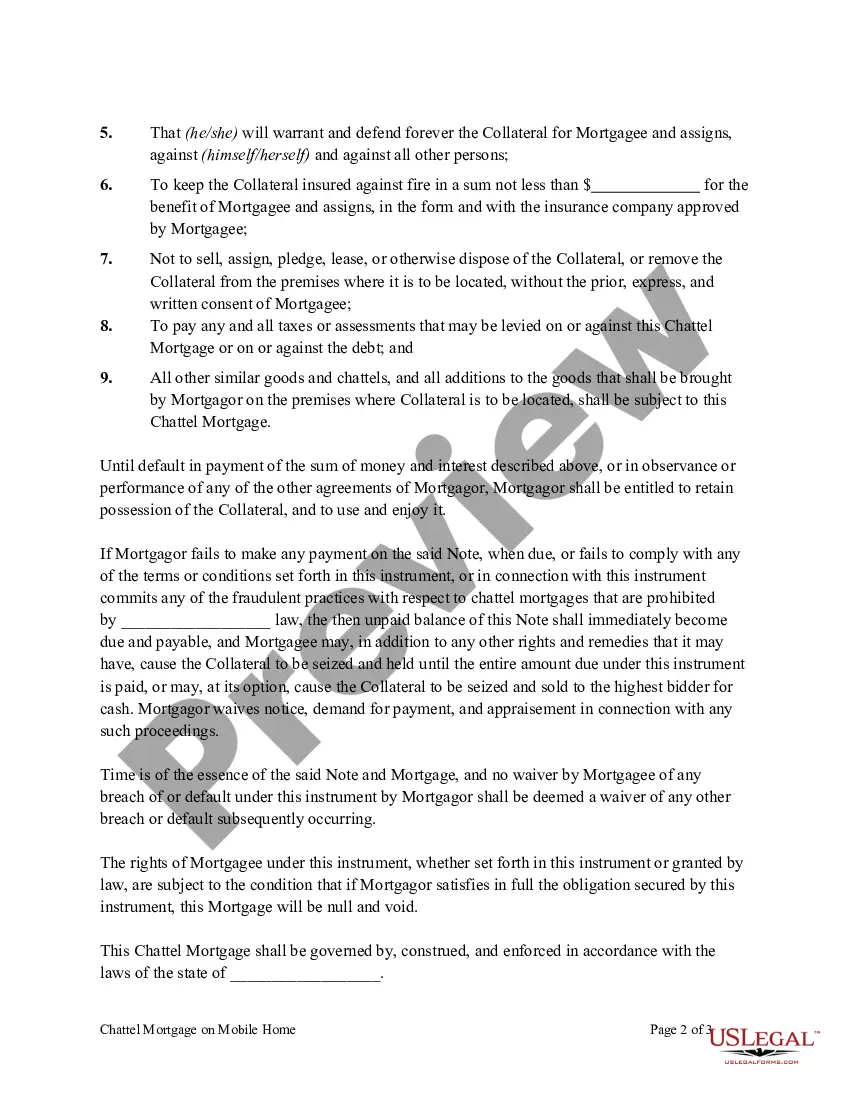

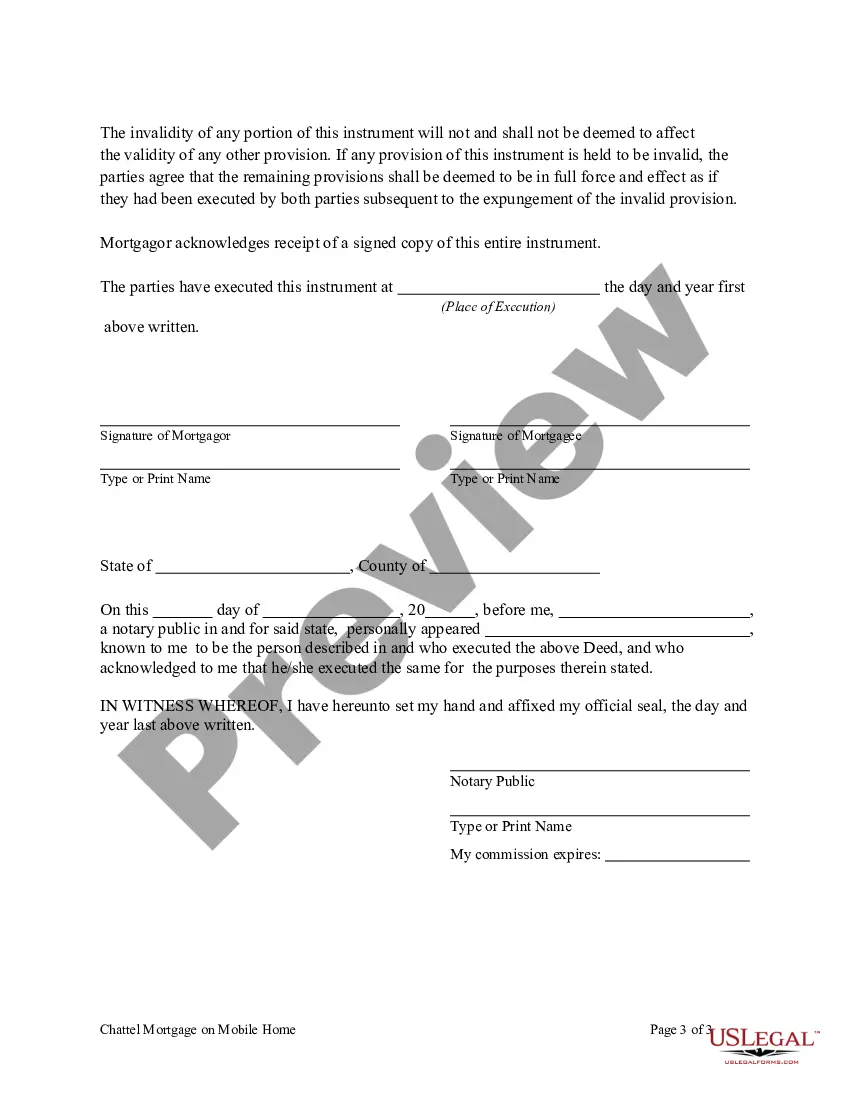

Title: West Virginia Chattel Mortgage on Mobile Home: A Comprehensive Guide to Understanding and Applying Introduction: In West Virginia, a Chattel Mortgage on a Mobile Home refers to a type of financing arrangement allowing individuals to secure a loan using their mobile home as collateral. This form of mortgage serves as an effective financial solution for individuals seeking to purchase a mobile home or access funds using their existing mobile home's value. This article aims to provide an in-depth understanding of West Virginia Chattel Mortgage on Mobile Home, its types, eligibility criteria, application process, benefits, and legal aspects. 1. Understanding West Virginia Chattel Mortgage on Mobile Home: A Chattel Mortgage in West Virginia is a legal agreement granting a lender temporary ownership rights over a mobile home until the borrower pays off the loan in full. This arrangement ensures the mobile home acts as collateral to secure the loan. 2. Types of West Virginia Chattel Mortgage on Mobile Home: a) Purchase Chattel Mortgage: This type of Chattel Mortgage is used when financing the initial purchase of a mobile home. It allows borrowers to secure a loan to buy a new or pre-owned mobile home. b) Refinance Chattel Mortgage: Borrowers who already own a mobile home can opt for this type of mortgage to access funds by using their mobile home's equity as collateral. 3. Eligibility Criteria for West Virginia Chattel Mortgage on Mobile Home: To qualify for a Chattel Mortgage on a Mobile Home in West Virginia, applicants generally need to meet the following criteria: — Proof of ownership of the mobilHOMom— - Adequate income and creditworthiness to repay the loan — Satisfy the lender's specific requirements 4. Applying for West Virginia Chattel Mortgage on Mobile Home: a) Gather Documentation: Prepare necessary documents such as proof of ownership, personal identification, proof of income, and credit history. b) Select a Lender: Research and choose a reputable lender offering Mobile Home Chattel Mortgages in West Virginia. c) Application Submission: Submit the completed application along with the required documents to the chosen lender. d) Loan Evaluation: The lender will assess the application, review creditworthiness, and determine the mobile home's value. e) Approval and Closing: Once approved, the lender will finalize the loan terms, and borrowers must sign the necessary documents, including the Chattel Mortgage agreement. 5. Benefits of West Virginia Chattel Mortgage on Mobile Home: a) Access to Financing: Enables individuals to purchase or refinance a mobile home when traditional home loans are not applicable. b) Quick Processing: Chattel Mortgages typically have a streamlined approval process, allowing borrowers to access funds faster. c) Flexible Loan Terms: Lenders may offer various repayment terms, allowing borrowers to customize the mortgage to suit their financial situation. d) Lower Down Payments: Chattel Mortgages often require comparatively lower down payments, making home purchase or refinancing more accessible. 6. Legal Aspects of West Virginia Chattel Mortgage on Mobile Home: a) Legal Ownership: Until the loan is fully repaid, the lender retains temporary ownership rights over the mobile home. b) Promissory Note: Borrowers must sign a promissory note, legally binding them to repay the loan. c) Chattel Mortgage Agreement: This document outlines the terms, conditions, and obligations of the lender and borrower regarding the Chattel Mortgage. Conclusion: Understanding West Virginia Chattel Mortgage on Mobile Home is crucial when considering buying or refinancing a mobile home in the state. By leveraging this financing option, individuals can secure the funds needed to achieve their homeownership goals. Whether it's purchasing a new mobile home or accessing equity, a Chattel Mortgage offers flexibility, convenience, and expedited loan processing.

West Virginia Chattel Mortgage on Mobile Home

Description

How to fill out West Virginia Chattel Mortgage On Mobile Home?

You may commit time online looking for the authorized file design which fits the state and federal specifications you require. US Legal Forms supplies a huge number of authorized forms which are evaluated by professionals. It is simple to down load or printing the West Virginia Chattel Mortgage on Mobile Home from my support.

If you have a US Legal Forms accounts, you can log in and click on the Download switch. After that, you can full, modify, printing, or indicator the West Virginia Chattel Mortgage on Mobile Home. Every authorized file design you buy is your own for a long time. To have one more duplicate for any bought kind, check out the My Forms tab and click on the related switch.

If you are using the US Legal Forms web site for the first time, follow the simple directions beneath:

- Initial, be sure that you have selected the right file design for that county/town of your liking. Read the kind outline to make sure you have picked the proper kind. If available, take advantage of the Preview switch to appear from the file design as well.

- If you wish to locate one more variation in the kind, take advantage of the Search field to discover the design that fits your needs and specifications.

- Upon having located the design you need, just click Buy now to continue.

- Pick the prices prepare you need, key in your credentials, and register for a merchant account on US Legal Forms.

- Complete the deal. You may use your bank card or PayPal accounts to cover the authorized kind.

- Pick the file format in the file and down load it to your product.

- Make changes to your file if possible. You may full, modify and indicator and printing West Virginia Chattel Mortgage on Mobile Home.

Download and printing a huge number of file templates using the US Legal Forms site, which offers the biggest variety of authorized forms. Use expert and status-certain templates to take on your company or person needs.