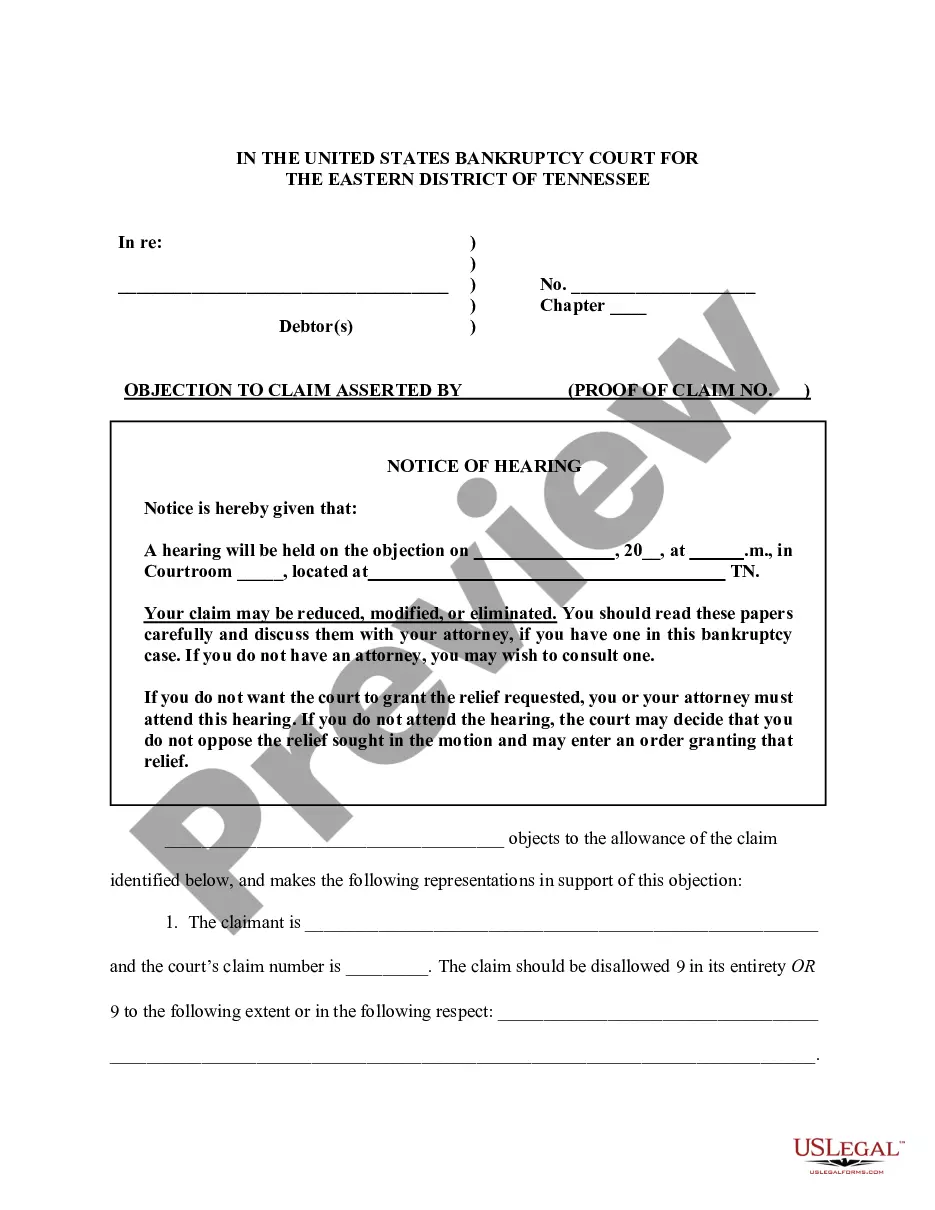

Any interested party in an estate of a decedent generally has the right to make objections to the accounting of the executor, the compensation paid or

proposed to be paid, or the proposed distribution of assets. Such objections must be filed within within a certain period of time from the date of service of the Petition for approval of the accounting.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Wyoming Objection to Allowed Claim in Accounting is a legal process through which a party disputes the validity or accuracy of a claim made in an accounting statement or report in the state of Wyoming. This objection is typically raised by an individual or a company that believes there are errors, discrepancies, or inconsistencies in the financial records provided. Key terms and keywords related to Wyoming Objection to Allowed Claim in Accounting: 1. Wyoming: The state where this objection process takes place, specifically concerning accounting claims. 2. Objection: A formal protest or challenge made by a party disputing the accuracy or validity of a claim. 3. Allowed Claim: A claim that has been approved or accepted by the accounting department or a court. 4. Accounting: The systematic process of recording, summarizing, analyzing, and interpreting financial information. 5. Discrepancies: Differences or inconsistencies found in financial records that may require further examination or clarification. 6. Errors: Mistakes or inaccuracies in financial statements, records, or calculations. 7. Inconsistencies: Contradictions or variations in data, calculations, or statements that need to be resolved. 8. Financial Records: Official documents containing information about an entity's financial transactions, such as balance sheets, income statements, and cash flow statements. Types of Wyoming Objection to Allowed Claim in Accounting: 1. Inaccurate Reporting: A party objects to an allowed claim by pointing out errors or misinterpretations in the financial reports provided by the claiming party. 2. Misclassification of Expenses: The objecting party challenges the classification of certain expenses within the claim, arguing that they were incorrectly categorized and should be reevaluated. 3. Calculation Errors: An objection is raised when mathematical mistakes are identified in the calculations provided within the accounting claim. 4. Documentation Discrepancies: The objecting party argues that the supporting documents provided with the claim do not align with the financial records or transactions stated, casting doubt on the claim's accuracy. 5. Lack of Supporting Evidence: An objection is made when the claiming party fails to provide sufficient evidence or documentation that can substantiate the validity of their claim. 6. Fraud or Misrepresentation: The objecting party asserts that the allowed claim is a result of intentional deception, misrepresentation, or fraudulent activities committed by the opposing party. It is important to consult legal and accounting professionals to fully understand the specifics and requirements of Wyoming Objection to Allowed Claim in Accounting.