The Wyoming Sale of Deceased Partner's Interest refers to the legal process involved in transferring and selling the ownership share of a deceased partner in a business located in the state of Wyoming, United States. This procedure ensures an orderly transition in the ownership structure and allows the deceased partner's interest to be fairly distributed or liquidated. When a partner dies, their ownership share in a business entity, such as a partnership or limited liability company (LLC), typically needs to be handled according to the terms laid out in the partnership or operating agreement. In Wyoming, the process for selling a deceased partner's interest may vary based on the specific circumstances and the type of business entity involved. There are various types of Wyoming Sale of Deceased Partner's Interest, including: 1. Sale to Remaining Partners: In some cases, the partnership or operating agreement may grant the surviving partners the right to purchase the deceased partner's interest. This option allows the business to maintain its ownership structure and ensures that the remaining partners have control over who becomes a partner. 2. Sale to Existing Shareholders or Members: If the business is structured as a corporation or an LLC with multiple members, the remaining shareholders or members may have the right of first refusal to purchase the deceased partner's interest. This provision safeguards the existing members' interests and prevents the entry of unwanted or unknown individuals into the ownership group. 3. Sale to a Third Party: If the partnership or operating agreement does not specify the rights of the remaining partners or existing members, or if they choose not to exercise their purchase rights, the deceased partner's interest can be sold to a third party. This option allows for the entry of a new partner who can provide additional capital, expertise, or resources to the business. 4. Liquidation and Distribution: If the partners or members decide to dissolve the business entity following the partner's death, the deceased partner's interest can be liquidated and distributed amongst the remaining partners or members. This option involves selling off the deceased partner's share of the business assets, paying off any outstanding debts or obligations, and distributing the remaining proceeds to the surviving partners or members in proportion to their ownership percentages. In all cases, the sale of a deceased partner's interest in Wyoming requires careful consideration of the legal and financial implications. It is crucial to consult with an experienced business attorney who can guide the partners or members through the process and ensure compliance with the relevant laws and regulations governing business entities in Wyoming.

Wyoming Sale of Deceased Partner's Interest

Description

How to fill out Wyoming Sale Of Deceased Partner's Interest?

Selecting the optimum authentic document template can be a challenge.

Naturally, there are numerous templates available online, but how do you find the genuine one you require.

Utilize the US Legal Forms website. The service offers thousands of templates, such as the Wyoming Sale of Deceased Partner's Interest, suitable for both business and personal purposes.

First, ensure you have selected the correct form for your city/area. You can explore the form using the Preview feature and review the form summary to confirm it is the right one for you.

- All of the forms are verified by professionals and comply with federal and state regulations.

- If you are already registered, Log In to your account and click on the Download option to retrieve the Wyoming Sale of Deceased Partner's Interest.

- Use your account to browse the legal forms you have previously purchased.

- Navigate to the My documents section of your account and obtain an additional copy of the document you need.

- If you are a new user of US Legal Forms, here are some simple steps for you to follow.

Form popularity

FAQ

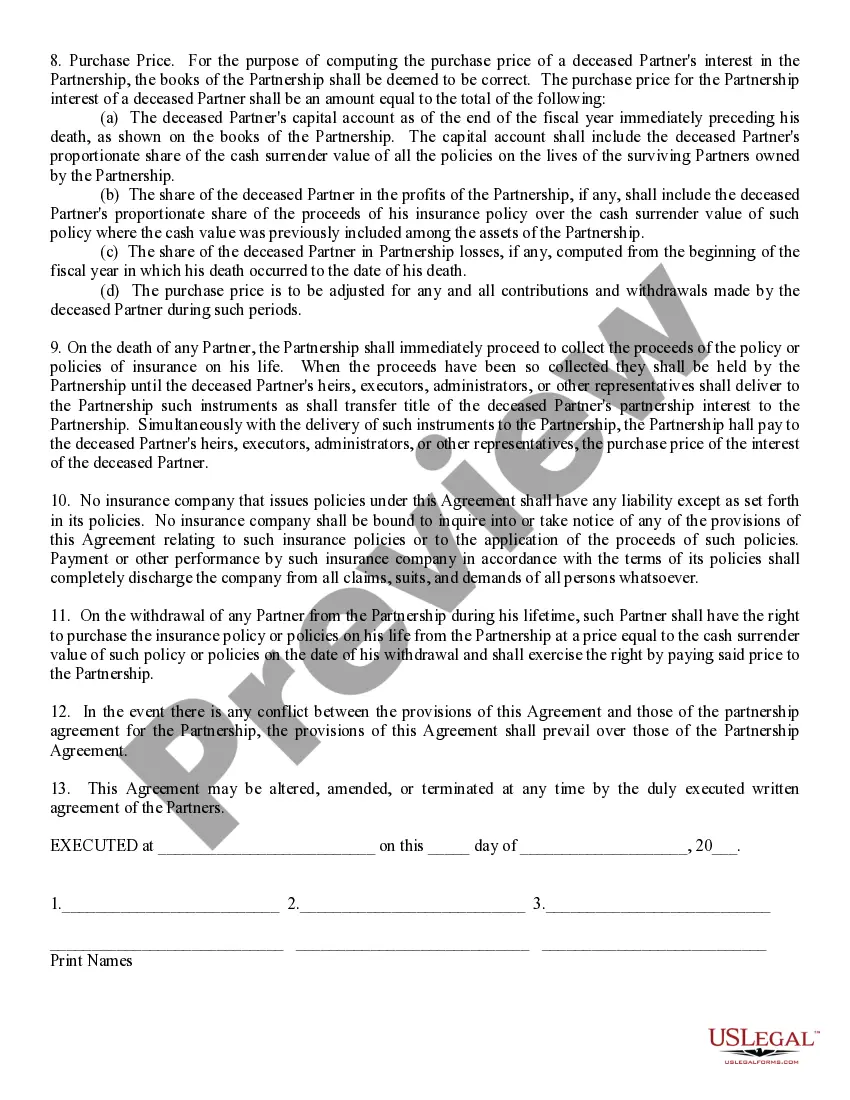

This means that on the death of any partner, all assets liquidated and the proceeds distributed equally between the living partners and the estate of the deceased, regardless of their contribution. Surviving partners do not have any rights to buy the business assets or continue to trade.

Most legislation states that the partnership will end upon the death or bankruptcy of any partner. If your partner dies, you will then owe your partner's estate their share of the partnership that accrues at the date of their death.

It should be noted that under section 37 of the Partnership Act, the executors would be entitled, at their choice, to interest at 6% p.a. on the amount due from the date of death to the date of payment or to that portion of profit which is earned by the firm with the help of the amount due to the deceased partner.

The death of a partner in a two-person partnership will terminate the partnership for federal tax purposes if it results in the partnership's immediately winding up its business (Sec. 708(b)(1)(A)). If this occurs, the partnership's tax year closes on the partner's date of death.

The death of a partner in a two-person partnership will terminate the partnership for federal tax purposes if it results in the partnership's immediately winding up its business (Sec. 708(b)(1)(A)). If this occurs, the partnership's tax year closes on the partner's date of death.

The gain or loss from the sale of a partnership interest is the difference between the sales proceeds received and the partner's tax basis in the interest at the time of the sale.

This means that a partner wishing to leave the partnership must first offer their interest to the other members in the company before offering it to an outside party. If all of the members refuse this offer, the partner is then allowed to transfer interest to anyone they choose.

The decedent's estate (or other successor, such as a living/revocable trust, depending upon how the deceased partner held their partnership interest; the Estate), will take such interest with an adjusted basis equal to the fair market value of such interest at the date of the partner's death, increased by the

Business partnership agreement. A properly arranged and funded agreement is a legally binding contract that spells out exactly what is to happen if one of the business's owners dies. It generally calls for the survivors to buy the deceased owner's share in the business from his or her heirs.

Can You Inherit A Partnership Interest? The partner can acquire his interest from his existing partner, for example. Gift or inheritance may be used to acquire a partnership interest. In addition, a partnership could get a special interest in property and cash from a partner.

Interesting Questions

More info

Interconnect Wolters Kluwer Interconnect History Help Login Log-in Log-in Log-in Log-in Login.