Wisconsin Split-Dollar Life Insurance

Description

How to fill out Split-Dollar Life Insurance?

Choosing the best authorized file web template can be quite a have a problem. Of course, there are a variety of templates available on the net, but how will you get the authorized form you need? Take advantage of the US Legal Forms web site. The services delivers 1000s of templates, such as the Wisconsin Split-Dollar Life Insurance, that can be used for company and personal requirements. All of the forms are examined by specialists and meet state and federal needs.

Should you be presently listed, log in to the accounts and click on the Obtain switch to have the Wisconsin Split-Dollar Life Insurance. Utilize your accounts to look throughout the authorized forms you may have ordered earlier. Check out the My Forms tab of your accounts and acquire an additional version of your file you need.

Should you be a brand new customer of US Legal Forms, allow me to share basic instructions for you to adhere to:

- Very first, be sure you have chosen the appropriate form for your city/state. It is possible to look through the form while using Preview switch and read the form outline to make certain it is the right one for you.

- When the form does not meet your expectations, utilize the Seach field to obtain the correct form.

- When you are certain that the form would work, select the Purchase now switch to have the form.

- Select the pricing prepare you need and enter in the required information. Create your accounts and buy the transaction using your PayPal accounts or charge card.

- Select the document structure and obtain the authorized file web template to the product.

- Complete, modify and print out and sign the attained Wisconsin Split-Dollar Life Insurance.

US Legal Forms is the greatest collection of authorized forms in which you will find numerous file templates. Take advantage of the company to obtain expertly-made documents that adhere to condition needs.

Form popularity

FAQ

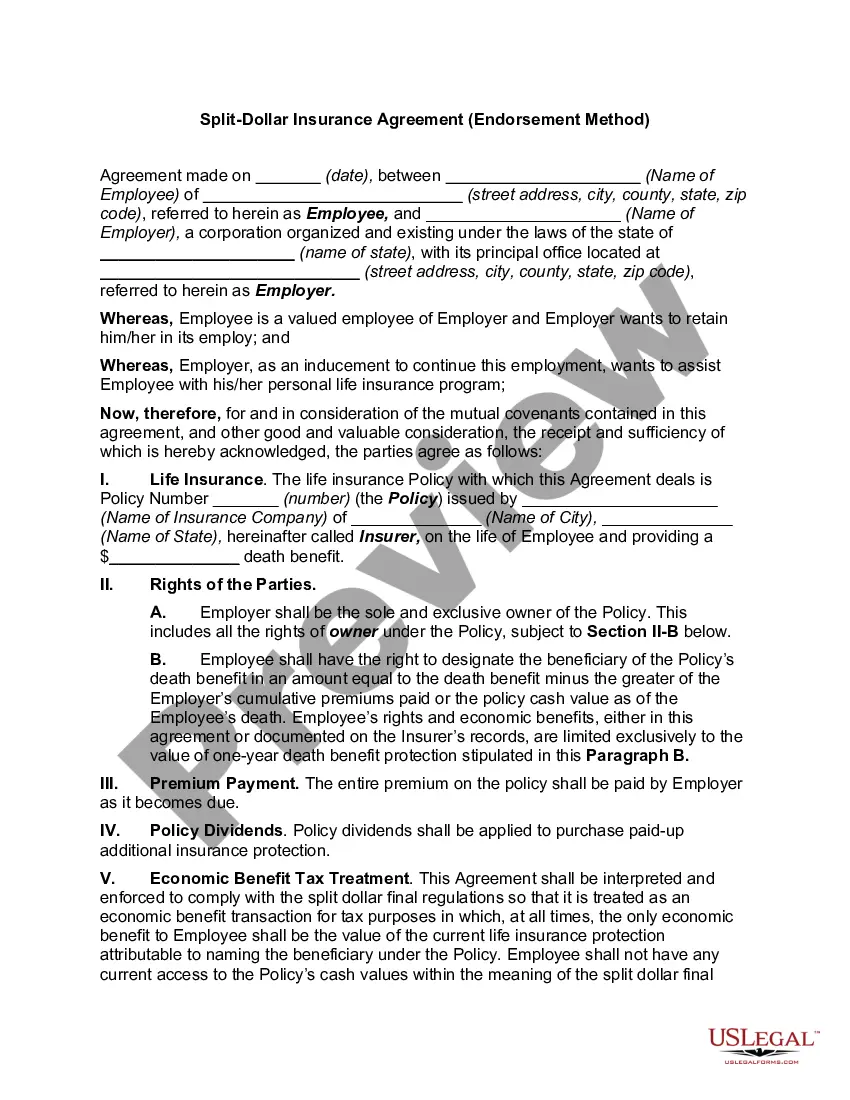

dollar life insurance agreement (or ?splitdollar plan?) is a strategy generally used as an employer benefit or for estate planning involving life insurance. It's an agreement between two or more parties to share the ownership, costs, and benefits of a permanent life insurance policy, like whole life.

Split Dollar Loan Regime Agreement & Contract Generally, at the employee's death, the employer receives a portion of the death benefit (usually equal to the total premiums plus interest from the loan) and the employee's beneficiary receives the balance.

While split-dollar life insurance arrangements offer numerous advantages, they also come with potential drawbacks, such as complexity, tax considerations, and limited availability. Both employers and employees must carefully weigh the benefits and disadvantages of this type of arrangement before deciding to pursue it.

?Economic benefit? refers to how the IRS treats this type of split-dollar insurance agreement. It means your employer is giving you some benefit but not a loan. That means you'll be taxed on the value of the life insurance provided, and that value is determined by the IRS or the insurance company.

Employers are responsible for making split-dollar life insurance premiums, regardless of the plan's type. However, it is important to note that under loan arrangements, employees must repay the premiums via collateral assignments made to their employer.

Common fringe benefits are basic items often included in hiring packages. These include health insurance, life insurance, tuition assistance, childcare reimbursement, cafeteria subsidies, below-market loans, employee discounts, employee stock options, and personal use of a company-owned vehicle.

There is no cost to the employee-participant unless the policy is transferred to them. This endorsement split-dollar plan is most often used to provide a low-cost death benefit to the employee-participant as a fringe benefit or where the employer wishes to own the policy and/or obtain key person protection.

The best way is to contact the policy's issuer (the life insurance company). Their records are key: even if you see your name listed on an old policy document, the deceased may have changed their beneficiaries (or the allocation of benefits among those beneficiaries) after that document was printed.

dollar life insurance agreement (or ?splitdollar plan?) is a strategy generally used as an employer benefit or for estate planning involving life insurance. It's an agreement between two or more parties to share the ownership, costs, and benefits of a permanent life insurance policy, like whole life.