Gift taxes are taxes that supplement the Estate Tax. Gift taxes are placed on gifts given away to any person while you are still living, so that you may not avoid estate taxes by making gifts of your estate. You may give up to $12,000 a year in cash or assets to an unlimited number of people each year without incurring gift tax liability, but the gifts must have no conditions attached. Married couples can give, as a couple, a $24,000 gift per year to as many people as they want. Under federal tax law, gifts totaling more than $12,000 to one person in one year are considered a taxable gift and generate a potential gift tax. It does not matter if you give one $13,000 gift or 13 gifts of $1,000 each, or one gift of $12,000 and a "birthday gift" of $1,000.

Gifts beyond the $12,000 limit (there is an exception for gifts that are directly paid by the gift giver for tuition and medical expenses) are considered "taxable gifts." Taxable gifts create liability for a gift tax. But gift tax is not due to be paid until you give away over $1,000,000 in your lifetime.

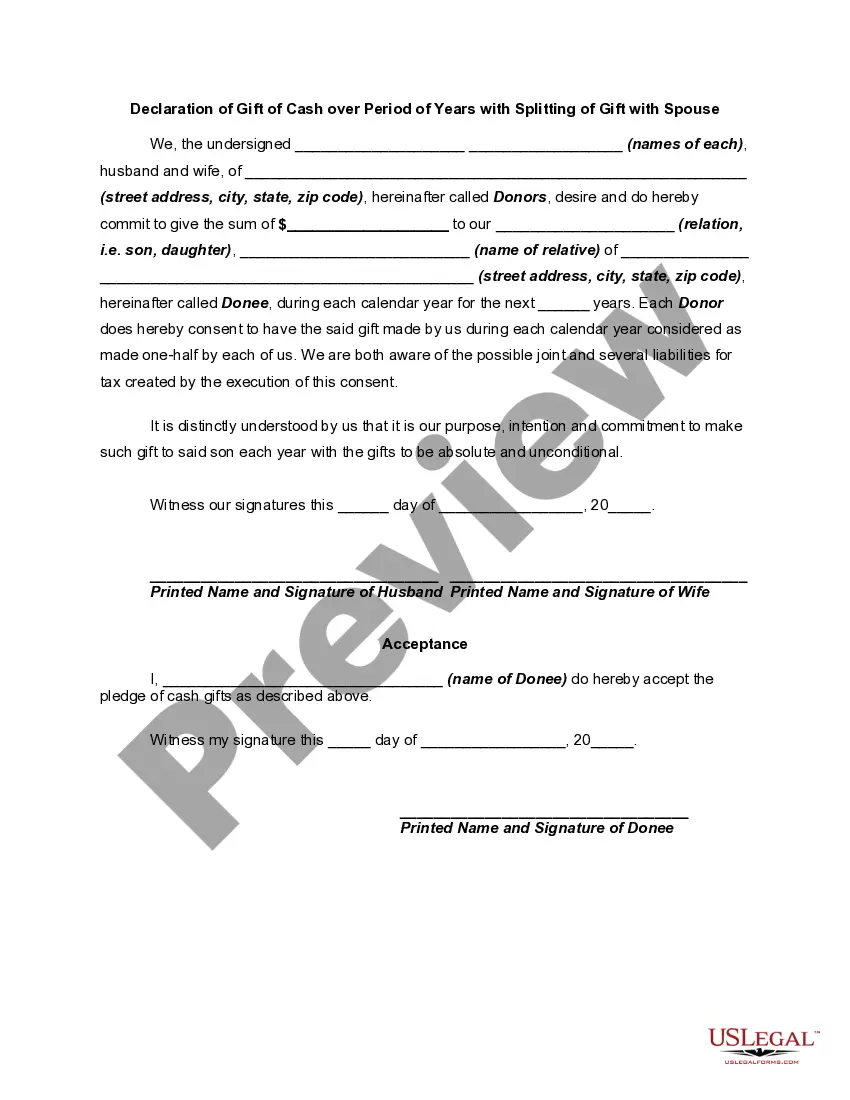

The Wyoming Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a legal document used to outline the details of a donation of cash that will be made over a specified number of years, while also allowing the option to split the gift amount with a spouse. This declaration is specific to the state of Wyoming and ensures compliance with state laws and regulations regarding gift giving. This type of declaration is commonly used in estate planning and philanthropic endeavors, where an individual or couple wishes to make a significant donation to a charitable organization or foundation but prefers to distribute the gift amount over multiple years. By spreading out the donation, the donor can take advantage of tax benefits and minimize the impact on their financial situation in a single year. The Wyoming Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse provides clarity and legal protection for all parties involved. It includes the following key information: 1. Donor Information: The declaration starts by identifying the donor or donors involved in the gift. 2. Spouse's Consent: In instances where the gift is to be split with a spouse, the declaration includes a section where the spouse gives their consent and agrees to distribute the gift as outlined. 3. Charitable Organization Information: The declaration specifies the name and contact details of the charitable organization or foundation that will receive the gift. 4. Gift Amount: The document stipulates the total amount of the gift and the portion that will be donated each year. 5. Duration of the Gift: The declaration outlines the number of years over which the gift will be given. 6. Method of Distribution: This section details the preferred method of distributing the gift each year, whether it be in equal installments or varying amounts. 7. Tax Implications: The declaration acknowledges any tax implications and states whether the donor or the charitable organization will be responsible for any associated taxes. Different variations or types of the Wyoming Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse may include specific provisions tailored to individual circumstances. For example, there could be options to adjust gift amounts during the specified period, add contingencies in case of unforeseen circumstances, or include restrictions on how the charitable organization may utilize the funds. In conclusion, the Wyoming Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a valuable legal document for individuals or couples in Wyoming who wish to make a donation spread over several years while also involving their spouse in the giving process. It ensures compliance with state laws, provides clarity for all parties involved, and helps individuals fulfill their philanthropic goals while optimizing tax benefits.