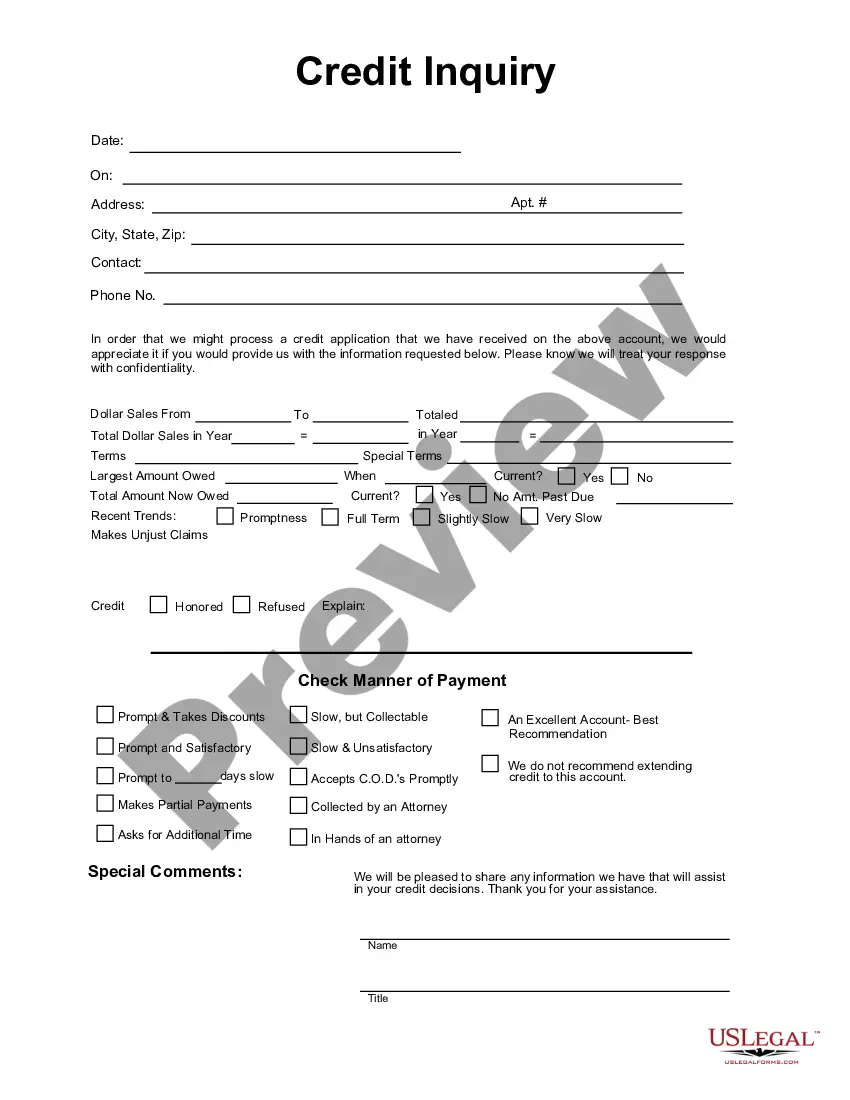

West Virginia Credit Inquiry: A Comprehensive Overview of Credit Inquiries in West Virginia In the realm of personal finance, understanding credit inquiries is crucial to maintaining a healthy credit score and financial well-being. Credit inquiries refer to the process by which lenders and creditors assess an individual's creditworthiness before granting credit or loan applications. In the state of West Virginia, credit inquiries play a vital role in determining an individual's eligibility for various financial services. This detailed description will delve into the concept of West Virginia Credit Inquiry and shed light on its different types and implications. Types of West Virginia Credit Inquiries: 1. Hard Credit Inquiries: A hard credit inquiry occurs when a financial institution, such as a bank or credit card company, reviews an individual's credit report to make a lending decision. Generally, applying for a new loan, credit card, or mortgage initiates a hard credit inquiry. Each hard inquiry can slightly impact an individual's credit score and remains on their credit report for two years. 2. Soft Credit Inquiries: Soft credit inquiries, on the other hand, have no impact on an individual's credit score. These inquiries occur when someone, such as an employer or landlord, checks an individual's credit report for background verification purposes. Soft credit inquiries are not related to credit applications and are often initiated without the individual's explicit consent. 3. Promotional Credit Inquiries: Promotional inquiries, also known as pre-screened offers, are initiated by credit card issuers or other financial institutions. These inquiries occur when institutions pre-approve individuals for credit offers based on their credit profiles. Although these inquiries are soft and won't harm credit scores, they may still show up in credit reports. Credit Inquiry Regulations and Protections in West Virginia: West Virginia law adheres to the Fair Credit Reporting Act (FCRA), a federal legislation that regulates credit reporting agencies (Crash) and protects consumers' rights. The FCRA requires Crash to provide accurate and fair credit reports, ensuring the privacy and protection of consumer information. Moreover, West Virginia residents benefit from additional state-level protections. The West Virginia Credit and Consumer Protection Act regulations provide safeguards against unauthorized inquiries and identity theft. This act allows individuals to place a security freeze on their credit reports, preventing unauthorized entities from accessing their credit information without consent. Implications of Credit Inquiries: It is important for West Virginia residents to be aware of the potential impact credit inquiries can have on their credit scores. While a single hard inquiry may only have a minimal effect, multiple recent inquiries within a short span of time can negatively impact a credit score. This is because it suggests a higher risk of credit-seeking behavior. To mitigate any negative effects, it is advisable to limit credit applications to essential ones and space them out over time. It is also prudent to regularly monitor credit reports for accuracy and promptly dispute any erroneous inquiries. In conclusion, understanding West Virginia Credit Inquiry is crucial for maintaining a healthy credit score and safeguarding personal financial interests. West Virginia residents should familiarize themselves with the different types of inquiries, such as hard, soft, and promotional, as well as the regulations and protections in place. By staying informed and proactive, individuals can make informed credit decisions and protect their financial well-being.

West Virginia Credit Inquiry

Description

How to fill out West Virginia Credit Inquiry?

Discovering the right lawful papers design could be a have a problem. Obviously, there are plenty of themes available on the net, but how would you get the lawful kind you need? Use the US Legal Forms website. The services delivers thousands of themes, such as the West Virginia Credit Inquiry, which can be used for organization and private requires. All the types are checked out by specialists and satisfy state and federal demands.

When you are presently signed up, log in to your profile and click on the Download switch to have the West Virginia Credit Inquiry. Make use of profile to appear through the lawful types you have ordered formerly. Check out the My Forms tab of your own profile and acquire one more copy from the papers you need.

When you are a brand new consumer of US Legal Forms, allow me to share basic directions for you to comply with:

- Very first, ensure you have chosen the correct kind for your personal town/state. It is possible to look over the shape while using Review switch and read the shape description to ensure this is the right one for you.

- When the kind will not satisfy your needs, make use of the Seach discipline to get the proper kind.

- When you are sure that the shape is acceptable, click the Acquire now switch to have the kind.

- Select the pricing strategy you desire and type in the required information and facts. Create your profile and purchase the order using your PayPal profile or Visa or Mastercard.

- Select the data file structure and download the lawful papers design to your product.

- Full, change and printing and sign the attained West Virginia Credit Inquiry.

US Legal Forms is definitely the biggest collection of lawful types that you can see numerous papers themes. Use the service to download appropriately-manufactured papers that comply with state demands.