A home equity line of credit is a form of revolving credit in which your home serves as collateral. Because the home is likely to be a consumer's largest asset, many homeowners use their credit lines only for major items such as education, home improvements, or medical bills and not for day-to-day expenses. A home equity line of credit differs from a conventional home equity loan in that the borrower is not advanced the entire sum up front, but uses a line of credit to borrow sums that total no more than the amount, similar to a credit card.

Another important difference from a conventional loan is that the interest rate on a home equity line of credit is variable based on an index such as prime rate. This means that the interest rate can - and almost certainly will - change over time. The margin is the difference between the prime rate and the interest rate the borrower will actually pay.

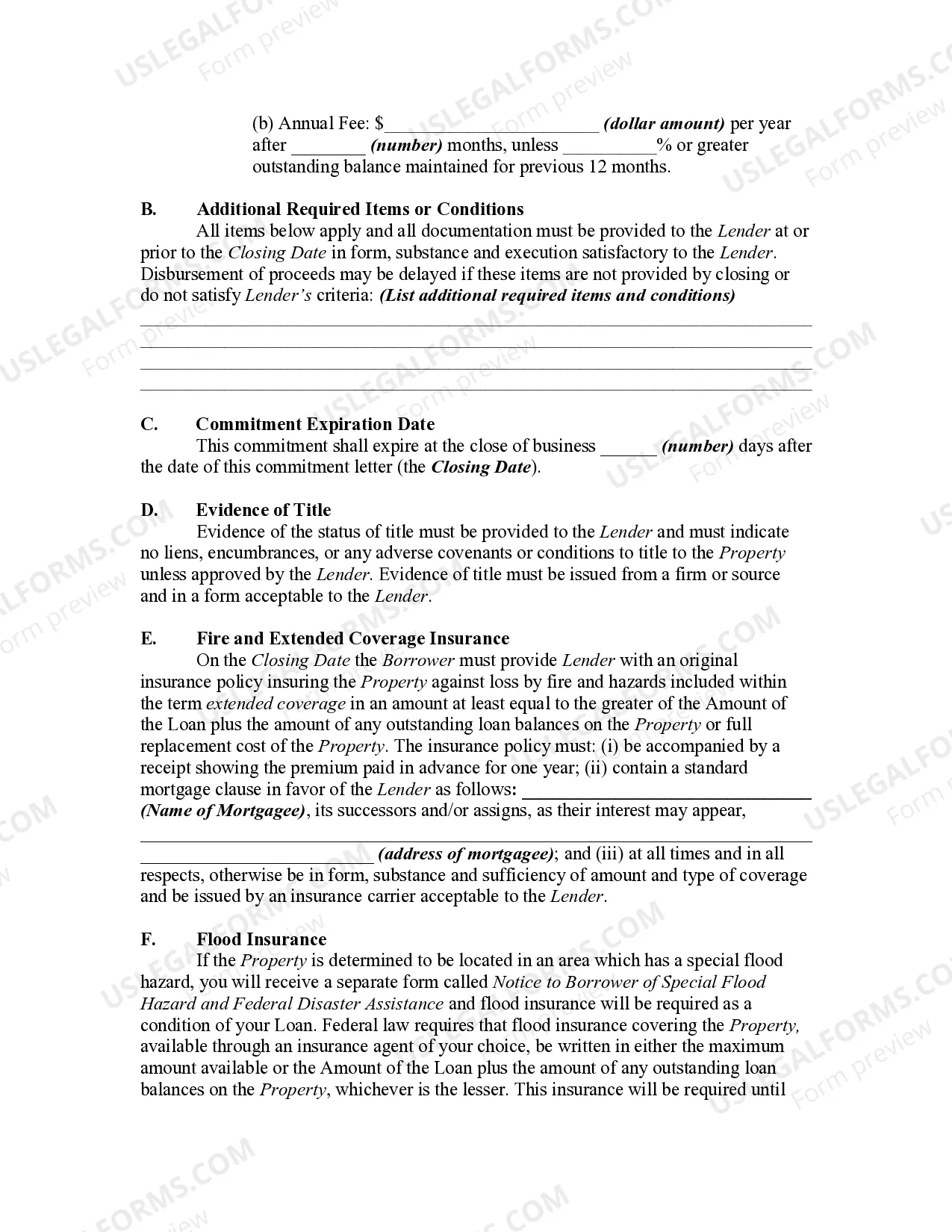

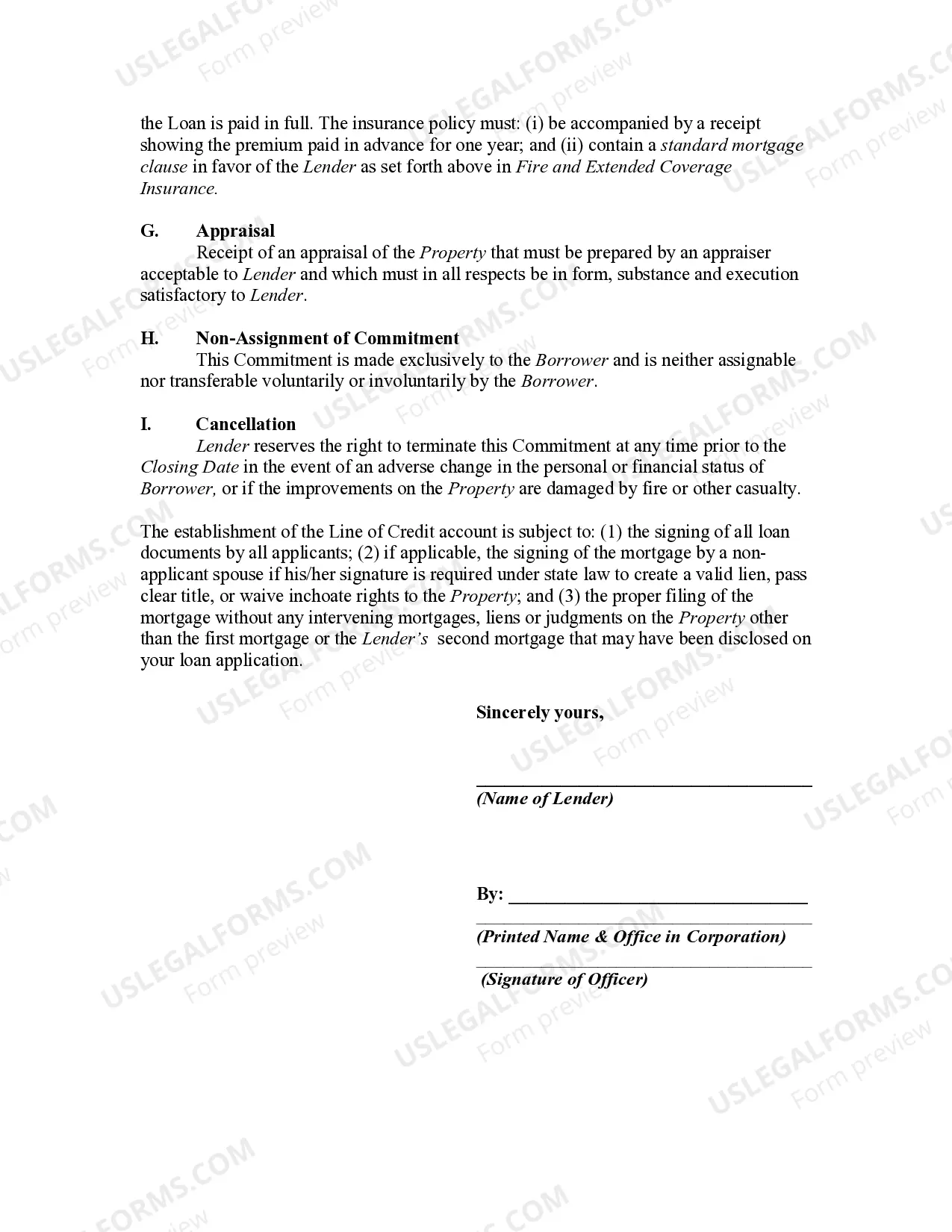

A West Virginia Mortgage Loan Commitment for a Home Equity Line of Credit (HELOT) is a binding agreement between a borrower and a lender that outlines the terms and conditions for accessing funds from the equity built within a property for various purposes such as home improvements, debt consolidation, or emergency expenses. This commitment, issued by the lender, serves as a guarantee of approval, allowing the borrower to secure a credit line based on the appraised value of their home. One of the main advantages of a HELOT is that it provides homeowners with a flexible and convenient way to access funds, as well as potentially lower interest rates compared to other forms of credit. The West Virginia Mortgage Loan Commitment for a HELOT offers several types to suit different financial needs and situations: 1. Fixed-Rate Home Equity Line of Credit: This type of commitment allows the borrower to access a fixed amount of funds at a fixed interest rate for the duration of the loan term. It provides stability and predictability in payment amounts, making it suitable for homeowners who prefer budgeting consistency. 2. Adjustable-Rate Home Equity Line of Credit: With this commitment, the interest rate fluctuates based on the market conditions, which can result in either lower or higher payments over time. This option may be ideal for borrowers who anticipate paying off the loan or require funds for short-term needs. 3. Combination Line of Credit: This commitment offers borrowers the option to split their loan into multiple portions, each with its own distinct interest rate and terms. This flexibility allows the borrower to tailor their financing strategy based on specific financial goals. Moreover, West Virginia Mortgage Loan Commitments for a HELOT commonly come with additional features like interest-only payments during the draw period and the option to convert the line of credit into a fixed-rate loan later on. These options provide borrowers with even more flexibility and control over their finances. Ultimately, a West Virginia Mortgage Loan Commitment for a Home Equity Line of Credit empowers homeowners to leverage the equity in their property to access funds for various purposes, helping them achieve their financial goals while enjoying the benefits of homeownership.