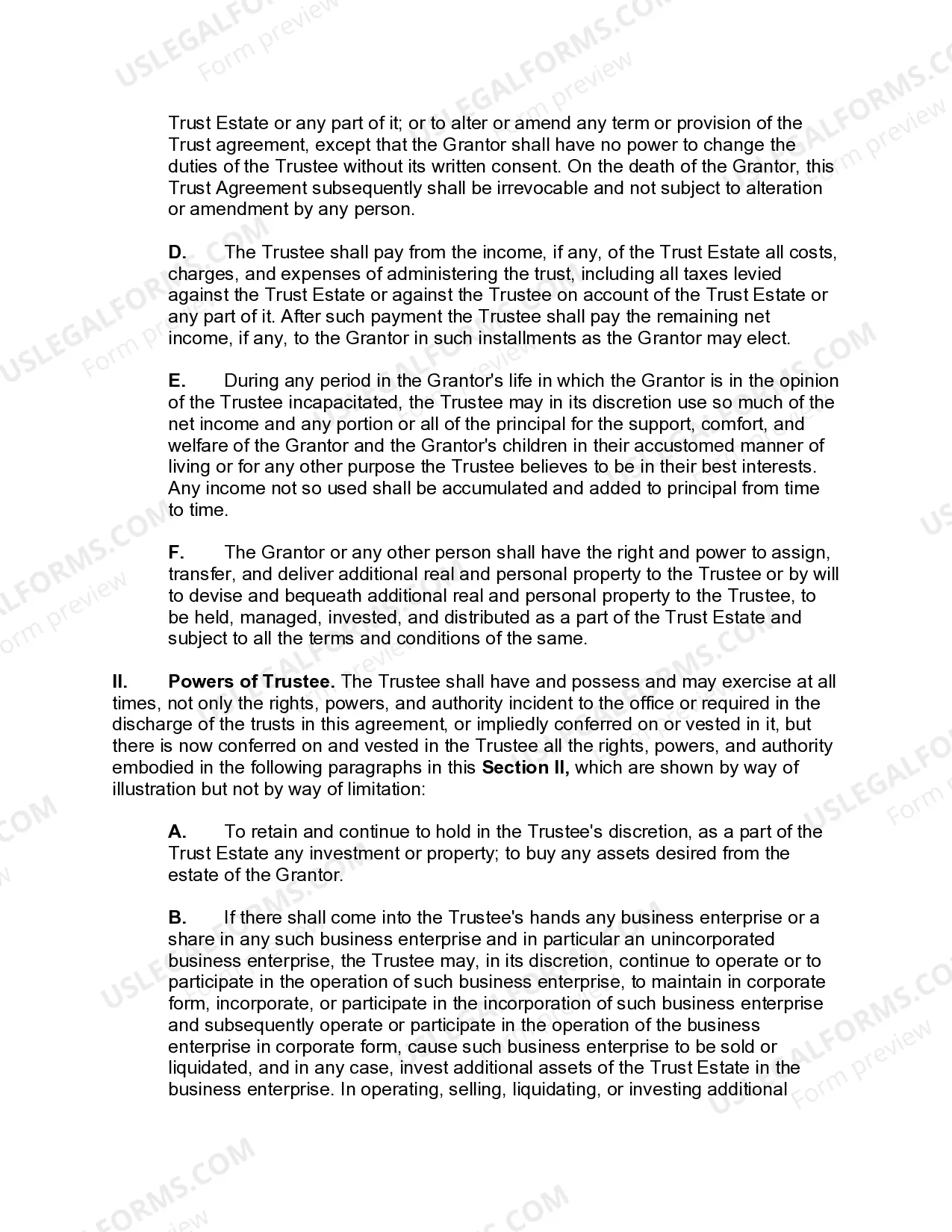

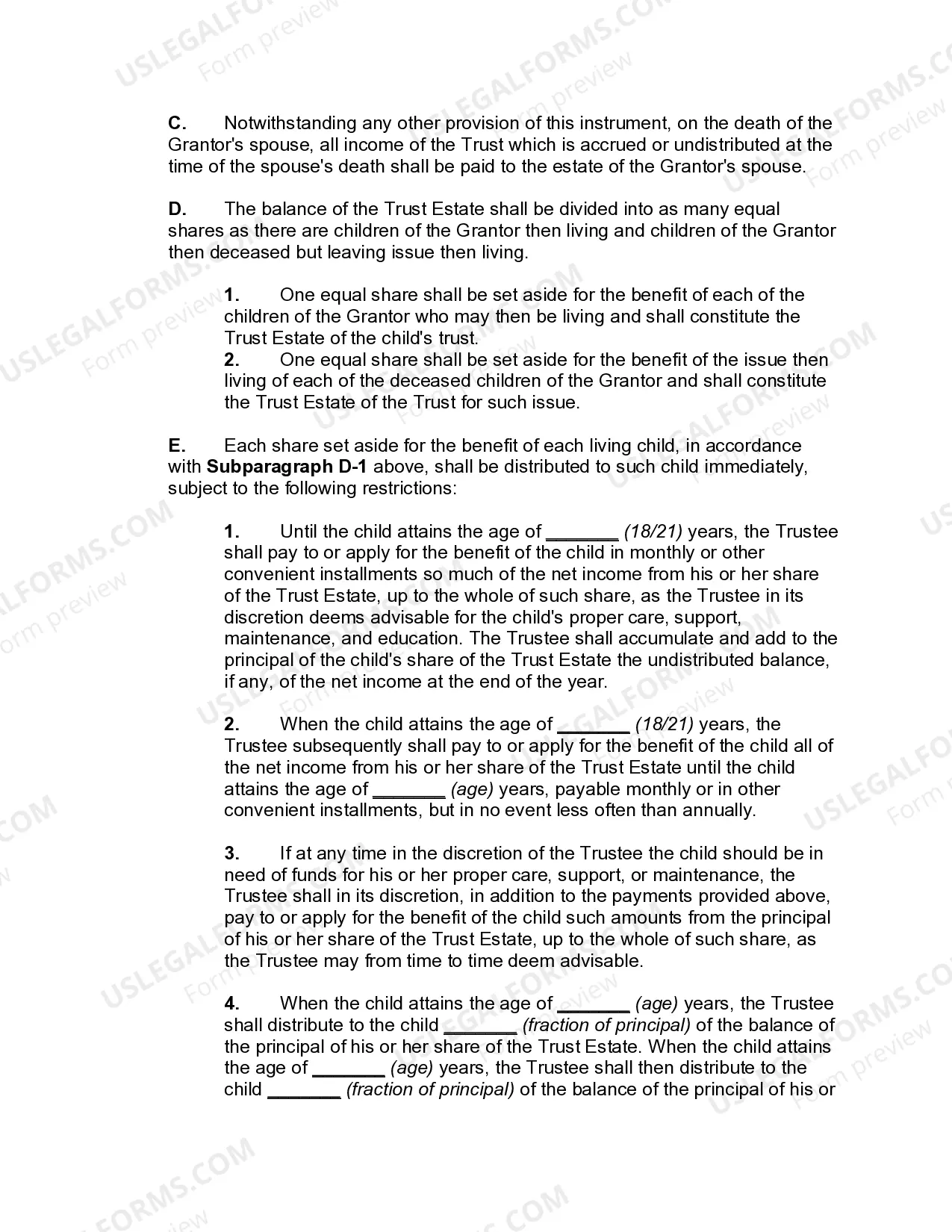

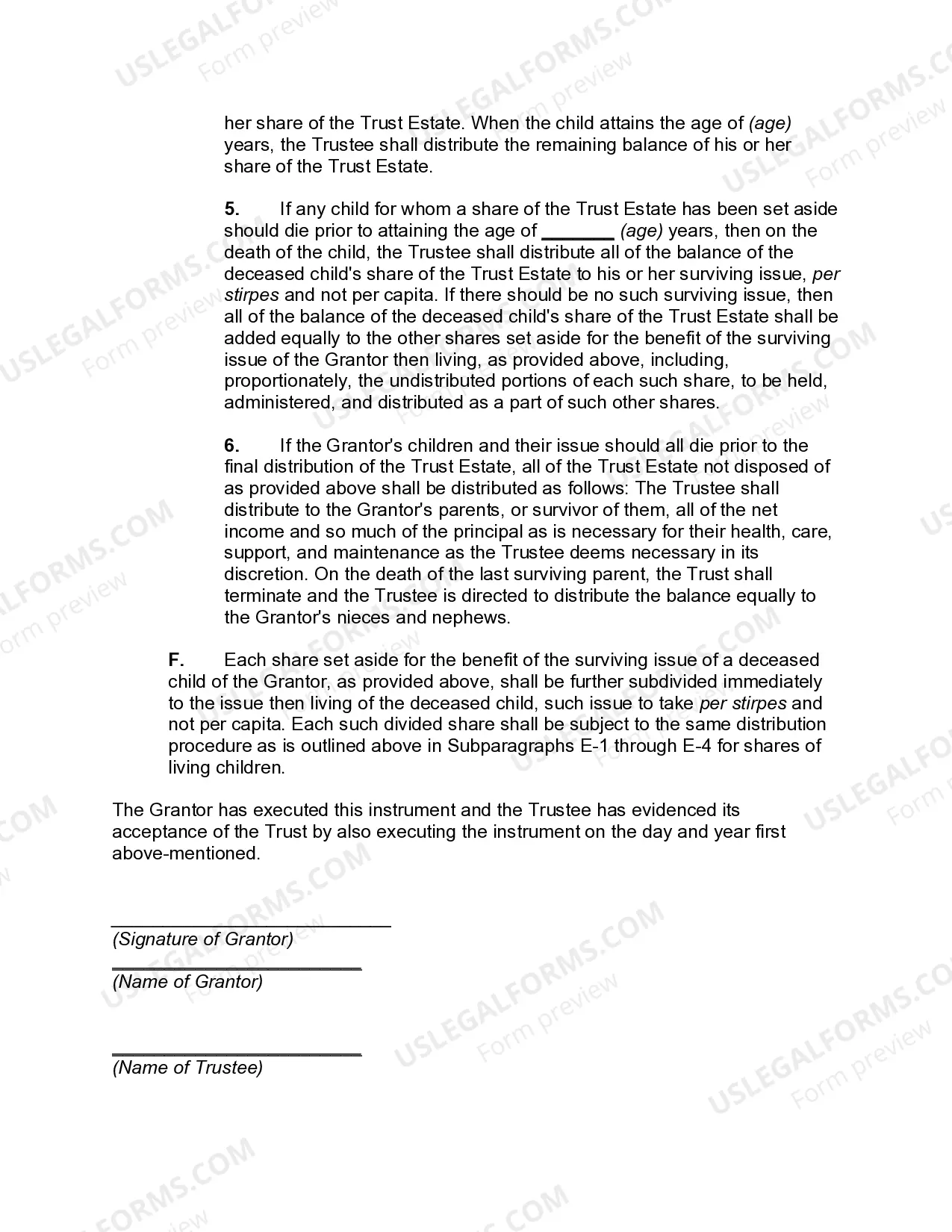

A Wisconsin Qualified Domestic Trust Agreement, also known as a DOT, is a legal arrangement designed to minimize estate tax liability for non-citizen spouses in Wisconsin. This trust allows a non-U.S. citizen surviving spouse to benefit from the assets of the deceased spouse without incurring immediate estate tax liabilities. Under U.S. estate tax laws, when a U.S. citizen who is married to a non-U.S. citizen passes away, the unlimited marital deduction does not apply to the non-citizen spouse. As a result, if the deceased spouse's assets exceed the federal estate tax exemption limit (which is set at $11.7 million in 2021), those assets may be subjected to estate taxes. However, by establishing a DOT as part of an estate plan, individuals can defer estate tax payments until distributions are made to the non-citizen spouse. A DOT must meet certain requirements to obtain the qualified status. Firstly, it must be created under Wisconsin law or by a Wisconsin resident. Secondly, at least one trustee of the DOT must be a U.S. citizen or a domestic corporation. Additionally, the trust must provide that any distributions made from the trust to the non-citizen spouse are subject to federal estate taxes. By deferring estate taxes until distributions are made from the trust, a DOT provides the non-U.S. citizen surviving spouse with access to income and principal from the trust while preserving the estate tax deferral benefits. This option ensures the financial security of the surviving spouse while still being compliant with the federal estate tax laws. It is essential to note that there are no specific types of Wisconsin Dots described in the legal terminology. However, the design and provisions of a DOT can vary based on the specific needs and circumstances of the individuals involved. Experienced estate planning attorneys in Wisconsin can assist in tailoring the DOT to meet the unique requirements of the couple and comply with relevant legal regulations. In conclusion, a Wisconsin Qualified Domestic Trust Agreement, or DOT, is a valuable tool for non-U.S. citizen spouses to mitigate estate tax liabilities when inheriting assets from their U.S. citizen spouse. Through deferring estate taxes until distributions are made, a DOT ensures the financial well-being of the non-citizen surviving spouse while adhering to federal estate tax laws. Seeking advice from legal professionals well-versed in estate planning and Dots is crucial to establish a suitable trust arrangement catered to one's individual circumstances.

Wisconsin Qualified Domestic Trust Agreement

Description

How to fill out Wisconsin Qualified Domestic Trust Agreement?

Have you been in a placement in which you require paperwork for either organization or person functions nearly every working day? There are a lot of legal file web templates available on the Internet, but getting kinds you can rely isn`t simple. US Legal Forms offers a large number of form web templates, just like the Wisconsin Qualified Domestic Trust Agreement, that are written to meet state and federal specifications.

In case you are already familiar with US Legal Forms website and possess your account, merely log in. Next, you are able to acquire the Wisconsin Qualified Domestic Trust Agreement web template.

Should you not have an accounts and need to start using US Legal Forms, adopt these measures:

- Find the form you will need and make sure it is for that proper city/region.

- Take advantage of the Review key to analyze the form.

- See the explanation to ensure that you have chosen the right form.

- When the form isn`t what you`re seeking, use the Look for industry to discover the form that meets your requirements and specifications.

- Whenever you find the proper form, click Purchase now.

- Select the pricing program you desire, fill in the desired info to create your money, and buy an order with your PayPal or bank card.

- Choose a handy file format and acquire your backup.

Find all of the file web templates you might have bought in the My Forms food selection. You can aquire a more backup of Wisconsin Qualified Domestic Trust Agreement at any time, if necessary. Just select the needed form to acquire or produce the file web template.

Use US Legal Forms, one of the most comprehensive assortment of legal varieties, to conserve efforts and steer clear of mistakes. The service offers expertly made legal file web templates that you can use for a variety of functions. Create your account on US Legal Forms and start generating your way of life easier.

Form popularity

FAQ

Estates, Trusts & Gifts. A qualified revocable trust (QRT) is any trust (or part of a trust) that was treated as owned by a decedent (on that decedent's date of death) by reason of a power to revoke that was exercisable by the decedent (without regard to whether the power was held by the decedent's spouse).

For tax purposes a trust may be taxed in any state for which it is determined to be a resident trust under the governing states definition of residency. This could be based on the location of the grantor, the location of the trustee or trust administrator, or the location of the beneficiaries.

Trusts, or portions of trusts, the assets of which consist of property placed in the trust by a person who is a resident of Wisconsin at the time that the property was placed in the trust if, at the time that the assets were placed in the trust, the trust was irrevocable.

If someone dies in Wisconsin with less than the exemption amount (currently $12,006,000), their estate doesn't owe any federal estate tax, and there is no Wisconsin estate tax. The heirs and beneficiaries inherit the property free of tax.

According to the IRS, gifts, inheritances, and bequests are generally not considered taxable income for recipients. If you receive property that produces income, though, such as dividends or IRA distributions, that income will be taxable to you.

Residency of the beneficiary. California, Georgia, Montana, North Carolina, North Dakota, and Tennessee tax a trust if it has one or more resident beneficiaries. Generally, only income attributable to the resident beneficiary is taxed by the state.

Wisconsin also has no inheritance tax, but there is a possibility you'll owe an inheritance tax in another state if you inherit money or property from someone living in that state.

To be considered a qualified trust, the trust must. be valid under state law; be irrevocable or, if revocable while the IRA owner is alive, must become irrevocable upon the IRA owner's death; and. have identifiable beneficiaries (generally people) listed.

A trust can be created while the grantor is alive, while an estate is created at the moment of someone's death. A trust is intended to be a semi-permanent entity. It exists to distribute assets over time according to a series of rules and conditions, overseen by a trustee. An estate is intended to be temporary.