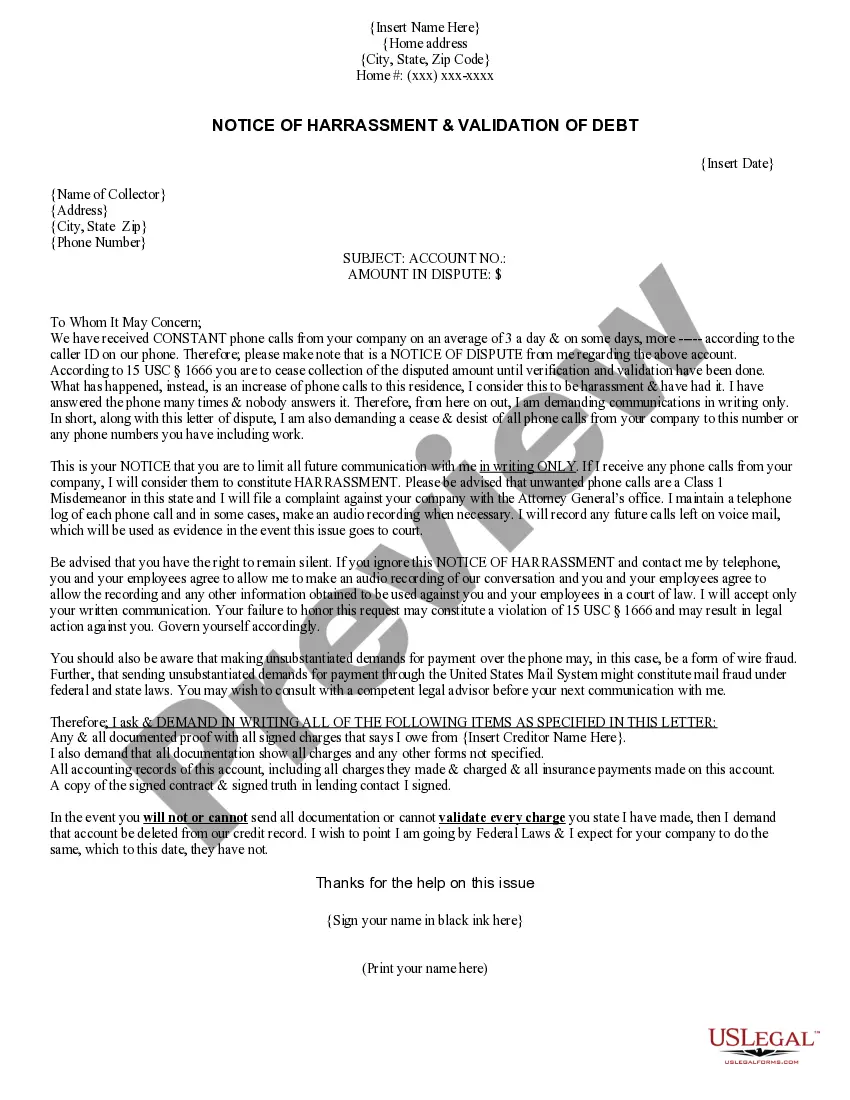

This NOTICE OF HARRASSMENT & VALIDATION OF DEBT is to be used when creditors call you repeatedly and mail you letters too. This form includes a cease and desist and a validation of debt, 2 letters in one.

Wyoming Notice of Harassment and Validation of Debt

Instant download

Description

How to fill out Wyoming Notice Of Harassment And Validation Of Debt?

If you wish to comprehensive, down load, or print out legal record themes, use US Legal Forms, the largest variety of legal kinds, that can be found on-line. Use the site`s easy and hassle-free lookup to obtain the files you want. Numerous themes for business and personal uses are sorted by classes and says, or key phrases. Use US Legal Forms to obtain the Wyoming Notice of Harassment and Validation of Debt in a few mouse clicks.

In case you are already a US Legal Forms buyer, log in to your account and then click the Acquire button to obtain the Wyoming Notice of Harassment and Validation of Debt. Also you can gain access to kinds you formerly downloaded from the My Forms tab of the account.

If you are using US Legal Forms the first time, follow the instructions below:

- Step 1. Ensure you have chosen the shape for that appropriate metropolis/nation.

- Step 2. Utilize the Preview method to examine the form`s content material. Do not forget to see the explanation.

- Step 3. In case you are unsatisfied using the type, use the Lookup industry near the top of the monitor to locate other versions in the legal type design.

- Step 4. Once you have located the shape you want, click the Buy now button. Pick the costs strategy you prefer and add your credentials to sign up for the account.

- Step 5. Process the purchase. You should use your credit card or PayPal account to accomplish the purchase.

- Step 6. Find the format in the legal type and down load it on your gadget.

- Step 7. Comprehensive, change and print out or indicator the Wyoming Notice of Harassment and Validation of Debt.

Every single legal record design you acquire is yours for a long time. You might have acces to every single type you downloaded within your acccount. Click the My Forms area and pick a type to print out or down load once more.

Be competitive and down load, and print out the Wyoming Notice of Harassment and Validation of Debt with US Legal Forms. There are many professional and status-specific kinds you can use for your personal business or personal demands.

Form popularity

FAQ

Fortunately, there are legal actions you can take to stop this harassment:Write a Letter Requesting To Cease Communications.Document All Contact and Harassment.File a Complaint With the FTC.File a Complaint With Your State's Agency.Consider Suing the Debt Collection Agency for Harassment.

The definition of debt collection harassment is to intimidate, abuse, coerce, bully or browbeat consumers into paying off debt. This happens most often over the phone, but harassment could come in the form of emails, texts, direct mail or talking to friends or neighbors about your debt.

No harassment The Fair Debt Collection Practices Act (FDCPA) says debt collectors can't harass, oppress, or abuse you or anyone else they contact. Some examples of harassment are: Repetitious phone calls that are intended to annoy, abuse, or harass you or any person answering the phone. Obscene or profane language.

Debt collectors are legally required to send one within five days of first contact. You have within 30 days from receiving a debt validation letter to send a debt verification letter. Here's the important part: You have just 30 days to respond to a debt validation letter with your debt verification letter.

Debt Collectors Can't Call You Repeatedly to Harass You This means that while the FDCPA doesn't place a specific limit on the number of calls debt collectors can make, it prohibits them from calling you multiple times just to harass you. (15 U.S. Code §? 1692d).

Failing to respond to a Debt Validation Letter while continuing to collect on the debt is a direct violation of the FDCPA. You can report a debt collector's failure to respond to your state's attorney general, the Consumer Financial Protection Bureau (CFPB), or the FTC.

The definition of debt collection harassment is to intimidate, abuse, coerce, bully or browbeat consumers into paying off debt. This happens most often over the phone, but harassment could come in the form of emails, texts, direct mail or talking to friends or neighbors about your debt.

If a debt collector fails to verify the debt but continues to go after you for payment, you have the right to sue that debt collector in federal or state court. You might be able to get $1,000 per lawsuit, plus actual damages, attorneys' fees, and court costs.

If you get a summons notifying you that a debt collector is suing you, don't ignore it. If you do, the collector may be able to get a default judgment against you (that is, the court enters judgment in the collector's favor because you didn't respond to defend yourself) and garnish your wages and bank account.

A debt validation letter should include the name of your creditor, how much you supposedly owe, and information on how to dispute the debt. After receiving a debt validation letter, you have 30 days to dispute the debt and request written evidence of it from the debt collector.

More info

§ 1692g, which mandates that a debt collector obtain verification of an alleged debt, if put on notice by the alleged debtor or his agent, that the debt is in ... Remember that if you make a written request for a debt verification notice, the collector is legally required to cease all debt collection ...The federal Fair Debt Collection Practices Act (FDCPA) was enacted to curba debt collector must send you a written notice stating how much you owe, ... The FDCPA protects consumers from harassment and deceitful tactics, outlines unfair practices, and establishes an avenue for individuals to file ... Has NCO Financial Systems violated your rights under the FDCPA? Are they harassing your for debt you do not owe? Get your free case review now! Plaintiff (e.g., creditor or debt buyer) files a complaint in court and provides notice of the lawsuit to defendant (i.e., person being sued). Once or twice a year she gets a letter from a collection agency.Federal law already prohibits debt collectors from harassing consumers ... So before you do anything else, send the collector a debt validation letter. This letter is allowed by the Fair Debt Collection Practices ... Thanks for the great tips and pointers! Now can you deliver some debt validation letter templates? If you're being harassed by a debt collector, we may be able to help.Collectors are required to send you a "validation notice" within ...