This form is a business type form that is formatted to allow you to complete the form using Adobe Acrobat or Word. The word files have been formatted to allow completion by entry into fields. Some of the forms under this category are rather simple while others are more complex. The formatting is worth the small cost.

Wisconsin Balance Sheet Notes Payable

Category:

State:

Multi-State

Control #:

US-123-AZ

Format:

Word;

PDF;

Rich Text

Instant download

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Balance Sheet Notes Payable?

If you need extensive, obtain, or printing legal document templates, use US Legal Forms, the largest selection of legal forms available online.

Utilize the site’s user-friendly and convenient search to find the documents you need.

Various templates for business and personal use are classified by categories and states, or keywords.

Step 4. Once you have found the form you need, click the Download now button. Choose the pricing plan you prefer and enter your credentials to register for an account.

Step 5. Process the payment. You can use your credit card or PayPal account to complete the transaction.

- Use US Legal Forms to get the Wisconsin Balance Sheet Notes Payable in just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and click the Download button to get the Wisconsin Balance Sheet Notes Payable.

- You can also access forms you previously purchased from the My documents tab of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Ensure you have selected the template for the correct city/state.

- Step 2. Utilize the Preview option to review the form’s content. Remember to read the summary.

- Step 3. If you are unsatisfied with the form, use the Search field at the top of the screen to find other templates in the legal form directory.

Form popularity

FAQ

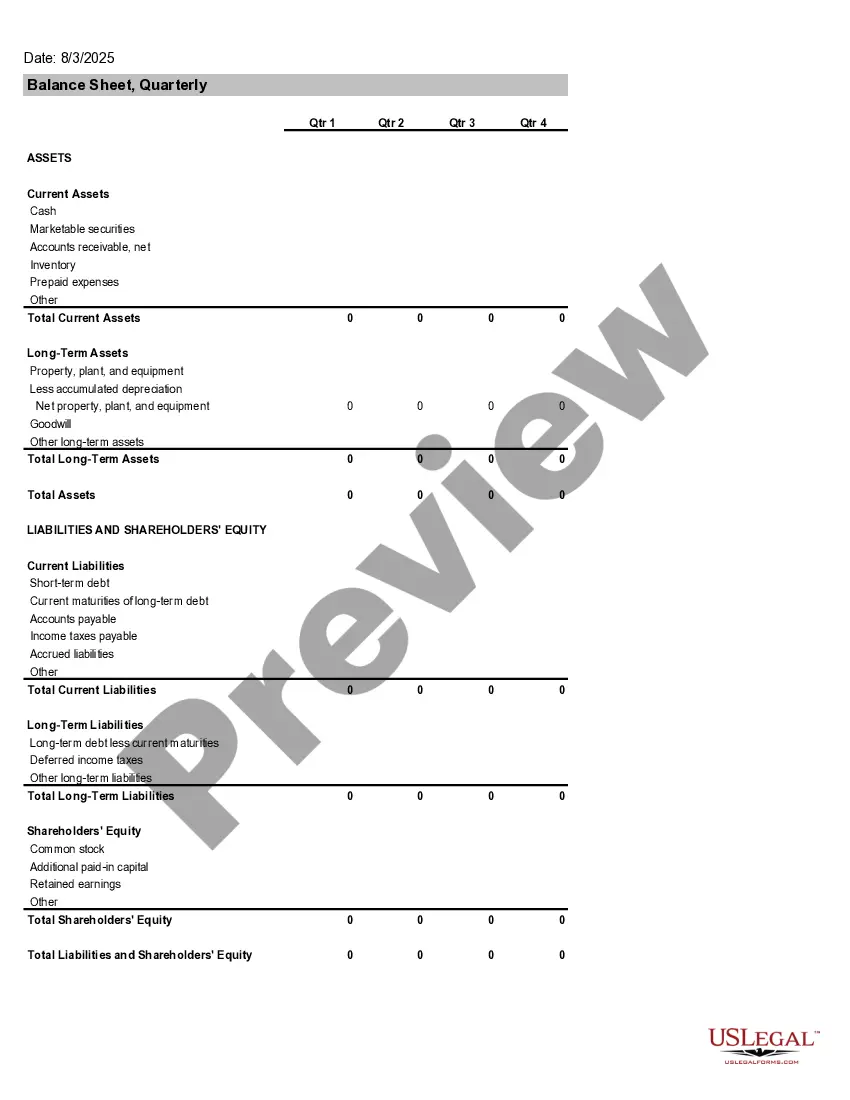

Some notes payable are secured, which means the creditor has a claim on the borrower's assets if payment terms are not met. If secured, the timeline for repayment could be longer. Notes payable appear under liabilities on the balance sheet, separated into bank debt and other long-term notes payable.

Notes to the financial statements disclose the detailed assumptions made by accountants when preparing a company's: income statement, balance sheet, statement of changes of financial position or statement of retained earnings. The notes are essential to fully understanding these documents.

Recorded on the right side of the balance sheet, liabilities include loans, accounts payable, mortgages, deferred revenues, bonds, warranties, and accrued expenses.

The principal payment of your loan will not be included in your business' income statement. This payment is a reduction of your liability, such as Loans Payable or Notes Payable, which is reported on your business' balance sheet. The principal payment is also reported as a cash outflow on the Statement of Cash Flows.

If a party takes out a loan, they receive cash, which is a current asset, but the loan amount is also added as a liability on the balance sheet. If a party issues a loan that will be repaid within one year, it may be a current asset.

Accounts payable (AP) represents the amount that a company owes to its creditors and suppliers (also referred to as a current liability account). Accounts payable is recorded on the balance sheet under current liabilities.

Both accounts payables and accrued expenses are liabilities. Accounts payable is the total amount of short-term obligations or debt a company has to pay to its creditors for goods or services bought on credit. With accounts payables, the vendor's or supplier's invoices have been received and recorded.

Accounts payable is listed on a company's balance sheet. Accounts payable is a liability since it is money owed to creditors and is listed under current liabilities on the balance sheet. Current liabilities are short-term liabilities of a company, typically less than 90 days.

Loans payable is a liability account listing the amount of any loan debt you've taken out and haven't repaid. A loans receivable asset account lists the amounts a lender has paid out to borrowers.

When a company borrows money from its bank, the amount received is recorded with a debit to Cash and a credit to a liability account, such as Notes Payable or Loans Payable, which is reported on the company's balance sheet.