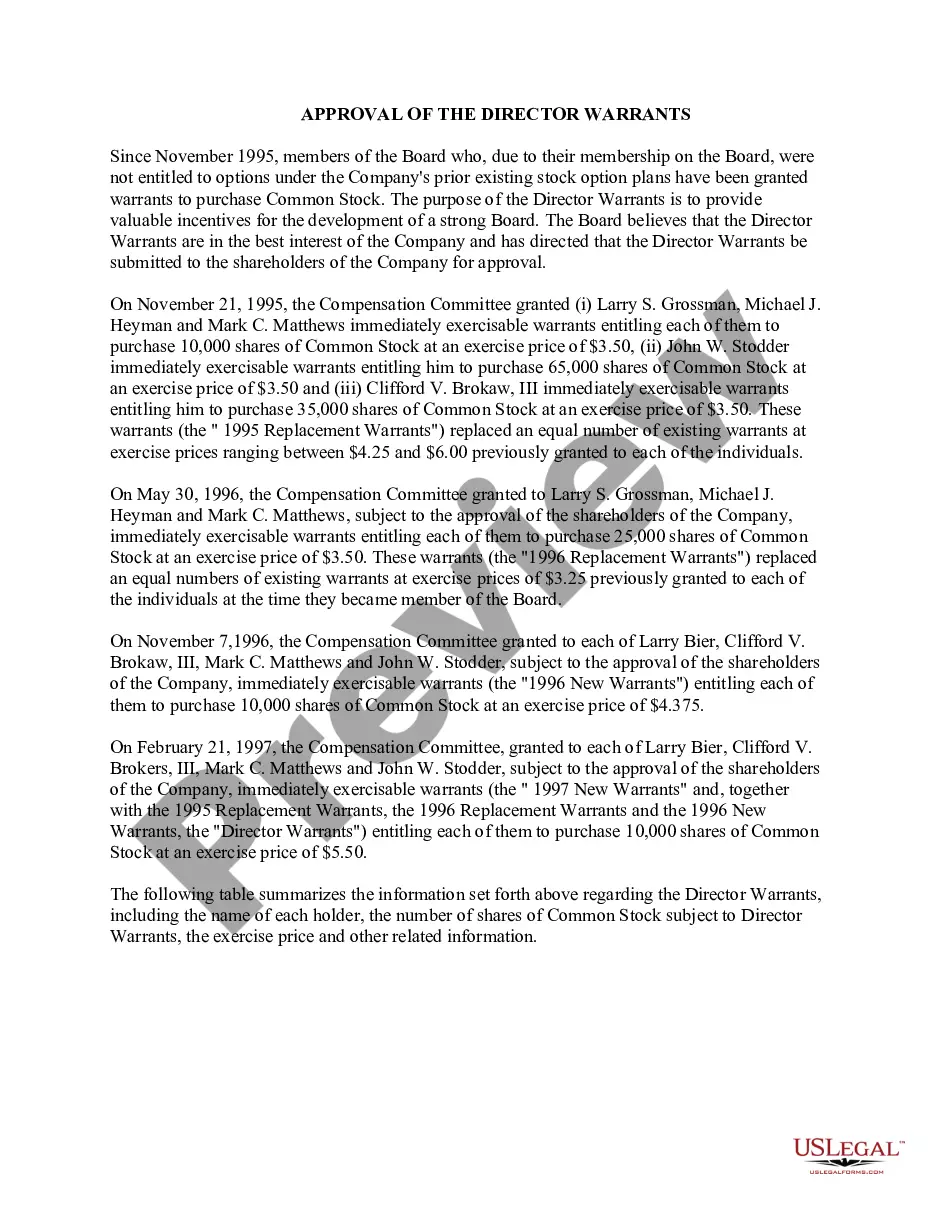

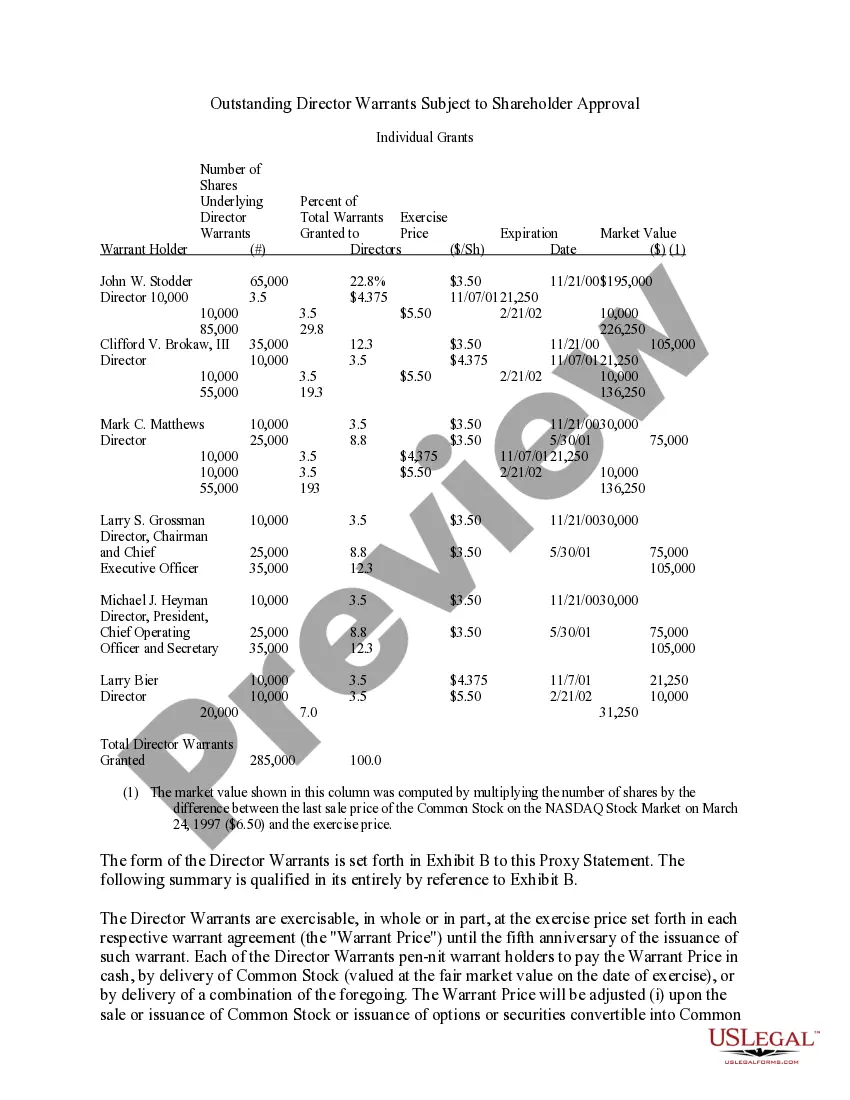

West Virginia Approval of Director Warrants: A Comprehensive Analysis of Different Types and Key Considerations West Virginia director warrants hold significant importance in the corporate realm, serving as a method of acknowledging and compensating directors for their hard work, dedication, and contributions to the organization. This detailed description seeks to provide an in-depth analysis of West Virginia Approval of director warrants, shedding light on various types and key considerations associated with them. 1. Definition and Purpose: Director warrants refer to the authorized rights granted to directors of a corporation, allowing them to purchase a specific number of company shares at a predetermined price within a specified timeframe. Essentially, director warrants serve to incentivize directors to align their interests with those of the shareholders, encouraging effective management and long-term value creation. 2. Types of West Virginia Approval of Director Warrants: a) Non-Qualified Director Warrants: Non-qualified director warrants are deemed as taxable compensation for the director. They are subject to federal income tax withholding and require the corporation to report the value of the warrants as income for the director. These warrants do not meet the qualification criteria outlined by the Internal Revenue Service (IRS). b) Incentive Director Warrants: Incentive director warrants, also known as qualified warrants, are structured to meet specific IRS guidelines, allowing for favorable tax treatment. Directors who exercise incentive warrants may qualify for long-term capital gains tax rates, generally less than ordinary income tax rates. c) Restricted Director Warrants: Restricted director warrants come with certain limitations or conditions placed on their exercise. These restrictions may include a specified vesting period, performance goals, or limitations on transferability. The purpose of restrictions is to ensure that directors actively contribute to the growth and success of the corporation during the stated timeframe. 3. Key Considerations: a) Board Approval: The issuance of director warrants requires the approval of the board of directors. A detailed resolution or agreement must be passed, outlining the terms and conditions of the warrant grants. It is crucial to ensure that all legal requirements, such as disclosure and fiduciary duties, are duly considered during the approval process. b) Exercise Price and Term: The exercise price of director warrants should be set at fair market value and must be explicitly stated in the warrant agreement. The term signifies the duration within which a director can exercise their warrants. Careful consideration should be given to strike a balance between encouraging long-term commitment and providing flexibility for future director appointments. c) Vesting Schedule: A vesting schedule determines when directors can exercise their warrants. It is essential to align the vesting period with the corporation's goals, objectives, and long-term strategies. Common vesting schedules include time-based vesting (cliff or graduated) and performance-based vesting tied to predetermined goals. d) Tax Implications: Directors must be aware of the tax implications associated with warrant exercises. Non-qualified warrants may result in immediate taxation, while qualified warrants offer potential tax advantages. Engaging tax professionals is recommended to navigate the complexities and optimize tax strategies. In conclusion, West Virginia Approval of Director Warrants plays a pivotal role in incentivizing directors and aligning their interests with the corporation's shareholders. By understanding the types of director warrants and key considerations associated with their approval, corporations can effectively design compensation mechanisms that promote sustainable growth, productivity, and shareholder value.

West Virginia Approval of director warrants

Description

How to fill out West Virginia Approval Of Director Warrants?

US Legal Forms - among the biggest libraries of legitimate varieties in the United States - provides a wide range of legitimate file web templates you may down load or print out. Utilizing the site, you may get a large number of varieties for company and specific functions, sorted by classes, states, or search phrases.You can find the most up-to-date types of varieties such as the West Virginia Approval of director warrants within minutes.

If you already have a membership, log in and down load West Virginia Approval of director warrants from the US Legal Forms local library. The Acquire key can look on every single type you look at. You have access to all formerly saved varieties inside the My Forms tab of your accounts.

If you wish to use US Legal Forms for the first time, listed below are easy recommendations to obtain started off:

- Be sure to have chosen the correct type for your personal city/area. Click the Preview key to analyze the form`s content material. Browse the type outline to actually have selected the proper type.

- In the event the type doesn`t suit your needs, make use of the Look for area on top of the display to get the one that does.

- If you are happy with the shape, confirm your option by simply clicking the Get now key. Then, select the prices strategy you prefer and supply your qualifications to sign up on an accounts.

- Procedure the purchase. Use your credit card or PayPal accounts to perform the purchase.

- Choose the file format and down load the shape on your own system.

- Make modifications. Complete, modify and print out and sign the saved West Virginia Approval of director warrants.

Every template you included in your account lacks an expiration time and is also the one you have for a long time. So, if you would like down load or print out yet another copy, just check out the My Forms segment and click on around the type you will need.

Gain access to the West Virginia Approval of director warrants with US Legal Forms, probably the most substantial local library of legitimate file web templates. Use a large number of professional and state-certain web templates that meet your company or specific requires and needs.

Form popularity

FAQ

- A party against whom a claim, counterclaim, or cross-claim is asserted or a declaratory judgment is sought may, at any time, move with or without supporting affidavits for a summary judgment in the party's favor as to all or any part thereof.

§62-1D-3. Interception of communications generally. §62-1D-4. Manufacture, possession or sale of intercepting device.

The Legislature shall provide for the support of free schools by appropriating thereto the interest of the invested "School Fund," the net proceeds of all forfeitures and fines accruing to this state under the laws thereof and by general taxation of persons and property or otherwise.

West Virginia is governed under its second and current constitution, which dates from 1872. The document includes fourteen articles and several amendments.

West Virginia's constitution, however, did not have a preamble until 1960. In addition to the principle of federalism, the West Virginia constitution is based on the democratic principles of sovereignty, limited government, separation of powers, and checks and balances.

The Legislature shall foster and encourage, moral, intellectual, scientific and agricultural improvement; it shall, whenever it may be practicable, make suitable provision for the blind, mute and insane, and for the organization of such institutions of learning as the best interests of general education in the state ...

Section 12. Freedom of speech and of the press; right peaceably to assemble, and to petition. Section 13. Militia; standing armies; military subordinate to civil power.

West Virginia is a one-party consent state when it comes to audio recording, meaning that if you intend on recording a conversation, at least one person in the conversation must consent for the recording to be legal [1]. If you're a participant in a conversation, you can be the one person to consent to the recording.