Wyoming Breakdown of Savings for Budget and Emergency Fund

Description

How to fill out Breakdown Of Savings For Budget And Emergency Fund?

Locating the appropriate valid document template can be challenging.

Of course, there are numerous templates available online, but how do you find the legitimate form you need.

Utilize the US Legal Forms platform. This service offers an extensive collection of templates, including the Wyoming Breakdown of Savings for Budget and Emergency Fund, suitable for both business and personal purposes.

You can review the document using the Review button and read the form description to confirm it’s suitable for you.

- All templates are verified by experts and comply with federal and state regulations.

- If you already have an account, Log In to your profile and click the Obtain button to download the Wyoming Breakdown of Savings for Budget and Emergency Fund.

- Use your account to browse through the legal forms you have previously purchased.

- Visit the My documents tab in your account to retrieve another copy of the document you need.

- For new users of US Legal Forms, here are simple steps to follow.

- First, make sure you have selected the correct form for your location.

Form popularity

FAQ

It does work. That $1,000 emergency fund will be enough to have your back while you hustle to pay off your debt as quick as you can. The Baby Steps work, so stick with themno matter how uncomfortable it might make you feel. Lean into that awkward feeling and let that spur you on to pay off your debt even faster.

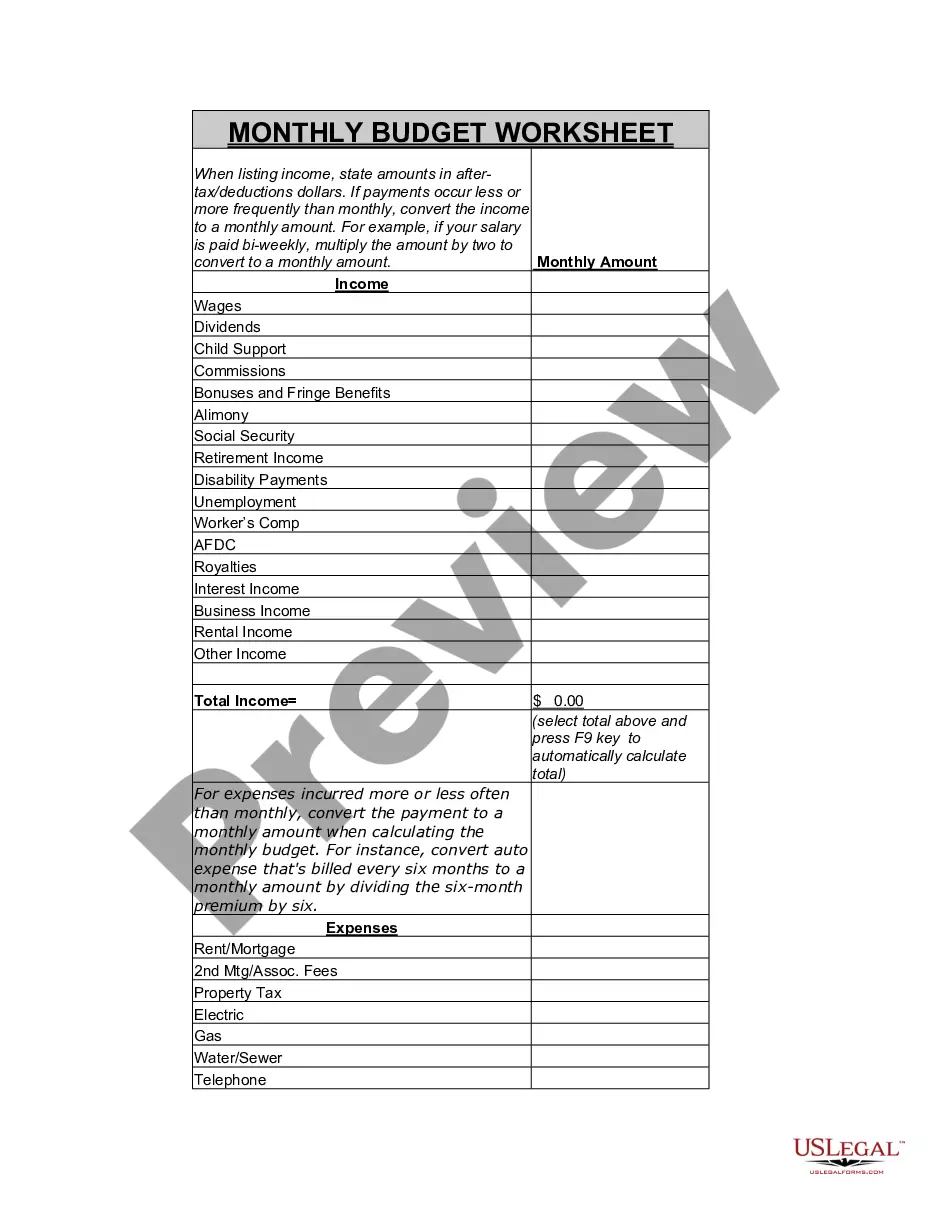

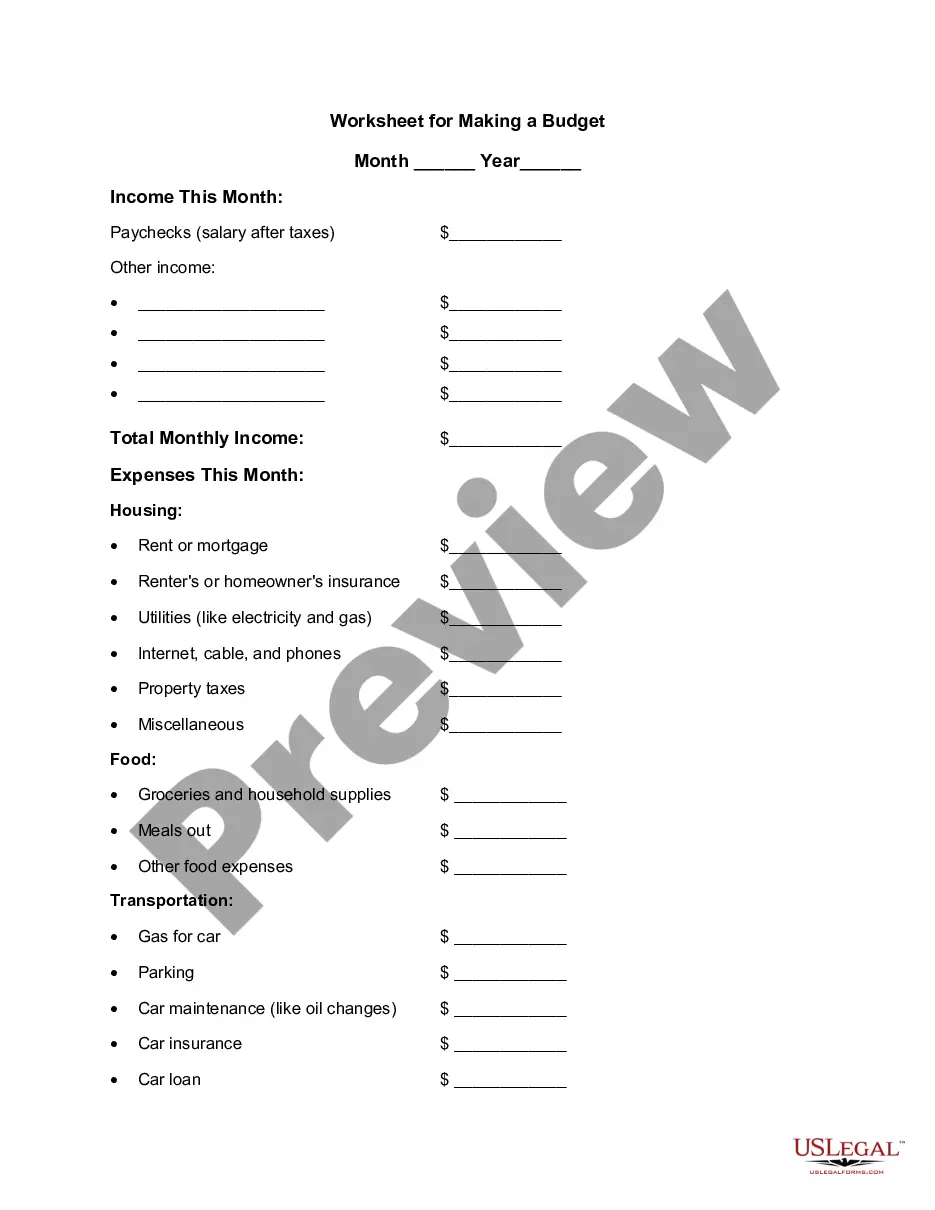

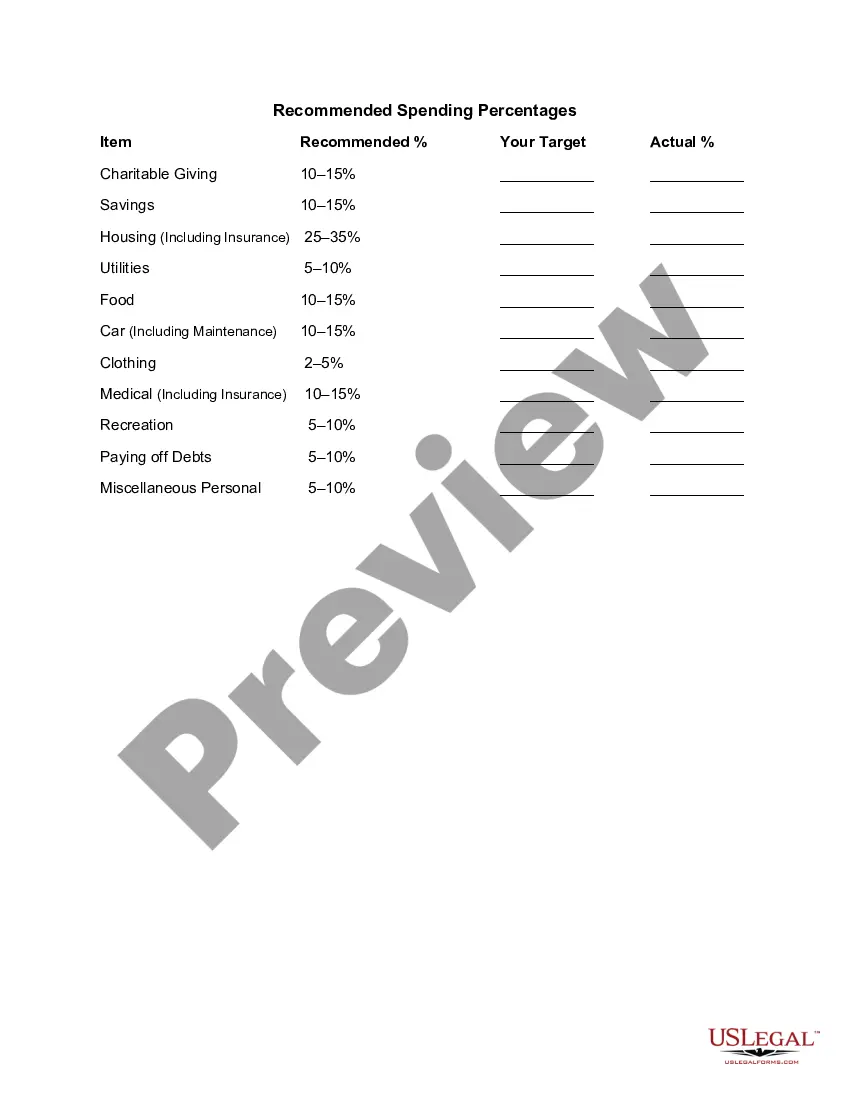

While the size of your emergency fund will vary depending on your lifestyle, monthly costs, income, and dependents, the rule of thumb is to put away at least three to six months' worth of expenses.

Calculate a Target Amount I generally recommend three months of net pay set aside for emergencies, she said. If you get two paychecks a month, and they are each $3,000 that's $6,000. I would multiply that by three, so you're looking at about nearly $20,000 in emergency savings.

I generally recommend three months of net pay set aside for emergencies, she said. If you get two paychecks a month, and they are each $3,000 that's $6,000. I would multiply that by three, so you're looking at about nearly $20,000 in emergency savings.

Most financial experts recommend that you have somewhere between three months and six months of basic living expenses in your emergency fund. The three-month guideline is generally recommended for those who are in salaried positions and have more secure employment.

What is the 50/30/20 rule? The 50/30/20 rule is an easy budgeting method that can help you to manage your money effectively, simply and sustainably. The basic rule of thumb is to divide your monthly after-tax income into three spending categories: 50% for needs, 30% for wants and 20% for savings or paying off debt.

The short answer: If starting small, try to set aside at least $500, but work your way up to half a year's worth of expenses. The long answer: The right amount for you depends on your financial circumstances, but a good rule of thumb is to have enough to cover three to six months' worth of living expenses.

The median emergency fund balance among workers today is $5,000, according to the 21st Annual Transamerica Retirement Survey. Not surprisingly, emergency savings increase by age, with median balances coming in at: $2,000 for Gen Z workers. $5,000 for millennial workers.

Poorman suggests the popular 50/30/20 rule of thumb for paycheck allocation: 50% of gross pay for essentials like bills and regular expenses (groceries, rent, or mortgage) 30% for spending on dining/ordering out and entertainment. 20% for personal saving and investment goals.

How much money should you have left after paying bills? This will vary from person to person but a good rule of thumb is to follow the 50/20/30 formula. 50% of your money to expenses, 30% into debt payoff, and 20% into savings.