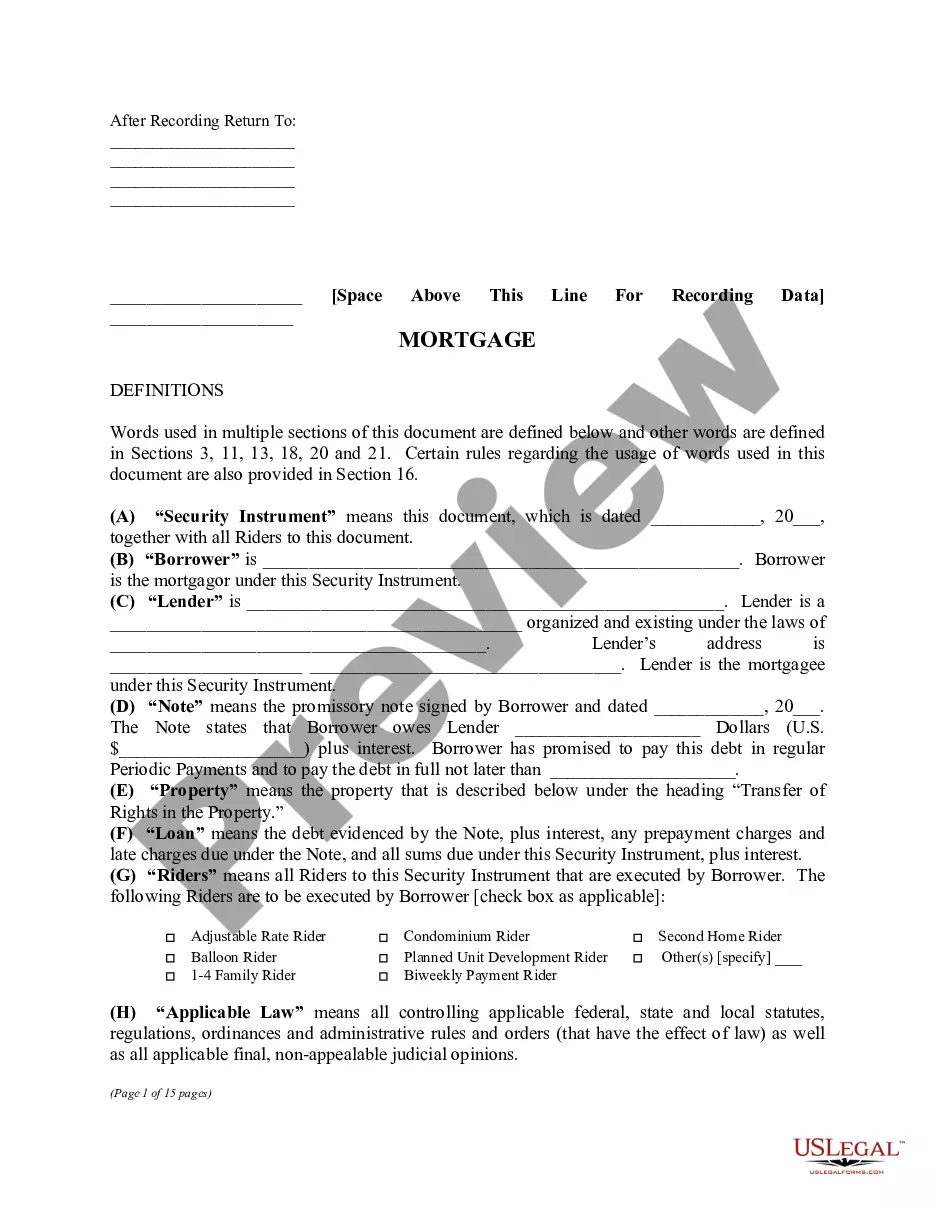

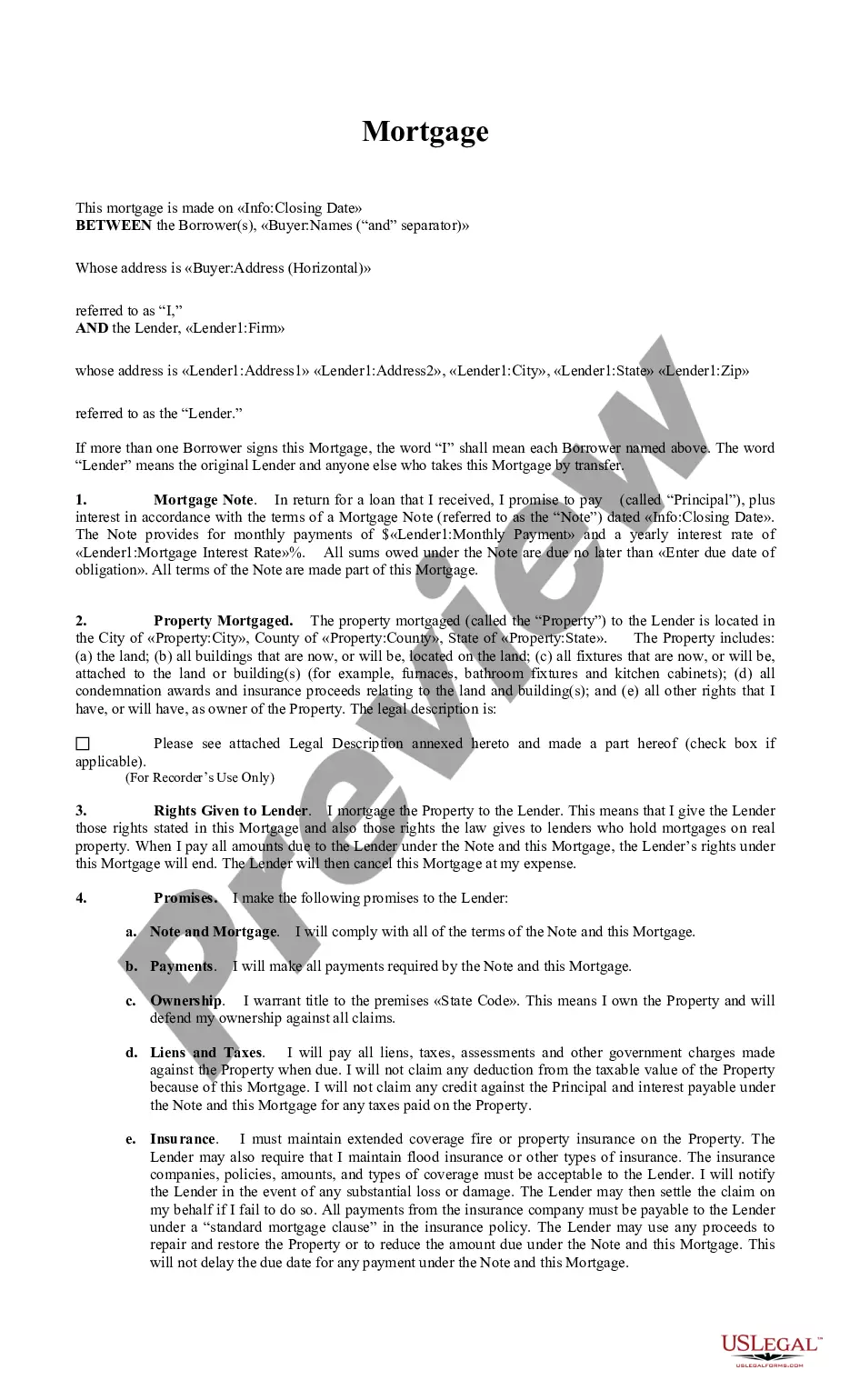

A reverse mortgage is a loan from the U.S. Government for 50% to 75% of the value of a home owned by a homeowner aged 62 and older. Instead of making monthly payments to a lender, as with a regular mortgage, a lender makes payments to the homeowner. The funds from a reverse mortgage are tax-free. The loan doesn't have to be repaid in the homeowner's lifetime, however, when the homeowner dies, the money received plus approximately 4% interest is repaid by their estate. The loan is repaid when the homeowner ceases to occupy the home as a principal residence, due to the homeowner (the last remaining spouse, in cases of couples) passing away, selling the home, or permanently moving out.

West Virginia Home Equity Conversion Mortgage - Reverse Mortgage

State:

Multi-State

Control #:

US-01685BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Home Equity Conversion Mortgage - Reverse Mortgage?

Locating the correct authentic document template can be a challenge.

Certainly, there are numerous templates accessible online, but how can you find the authentic form you require.

Utilize the US Legal Forms website. The platform offers an extensive collection of templates, such as the West Virginia Home Equity Conversion Mortgage - Reverse Mortgage, which can be utilized for both business and personal purposes.

You can preview the form using the Review button and examine the form details to confirm it is suitable for your needs. If the form does not meet your specifications, use the Search field to locate the appropriate form. Once you are confident that the form is suitable, click on the Get now button to obtain the form. Select the pricing plan you prefer and provide the necessary information. Create your account and pay for your order using your PayPal account or credit card. Choose the document format and download the legitimate document template to your device. Complete, modify, print, and sign the acquired West Virginia Home Equity Conversion Mortgage - Reverse Mortgage. US Legal Forms boasts the largest collection of legitimate forms where you can find a variety of document templates. Use the service to download professionally-crafted documents that comply with state regulations.

- All of the forms are reviewed by professionals and comply with federal and state regulations.

- If you are already registered, sign in to your account and click the Download button to access the West Virginia Home Equity Conversion Mortgage - Reverse Mortgage.

- Use your account to search for the legitimate forms you have acquired previously.

- Navigate to the My documents section of your account to retrieve another copy of the document you need.

- If you are a new user of US Legal Forms, here are simple instructions for you to follow.

- First, ensure you have selected the correct form for your city/region.

Form popularity

FAQ

A Home Equity Conversion Mortgage (HECM), the most common type of reverse mortgage, is a special type of home loan only for homeowners who are 62 and older. This information only applies to Home Equity Conversion Mortgages (HECMs), which are the most common type of reverse mortgage loans.

A traditional private reverse mortgage is not necessarily backed by the federal government, whereas an HECM is not only underwritten by HUD, it is also regulated to consumer safety by the federal government as well. This allows interest rates charged to be far lower.

Generally speaking, you can usually get somewhere between 40% to 60% of your home's appraised value. And the higher your home value is, the more money you can potentially access.

Reverse mortgages represent one way to get the equity out of your home, but they aren't the only way. If you don't qualify for a reverse mortgage but still want to turn your equity to cash, there are options that you can consider.

If borrowers run out of available funds, they can stay in the house, provided they continue to live in and maintain it and stay current on required taxes and insurance. In this sense, they will not have outlived the mortgage, but they will have outlived their ability to borrow more money from it.

Cons of HECM You have to live in your home: When you get a HECM, your property must be your principal residence for much of the year. You'll have to pay back the HECM if you sell the home or want to move.

Reverse Mortgage Loan Limits For the government-insured Home Equity Conversion Mortgage (HECM), the maximum reverse mortgage limit you can borrow against is $1,089,300 (updated January 1st, 2023), even if your home is appraised at a higher value than that.

Whether you have a conventional or reverse mortgage, you always risk losing your home if you don't meet loan obligations. With a traditional mortgage, the typical way that a borrower defaults on the loan is if they don't make monthly payments.