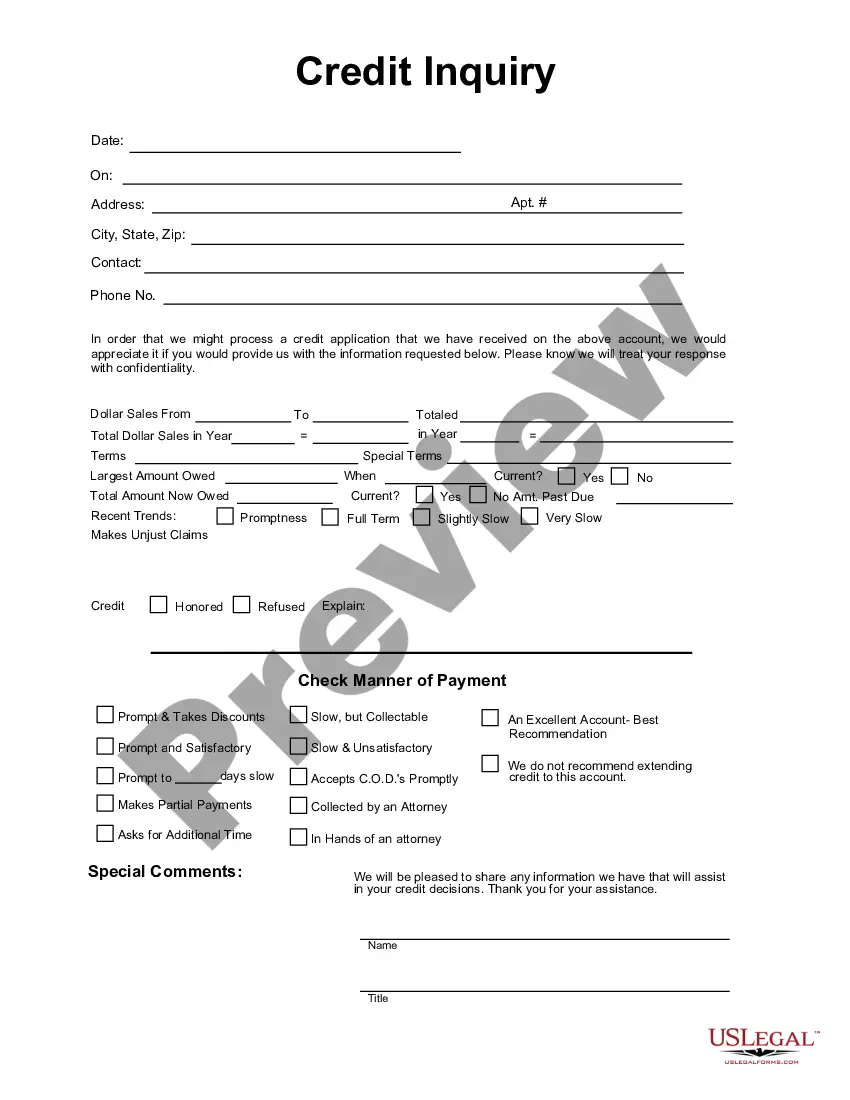

Wisconsin Credit Inquiry refers to the process of accessing an individual's credit report in the state of Wisconsin. A credit inquiry is typically requested by lenders, financial institutions, landlords, employers, or insurance companies to assess an individual's creditworthiness and make informed decisions regarding extending credit, rental agreements, employment, or insurance coverage. In Wisconsin, credit inquiries are governed by state and federal laws to protect consumers' privacy and ensure fair credit reporting practices. There are two types of Wisconsin Credit Inquiries: soft inquiries and hard inquiries. Soft inquiries are usually initiated by individuals themselves or by businesses for promotional purposes. They do not impact the credit score and are often used for pre-approval offers, background checks, or personal credit monitoring. Soft inquiries can be initiated by credit card companies offering pre-qualified credit card offers or individuals checking their own credit reports. On the other hand, hard inquiries are typically requested when an individual applies for credit, whether it is a loan, credit card, mortgage, or any other form of credit-based service. Hard inquiries can slightly lower an individual's credit score and may stay on the credit report for up to two years. Multiple hard inquiries within a short period can raise concerns for lenders as it may imply a high level of credit-seeking activity and potential financial risk. To initiate a Wisconsin Credit Inquiry, authorized entities must adhere to specific legal requirements, such as obtaining written consent from the individual, complying with the Fair Credit Reporting Act (FCRA), and providing clear disclosure of the purpose and nature of the inquiry. The FCRA also grants consumers the right to dispute inaccurate or incomplete information present on their credit reports. In Wisconsin, consumers have the option to freeze or restrict access to their credit reports through a credit freeze. This allows individuals to protect their credit data from unauthorized access, reducing the risk of identity theft, and preventing the misuse of personal information. In summary, Wisconsin Credit Inquiry refers to the process of accessing an individual's credit report in compliance with state and federal laws. It involves both soft and hard inquiries, used for different purposes and with varying impacts on an individual's credit score. By understanding these credit inquiry types and regulations, individuals can stay informed and make responsible financial decisions while protecting their privacy and creditworthiness.

Wisconsin Credit Inquiry

Description

How to fill out Wisconsin Credit Inquiry?

Choosing the best authorized file format could be a battle. Naturally, there are a lot of themes available on the net, but how would you discover the authorized type you require? Use the US Legal Forms internet site. The services offers a huge number of themes, like the Wisconsin Credit Inquiry, that can be used for company and personal requirements. All the forms are examined by pros and meet federal and state needs.

When you are already registered, log in in your account and then click the Download button to get the Wisconsin Credit Inquiry. Make use of your account to search with the authorized forms you may have acquired earlier. Visit the My Forms tab of your own account and acquire yet another backup from the file you require.

When you are a whole new end user of US Legal Forms, listed below are simple recommendations so that you can comply with:

- Very first, make certain you have chosen the correct type for your personal town/state. You can check out the form making use of the Review button and read the form information to ensure this is the best for you.

- When the type is not going to meet your requirements, use the Seach industry to find the correct type.

- Once you are certain that the form is proper, click on the Buy now button to get the type.

- Select the costs program you would like and type in the essential info. Create your account and purchase the order using your PayPal account or Visa or Mastercard.

- Opt for the submit file format and acquire the authorized file format in your device.

- Complete, edit and produce and signal the acquired Wisconsin Credit Inquiry.

US Legal Forms may be the largest library of authorized forms where you can see numerous file themes. Use the company to acquire appropriately-produced files that comply with status needs.