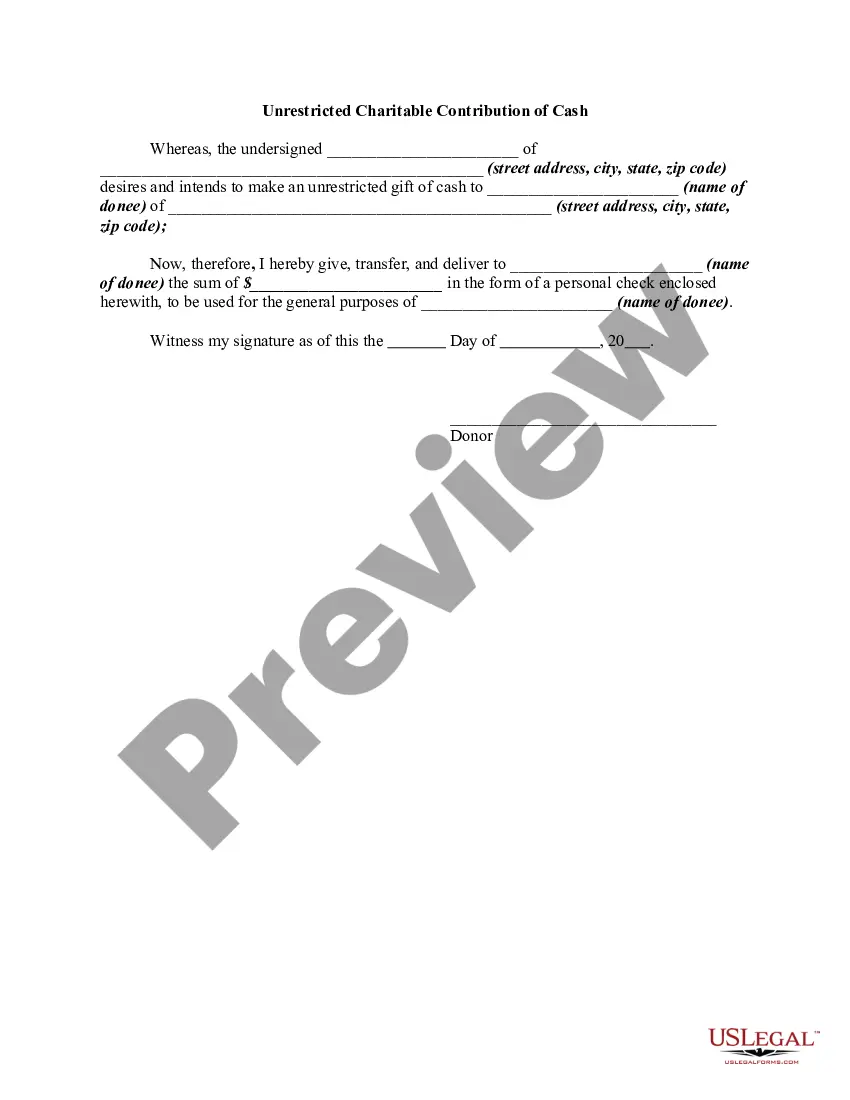

Wyoming Unrestricted Charitable Contribution of Cash

Description

How to fill out Unrestricted Charitable Contribution Of Cash?

Have you ever been in a situation where you require documentation that a certain organization or individual utilizes almost every time.

There are many legal document templates accessible online, but finding reliable versions can be challenging.

US Legal Forms offers thousands of document templates, including the Wyoming Unrestricted Charitable Contribution of Cash, that are crafted to comply with state and federal regulations.

Once you locate the appropriate document, click Buy now.

Select your preferred pricing plan, enter the necessary information to create your account, and complete your purchase using PayPal or a Visa or Mastercard.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Then, you can download the Wyoming Unrestricted Charitable Contribution of Cash template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Locate the form you need and ensure it corresponds to your area/state.

- Use the Review button to examine the form.

- Read the description to verify that you have chosen the correct document.

- If the document is not what you are looking for, utilize the Lookup field to find the form that fits your needs and requirements.

Form popularity

FAQ

Proof can be provided in the form of an official receipt or invoice from the receiving charitable organization, but can also be provided via credit card statements or other financial records detailing the donation.

Any donations worth $250 or more must be recognized with a receipt. The charity receiving this donation must automatically provide the donor with a receipt. As a general rule a nonprofit organization should NOT place a value on what is donated (that is the responsibility of the donor).

Any donations worth $250 or more must be recognized with a receipt. The charity receiving this donation must automatically provide the donor with a receipt. As a general rule a nonprofit organization should NOT place a value on what is donated (that is the responsibility of the donor).

Cash or property donations worth more than $250: The IRS requires you to get a written letter of acknowledgment from the charity. It must include the amount of cash you donated, whether you received anything from the charity in exchange for your donation, and an estimate of the value of those goods and services.

Most taxpayers can deduct up to $300 in charitable contributions without itemizing deductions Internal Revenue Service.

In most cases, the amount of charitable cash contributions taxpayers can deduct on Schedule A as an itemized deduction is limited to a percentage (usually 60 percent) of the taxpayer's adjusted gross income (AGI). Qualified contributions are not subject to this limitation.

Most taxpayers can deduct up to $300 in charitable contributions without itemizing deductions.

Proof can be provided in the form of an official receipt or invoice from the receiving charitable organization, but can also be provided via credit card statements or other financial records detailing the donation.

Cash or property donations worth more than $250: The IRS requires you to get a written letter of acknowledgment from the charity. It must include the amount of cash you donated, whether you received anything from the charity in exchange for your donation, and an estimate of the value of those goods and services.

For any contribution of $250 or more (including contributions of cash or property), you must obtain and keep in your records a contemporaneous written acknowledgment from the qualified organization indicating the amount of the cash and a description of any property contributed.