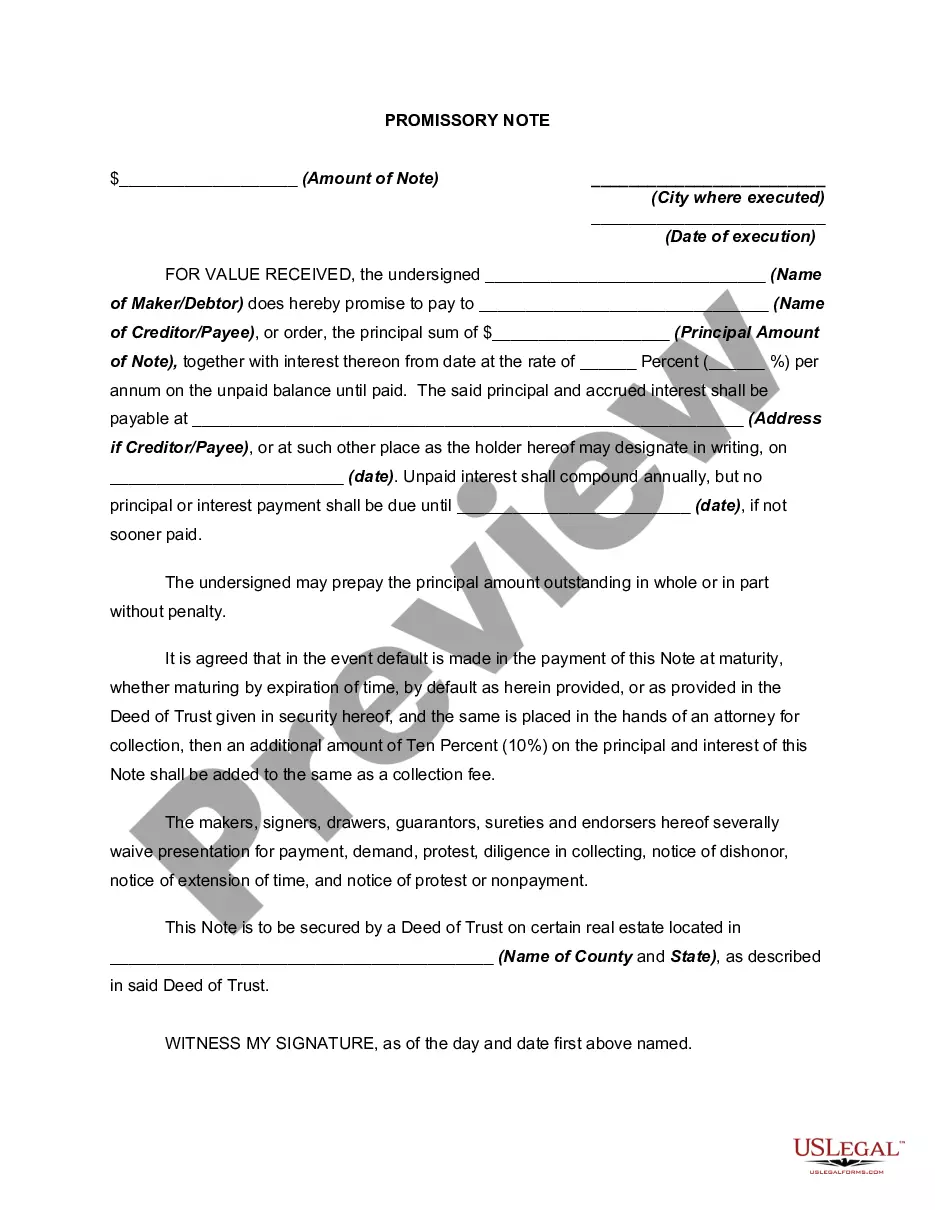

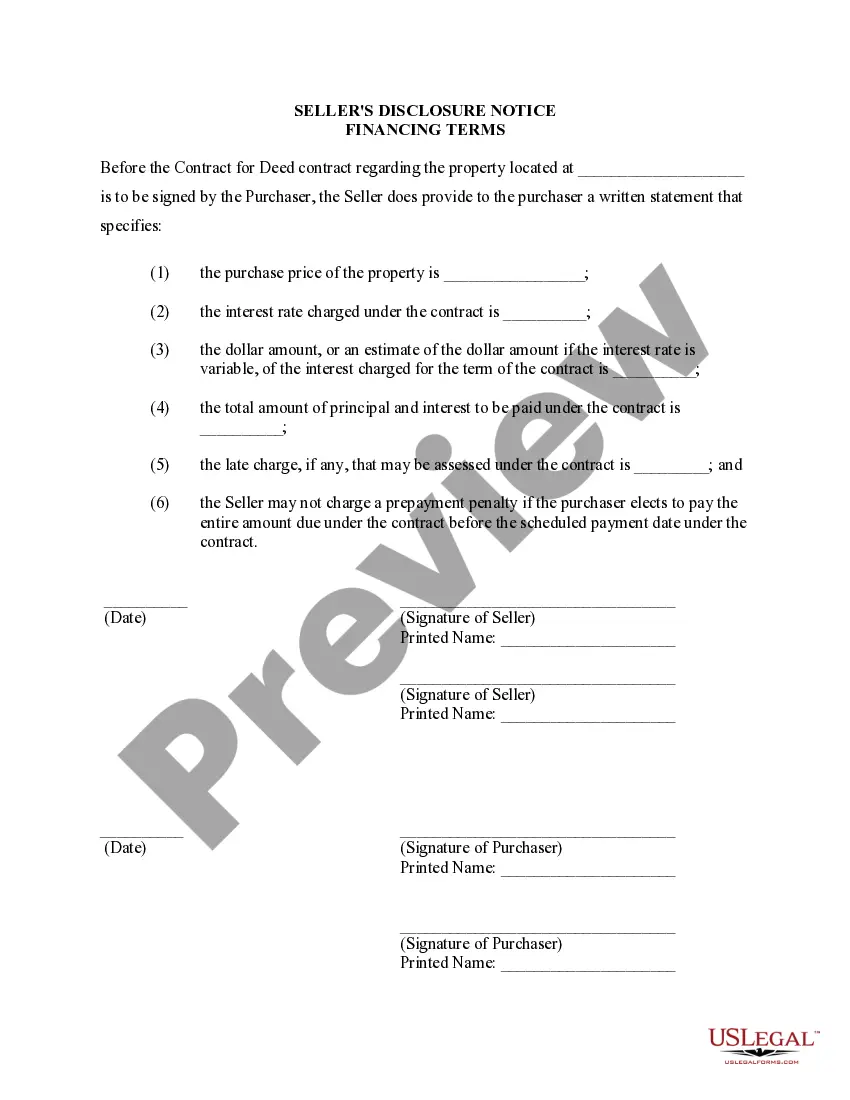

This Seller's Disclosure Notice of Financing Terms Contract for Deed serves as notice to Purchaser of the purchase price of property and how payments, interest, and late charges are set. This document should be completed by Seller of property and provided to the Purchaser at or before the signing of the contract for deed.

Santa Ana, California Seller's Disclosure of Financing Terms for Residential Property in Connection with Contract or Agreement for Deed — A Comprehensive Guide When entering into a real estate transaction involving residential property in Santa Ana, California, it is imperative for both buyers and sellers to have a clear understanding of the financing terms. In particular, when a contract or agreement for deed, also known as a land contract, is involved, the seller is obligated to provide a detailed disclosure of the financing terms. This helps ensure transparency and protects the interests of all parties involved in the transaction. The Seller's Disclosure of Financing Terms for Residential Property in connection with a Contract or Agreement for Deed serves as a document outlining the various financial aspects of the transaction, covering important details such as loan conditions, interest rates, payment terms, and any additional charges or fees that the buyer may encounter. In Santa Ana, California, there are several types of Seller's Disclosures of Financing Terms for Residential Property in connection with a Contract or Agreement for Deed, based on the specific circumstances of the transaction. Some of these variations include: 1. Traditional Financing Terms Disclosure: This type of disclosure is used when the buyer and seller agree to follow the conventional route of obtaining financing from a financial institution or lender. It outlines the terms of the loan, including the principal amount, interest rate, repayment schedule, and any prepayment penalties. 2. Seller Financing Terms Disclosure: In cases where the seller chooses to finance the purchase directly, without involving a third-party lender, this disclosure is required. It details the seller's financing terms, such as the down payment amount, interest rate, repayment schedule, and other relevant conditions. 3. Balloon Payment Disclosure: A balloon payment refers to a lump sum payment due at the end of the loan term. If such a payment structure is part of the financing terms in a contract or agreement for deed, the seller must include a specific disclosure outlining the presence of a balloon payment, its amount, and when it becomes due. 4. Variable Interest Rate Disclosure: If the financing terms for the residential property involve a variable or adjustable interest rate, the seller is obligated to provide a disclosure notifying the buyer of this condition. This disclosure should detail how the interest rate is determined, the frequency of adjustments, and any caps or limits on rate changes. 5. Additional Charges and Fees Disclosure: Apart from the principal loan amount and interest, certain additional charges or fees may be applicable, such as late payment fees, processing fees, or document recording fees. The seller must disclose all such charges in this disclosure, ensuring that the buyer is fully informed about the financial obligations associated with the transaction. In conclusion, the Seller's Disclosure of Financing Terms for Residential Property in connection with a Contract or Agreement for Deed in Santa Ana, California, is a crucial document that outlines the financial aspects of the transaction. From traditional financing terms to seller financing, balloon payments, variable interest rates, and additional charges, these disclosures ensure transparency and protect the rights of buyers and sellers in the residential property market.Santa Ana, California Seller's Disclosure of Financing Terms for Residential Property in Connection with Contract or Agreement for Deed — A Comprehensive Guide When entering into a real estate transaction involving residential property in Santa Ana, California, it is imperative for both buyers and sellers to have a clear understanding of the financing terms. In particular, when a contract or agreement for deed, also known as a land contract, is involved, the seller is obligated to provide a detailed disclosure of the financing terms. This helps ensure transparency and protects the interests of all parties involved in the transaction. The Seller's Disclosure of Financing Terms for Residential Property in connection with a Contract or Agreement for Deed serves as a document outlining the various financial aspects of the transaction, covering important details such as loan conditions, interest rates, payment terms, and any additional charges or fees that the buyer may encounter. In Santa Ana, California, there are several types of Seller's Disclosures of Financing Terms for Residential Property in connection with a Contract or Agreement for Deed, based on the specific circumstances of the transaction. Some of these variations include: 1. Traditional Financing Terms Disclosure: This type of disclosure is used when the buyer and seller agree to follow the conventional route of obtaining financing from a financial institution or lender. It outlines the terms of the loan, including the principal amount, interest rate, repayment schedule, and any prepayment penalties. 2. Seller Financing Terms Disclosure: In cases where the seller chooses to finance the purchase directly, without involving a third-party lender, this disclosure is required. It details the seller's financing terms, such as the down payment amount, interest rate, repayment schedule, and other relevant conditions. 3. Balloon Payment Disclosure: A balloon payment refers to a lump sum payment due at the end of the loan term. If such a payment structure is part of the financing terms in a contract or agreement for deed, the seller must include a specific disclosure outlining the presence of a balloon payment, its amount, and when it becomes due. 4. Variable Interest Rate Disclosure: If the financing terms for the residential property involve a variable or adjustable interest rate, the seller is obligated to provide a disclosure notifying the buyer of this condition. This disclosure should detail how the interest rate is determined, the frequency of adjustments, and any caps or limits on rate changes. 5. Additional Charges and Fees Disclosure: Apart from the principal loan amount and interest, certain additional charges or fees may be applicable, such as late payment fees, processing fees, or document recording fees. The seller must disclose all such charges in this disclosure, ensuring that the buyer is fully informed about the financial obligations associated with the transaction. In conclusion, the Seller's Disclosure of Financing Terms for Residential Property in connection with a Contract or Agreement for Deed in Santa Ana, California, is a crucial document that outlines the financial aspects of the transaction. From traditional financing terms to seller financing, balloon payments, variable interest rates, and additional charges, these disclosures ensure transparency and protect the rights of buyers and sellers in the residential property market.