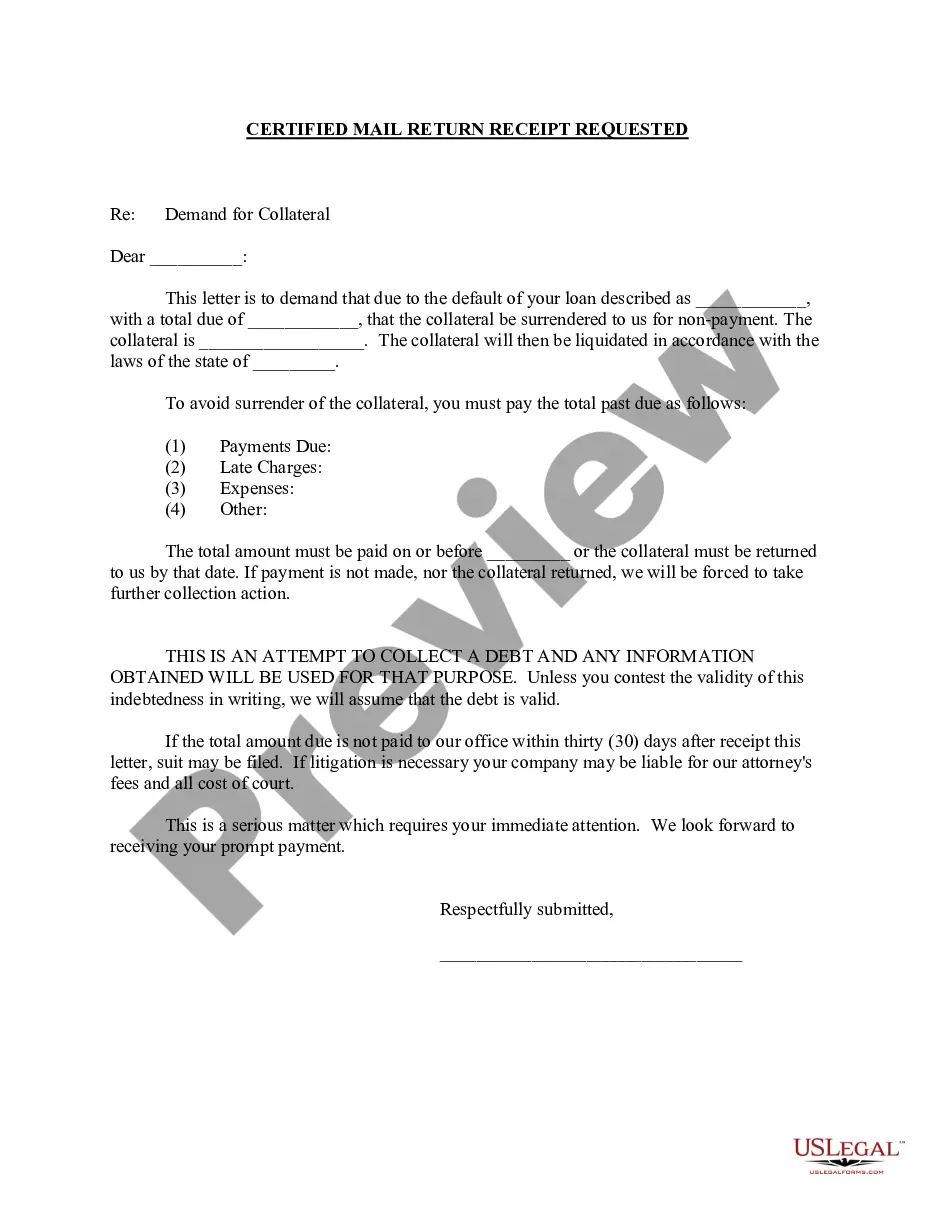

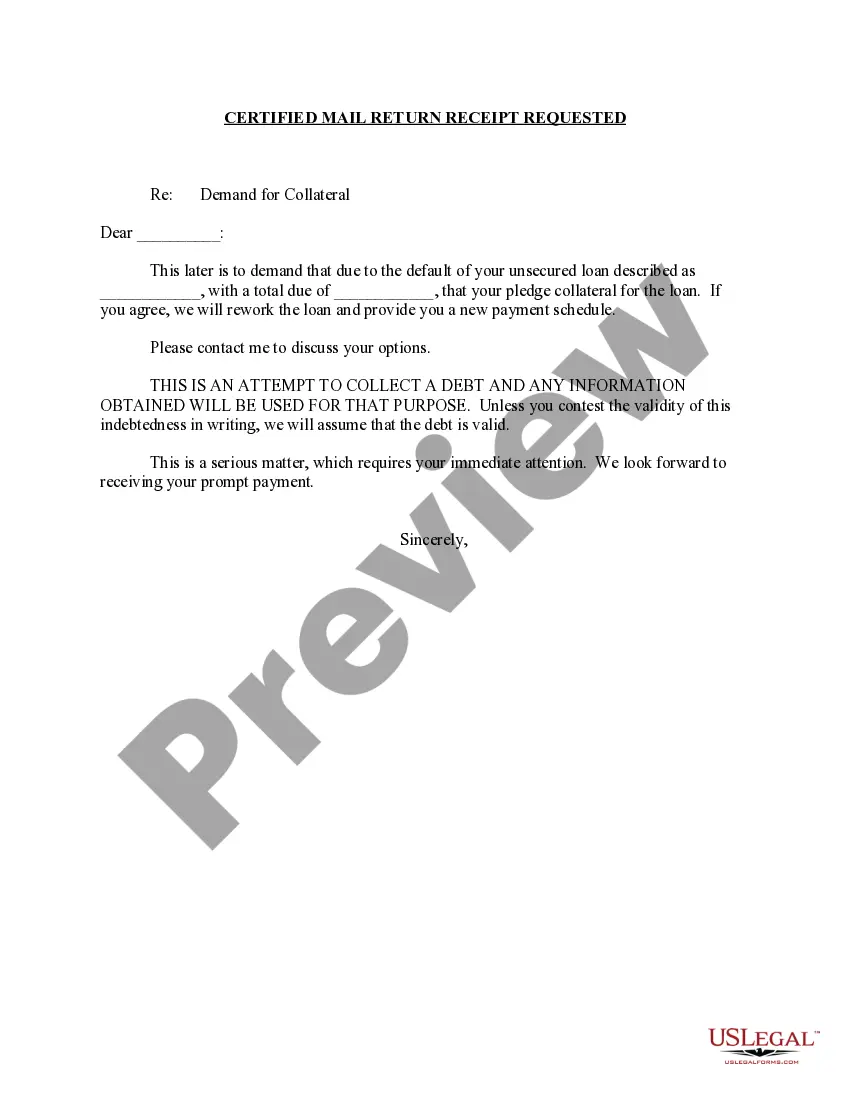

West Virginia's Demand for Collateral by Creditor refers to a legal process in which a creditor requests collateral from a debtor to secure the repayment of a debt. This demand is made as a form of safeguard for the creditor in case the debtor defaults on their loan or fails to fulfil their financial obligations. Under West Virginia law, there are various types of demand for collateral by creditors, including: 1. Security Agreement: A security agreement is a written contract between the debtor and creditor that outlines the terms and conditions of the collateral provided. It establishes the creditor's right to claim the collateral if the debtor fails to repay the loan. 2. UCC Financing Statement: The Uniform Commercial Code (UCC) requires the filing of a financing statement with the Secretary of State's office in West Virginia. This statement provides public notice of the creditor's interest in the collateral, allowing other parties to be aware of the creditor's rights. 3. Lien: A lien is a legal claim or right that the creditor has over the debtor's property until the debt is repaid. If the debtor defaults, the creditor may enforce the lien and seize the collateral to satisfy the debt. 4. Repossession: In cases where the debtor fails to repay the loan, the creditor can exercise their right to repossess the collateral. This typically involves physically taking possession of the property, such as a vehicle or equipment. It is important for both debtors and creditors in West Virginia to understand the implications and legalities of demand for collateral. Debtors must carefully consider the collateral they provide, understanding that it may be subject to seizure in case of default. Creditors, on the other hand, must follow proper legal procedures and respect the rights of the debtors when demanding collateral. In summary, West Virginia's Demand for Collateral by Creditor is a legal process that allows creditors to request collateral from debtors as security for repayment. The various types of demand include security agreements, UCC financing statements, liens, and repossession. Both debtors and creditors must be well-informed about these procedures to ensure fair and lawful enforcement of debt obligations.

West Virginia Demand for Collateral by Creditor

Description

How to fill out West Virginia Demand For Collateral By Creditor?

Are you presently in a placement that you need documents for possibly organization or person reasons virtually every working day? There are a lot of lawful document layouts available online, but getting ones you can depend on is not easy. US Legal Forms offers 1000s of type layouts, like the West Virginia Demand for Collateral by Creditor, which are created to satisfy federal and state specifications.

When you are currently informed about US Legal Forms web site and have your account, just log in. After that, you are able to download the West Virginia Demand for Collateral by Creditor template.

If you do not offer an profile and want to start using US Legal Forms, abide by these steps:

- Get the type you need and make sure it is for the right area/area.

- Take advantage of the Preview key to review the form.

- Read the explanation to ensure that you have selected the right type.

- If the type is not what you are trying to find, make use of the Lookup field to get the type that meets your requirements and specifications.

- Whenever you discover the right type, simply click Purchase now.

- Opt for the prices program you would like, fill in the required details to make your money, and purchase the order making use of your PayPal or Visa or Mastercard.

- Pick a handy paper structure and download your copy.

Find all of the document layouts you might have purchased in the My Forms menus. You can get a more copy of West Virginia Demand for Collateral by Creditor at any time, if required. Just click the essential type to download or printing the document template.

Use US Legal Forms, the most extensive selection of lawful varieties, to save efforts and prevent blunders. The assistance offers expertly created lawful document layouts which can be used for a range of reasons. Create your account on US Legal Forms and initiate generating your way of life a little easier.