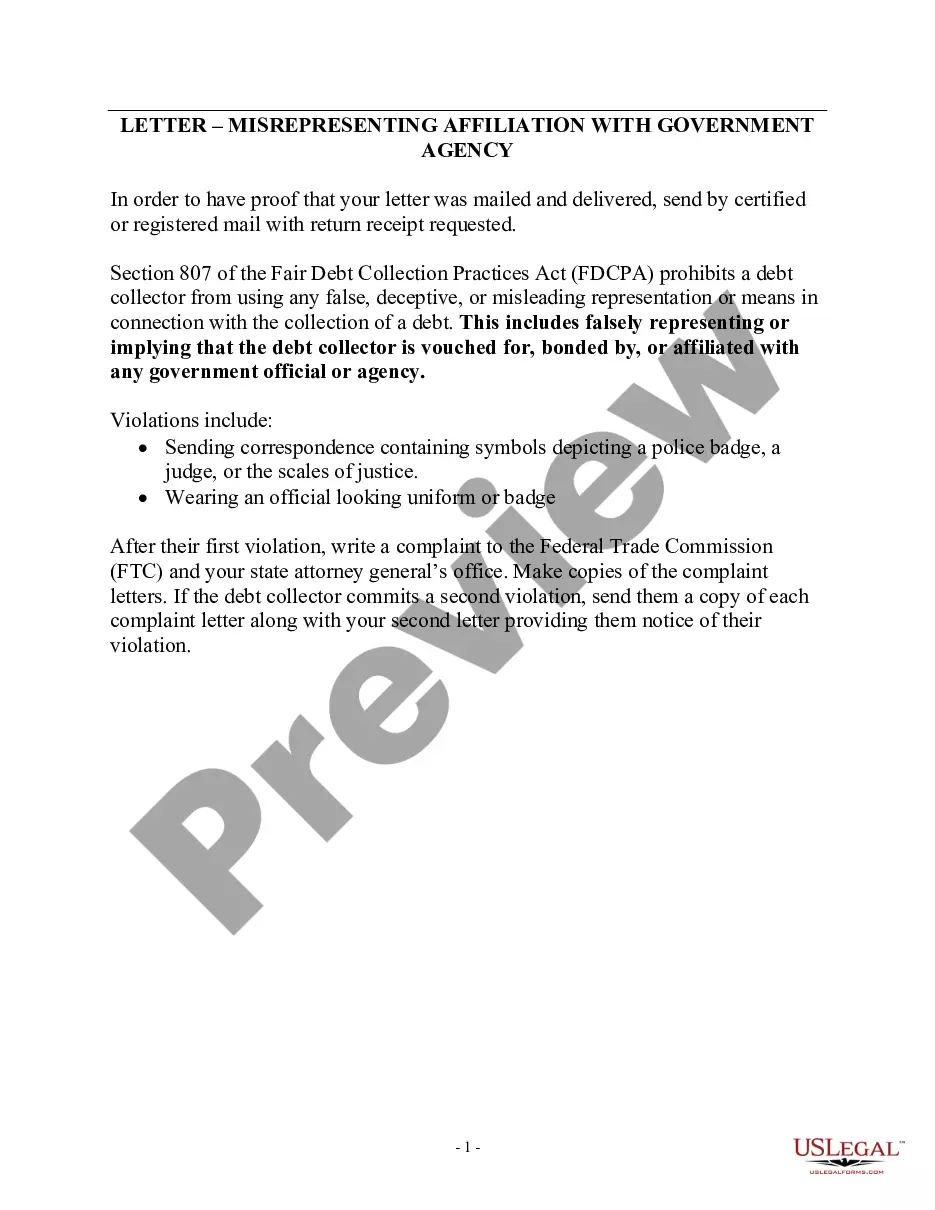

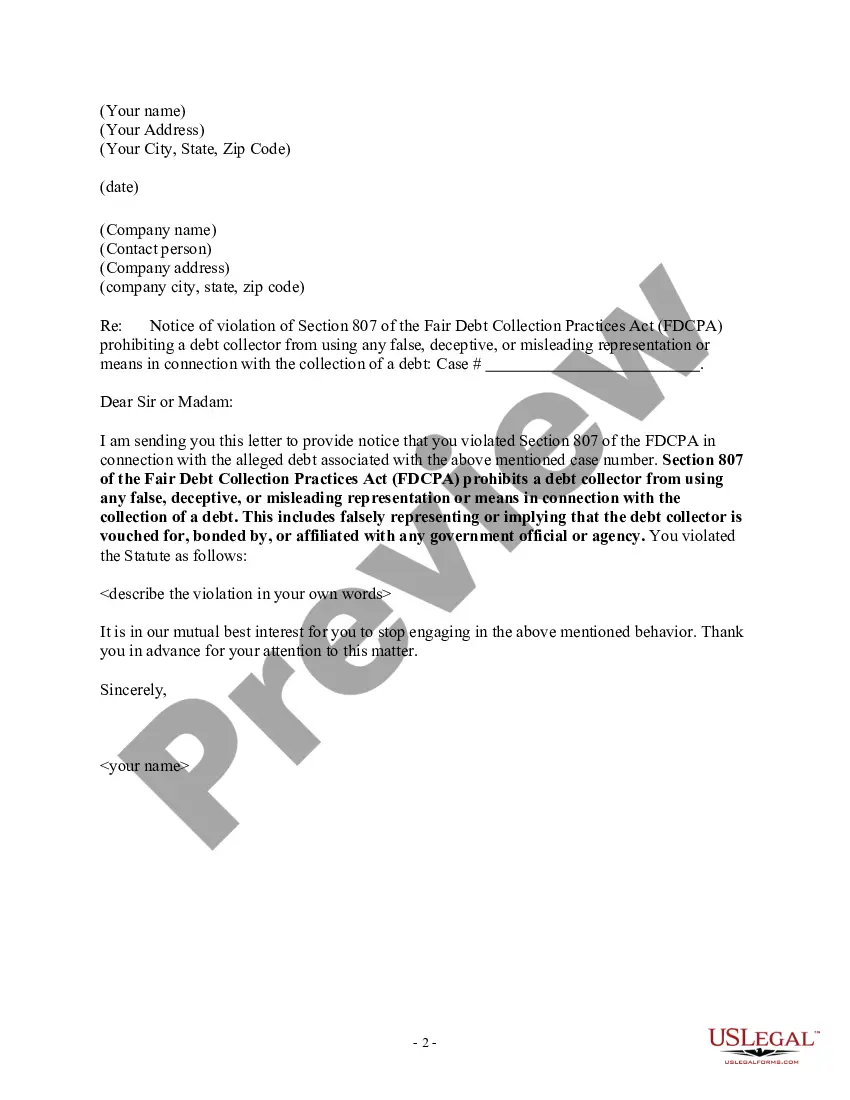

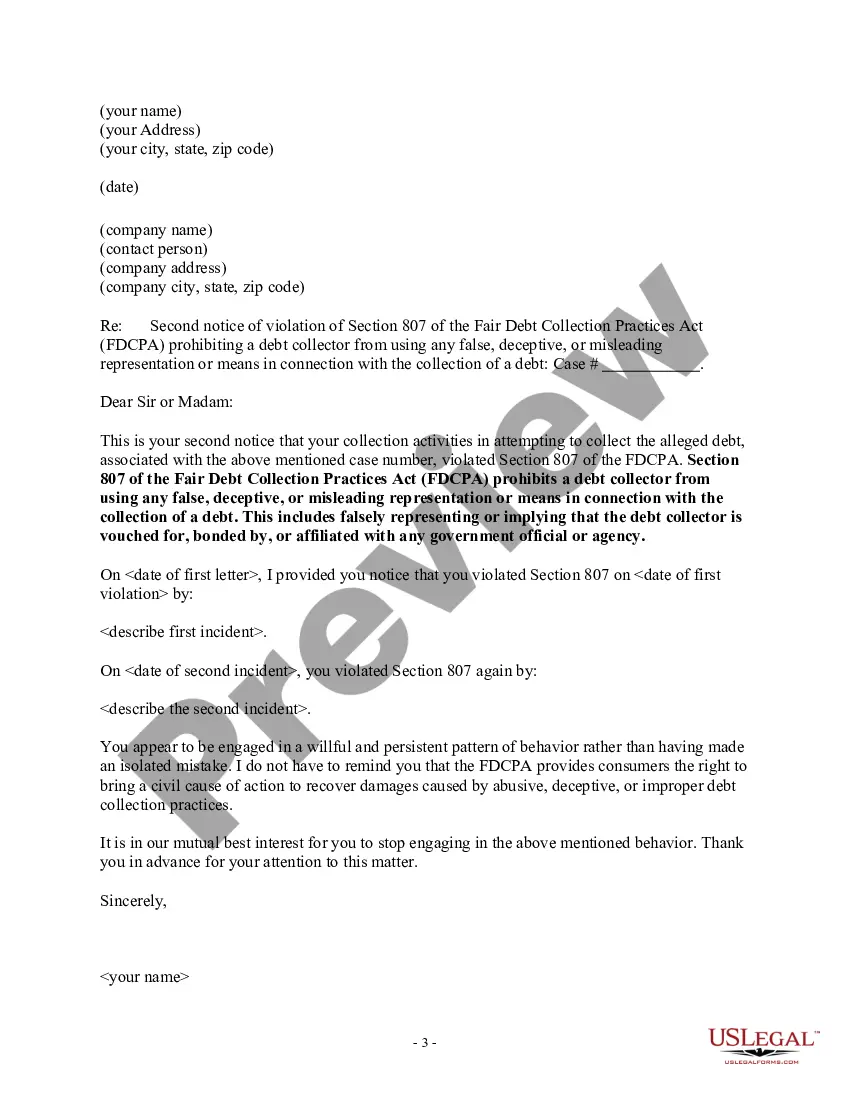

West Virginia Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself

Description

How to fill out West Virginia Notice Of Violation Of Fair Debt Act - Creditor Misrepresented Himself?

Are you in a situation that you need to have paperwork for sometimes enterprise or individual reasons just about every day? There are a variety of authorized file layouts available on the Internet, but finding versions you can depend on is not simple. US Legal Forms provides 1000s of type layouts, like the West Virginia Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself, that happen to be created to fulfill federal and state specifications.

In case you are currently knowledgeable about US Legal Forms site and get an account, basically log in. After that, you can down load the West Virginia Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself template.

Unless you offer an account and would like to start using US Legal Forms, abide by these steps:

- Discover the type you will need and make sure it is for your appropriate area/county.

- Take advantage of the Review key to examine the shape.

- See the information to ensure that you have chosen the correct type.

- When the type is not what you are looking for, make use of the Research area to discover the type that suits you and specifications.

- If you discover the appropriate type, click on Get now.

- Choose the prices plan you would like, fill out the necessary information and facts to generate your account, and buy your order making use of your PayPal or bank card.

- Select a handy paper formatting and down load your version.

Locate all the file layouts you have bought in the My Forms food selection. You may get a extra version of West Virginia Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself whenever, if required. Just click on the needed type to down load or produce the file template.

Use US Legal Forms, by far the most extensive selection of authorized varieties, in order to save some time and prevent faults. The support provides skillfully made authorized file layouts that you can use for a selection of reasons. Make an account on US Legal Forms and commence creating your daily life easier.

Form popularity

FAQ

The FDCPA defines a "creditor" as the person or entity that extended you the credit in the first place (in other words, your original lender). Because the FDCPA is designed to protect debtors against third-party debt collectors, it doesn't apply to your original creditor or its employees.

Unless your state law provides otherwise, the FDCPA only requires debt collectors, not original creditors, to verify debts in certain circumstances. This requirement includes law firms that are routinely engaged in collecting debts.

By definition, creditors and first-party servicers are excluded from coverage because they are not debt collectors under the FDCPA.

The Fair Debt Collection Practices Act (FDCPA) The FDCPA prohibits debt collection companies from using abusive, unfair or deceptive practices to collect debts from you.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.

The FDCPA applies only to the collection of debt incurred by a consumer primarily for personal, family, or household purposes. It does not apply to the collection of corporate debt or debt owed for business or agricultural purposes.

Your credit card debt, auto loans, medical bills, student loans, mortgage, and other household debts are covered under the FDCPA.

At a minimum, proper debt validation should include an account balance along with an explanation of how the amount was derived. But most debt collectors respond with an account statement from the original creditor as debt validation and that's generally considered sufficient.

7 Most Common FDCPA ViolationsContinued attempts to collect debt not owed.Illegal or unethical communication tactics.Disclosure verification of debt.Taking or threatening illegal action.False statements or false representation.Improper contact or sharing of info.Excessive phone calls.

Among the insider tips, Ulzheimer shared with the audience was this: if you are being pursued by debt collectors, you can stop them from calling you ever again by telling them '11-word phrase'. This simple idea was later advertised as an '11-word phrase to stop debt collectors'.