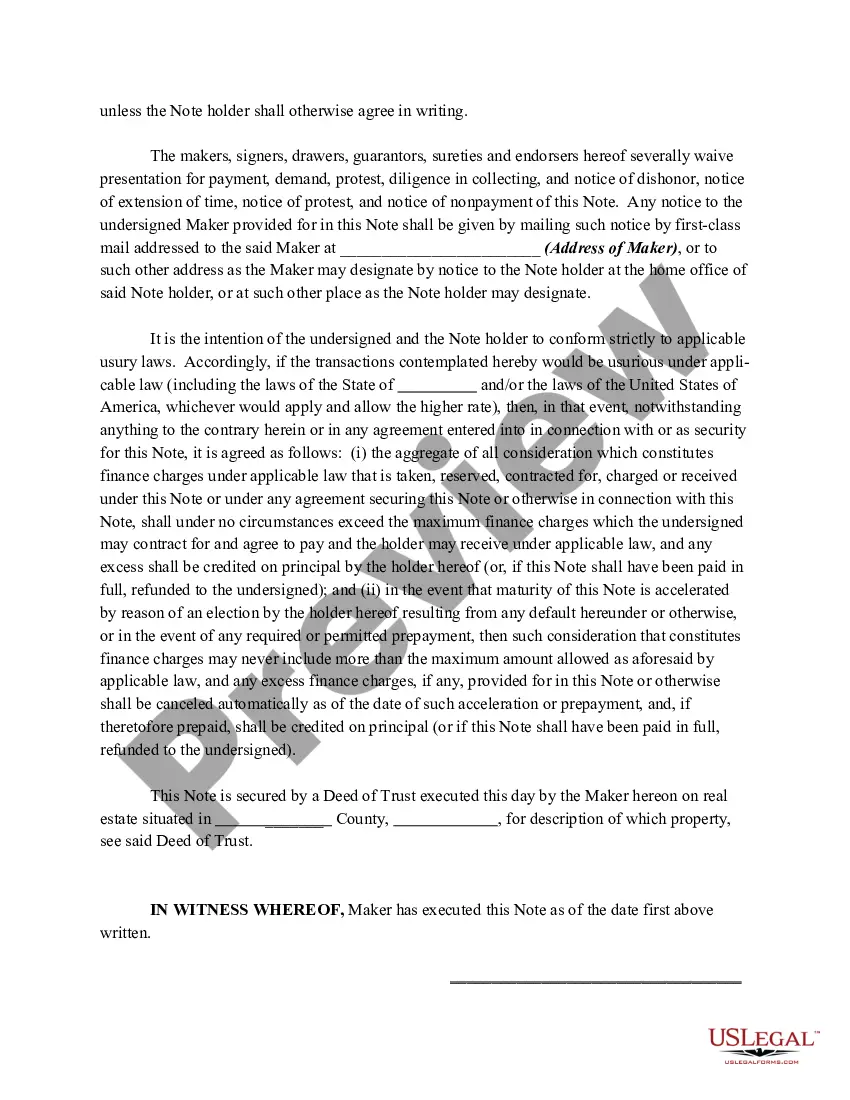

A West Virginia Promissory Note — Balloon Note is a legally binding document that outlines a borrower's promise to repay a loan with a large lump sum payment at the end of the loan term. This type of promissory note is commonly used in situations where the borrower needs a lower monthly payment for a certain period, but can afford a larger final payment. The West Virginia Promissory Note — Balloon Note typically includes essential information such as the names and contact details of the borrower and lender, the principal amount of the loan, the interest rate, the loan term, and the repayment schedule. It also includes provisions for late fees, prepayment penalties, and any additional terms agreed upon by the parties involved. There are various types of West Virginia Promissory Note — Balloon Notes, including: 1. Residential Balloon Note: This type of promissory note is used for residential mortgages, where the borrower has a lower monthly payment during the term of the loan, but must make a larger balloon payment at the end. This allows borrowers to manage their finances more easily during the loan term. 2. Business Balloon Note: This type of promissory note is used for business loans, where the borrower may need additional cash flow for a specific period. The borrower makes smaller monthly payments, with a larger balloon payment due at the end of the loan term. This type of note enables businesses to invest in growth opportunities while keeping their monthly expenses lower. 3. Agricultural Balloon Note: This specific type of balloon note is used for agricultural loans. Farmers and agricultural businesses often experience seasonal income fluctuations, so the balloon note allows them to make smaller payments during low-income periods and a larger payment when their income is higher. It is crucial to consult with legal professionals or financial advisors to ensure compliance with West Virginia state laws when drafting or using a West Virginia Promissory Note — Balloon Note. The terms and conditions of the note should be agreed upon and signed by both parties involved to ensure the enforceability of the agreement.

West Virginia Promissory Note - Balloon Note

Description

How to fill out West Virginia Promissory Note - Balloon Note?

It is feasible to spend hours online attempting to locate the legal document template that fits both state and federal requirements you will require.

US Legal Forms provides thousands of legal forms that are validated by experts.

You have the option to download or print the West Virginia Promissory Note - Balloon Note from my services.

If available, use the Review button to preview the document format as well.

- If you already possess a US Legal Forms account, you can Log In and click the Download button.

- Then, you can complete, amend, print, or sign the West Virginia Promissory Note - Balloon Note.

- Every legal document format you obtain is yours permanently.

- To get an additional copy of the purchased form, go to the My documents tab and click the respective button.

- If you are using the US Legal Forms site for the first time, follow the straightforward instructions below.

- First, ensure you have selected the correct document format for the location/region of your choice.

- Review the form outline to confirm you have chosen the right type.

Form popularity

FAQ

To legalize a promissory note, you typically need to ensure it is signed by both parties and adheres to state laws, including any necessary witnesses or notary requirements. In a West Virginia Promissory Note - Balloon Note, following these steps is crucial for validation and enforceability. You may want to consult with legal professionals to confirm that your document meets all legal criteria. Resources at USLegalForms can help you navigate this process smoothly.

A key disadvantage of balloon payments is the financial burden they place on borrowers at the end of the term. With a West Virginia Promissory Note - Balloon Note, the large final payment can lead to stress or even default if you lack the necessary funds. This can cause borrowers to rethink their financial strategies or seek alternative financing arrangements. Planning ahead is essential to mitigate this disadvantage.

To claim a promissory note, you must present the original document to the borrower and request payment. A West Virginia Promissory Note - Balloon Note allows for a legal process to enforce repayment if necessary. In cases of default, you may need to seek legal advice to initiate collection procedures. Platforms like USLegalForms can guide you through your options for claiming or enforcing your promissory note.

The major problem with balloon payments is the risk of facing a large final payment that the borrower may not be able to afford. This situation often arises in a West Virginia Promissory Note - Balloon Note, which can lead to financial strain if proper budgeting isn't in place. Additionally, borrowers might encounter difficulties securing refinancing options when they cannot make the balloon payment. This underscores the importance of evaluating your financial situation carefully.

Balloon payment examples often include auto loans or mortgages that feature a significant payment at the conclusion of the term. For instance, if your West Virginia Promissory Note - Balloon Note specifies monthly payments of $500, you might owe a final payment of $20,000 at the end of five years. This setup can be appealing for those seeking lower payments until the end, but it requires careful planning. Always calculate your ability to make that final payment before committing.

The enforceability of a promissory note, including the West Virginia Promissory Note - Balloon Note, typically depends on its terms and the parties involved. A properly written and signed note is generally enforceable in a court of law. If either party defaults on their obligations, the other may seek legal remedies. For clarity and security, consider using platforms like USLegalForms, which provide templates and guidance for creating enforceable promissory notes.

In West Virginia, the statute of limitations for a promissory note is generally five years. This means you have a five-year period to enforce the terms of your West Virginia Promissory Note - Balloon Note through legal action. If this time frame expires, it may become challenging to collect on the note. Therefore, it is crucial to address any payment issues promptly to protect your rights.

To obtain a West Virginia Promissory Note - Balloon Note, you can utilize online services that specialize in legal document creation. One reliable option is US Legal Forms, which offers customizable templates suited to your specific needs. Simply choose the appropriate form, fill in the necessary details, and download your document. This streamlined process ensures you receive a legally sound promissory note quickly.

Interesting Questions

More info

This free Search LendingTree and also help you find the right credit card loan, finance credit cards, home loans, small business loans or any other loans for your personal or business. LendingTree also find some of the most reputable lenders in the world and give them FREE access to the lenders' data. So you can search them directly on your home page without any restrictions.