This form is a generic example that may be referred to when preparing such a form.

San Jose California Deed of Trust Securing Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually

Category:

State:

California

City:

San Jose

Control #:

CA-01701BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out California Deed Of Trust Securing Promissory Note With No Payment Due Until Maturity And Interest To Compound Annually?

Regardless of social or occupational position, completing legal documents is a regrettable requirement in the modern professional landscape.

It is frequently exceedingly difficult for individuals lacking any legal education to create these types of documents from scratch, primarily due to the intricate terminology and legal subtleties they involve.

This is where US Legal Forms proves to be invaluable.

Verify that the template you have selected is relevant to your area, considering that the laws of one state or county do not apply to another.

Review the form and examine a brief summary (if available) of scenarios for which the document could be applicable.

- Our platform provides an extensive assortment of over 85,000 ready-to-use state-specific forms suitable for nearly any legal circumstance.

- US Legal Forms is also an excellent tool for associates or legal advisors looking to save time by utilizing our DIY documents.

- Whether you need the San Jose California Deed of Trust Securing Promissory Note with no Payment Due Until Maturity and Interest Compounding Annually or any other documentation applicable in your state or county, US Legal Forms has everything readily available.

- Here’s how you can swiftly obtain the San Jose California Deed of Trust Securing Promissory Note with no Payment Due Until Maturity and Interest Compounding Annually using our reliable platform.

- If you are already a subscriber, you can proceed to Log In to your account to access the required form.

- However, if you are new to our platform, make sure to follow these instructions before downloading the San Jose California Deed of Trust Securing Promissory Note with no Payment Due Until Maturity and Interest Compounding Annually.

Form popularity

FAQ

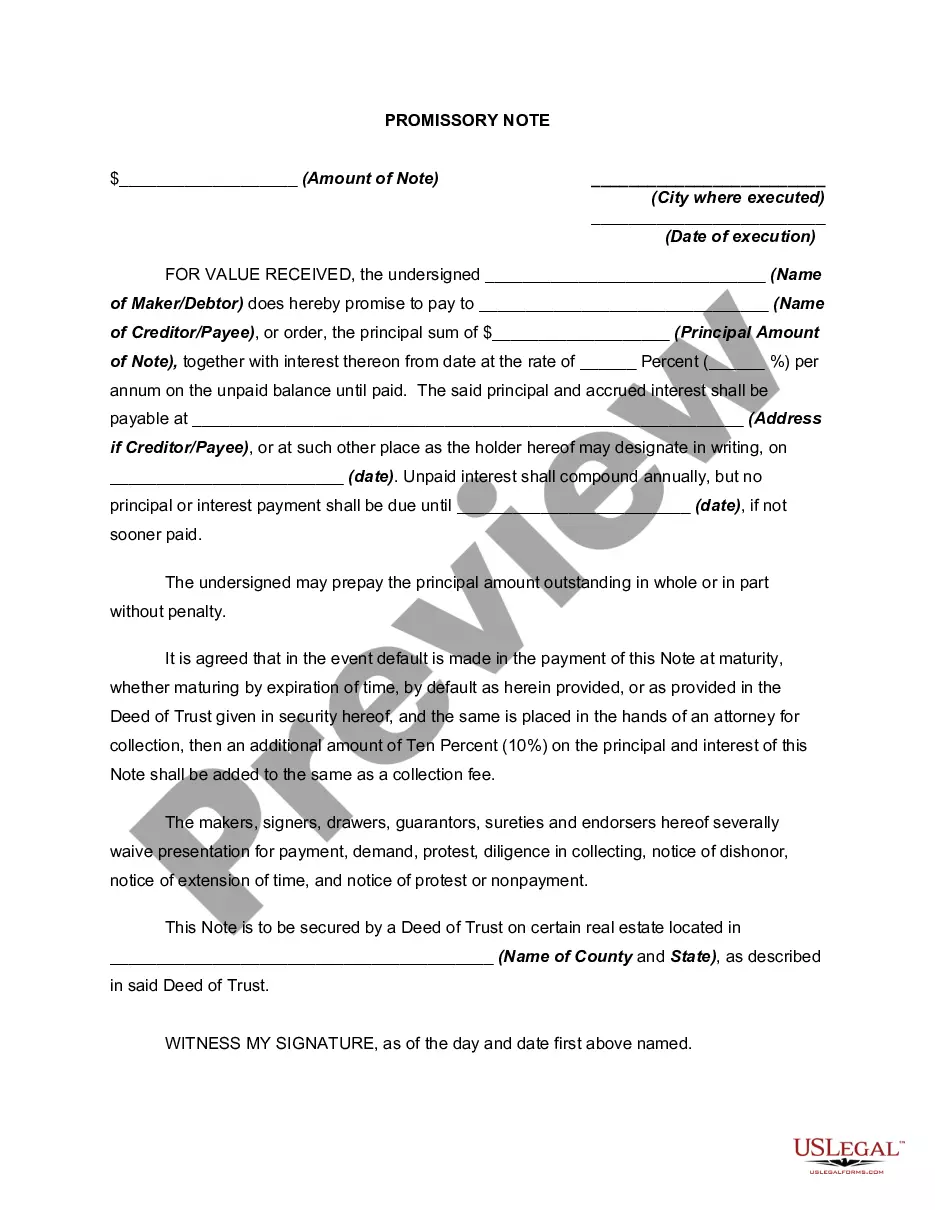

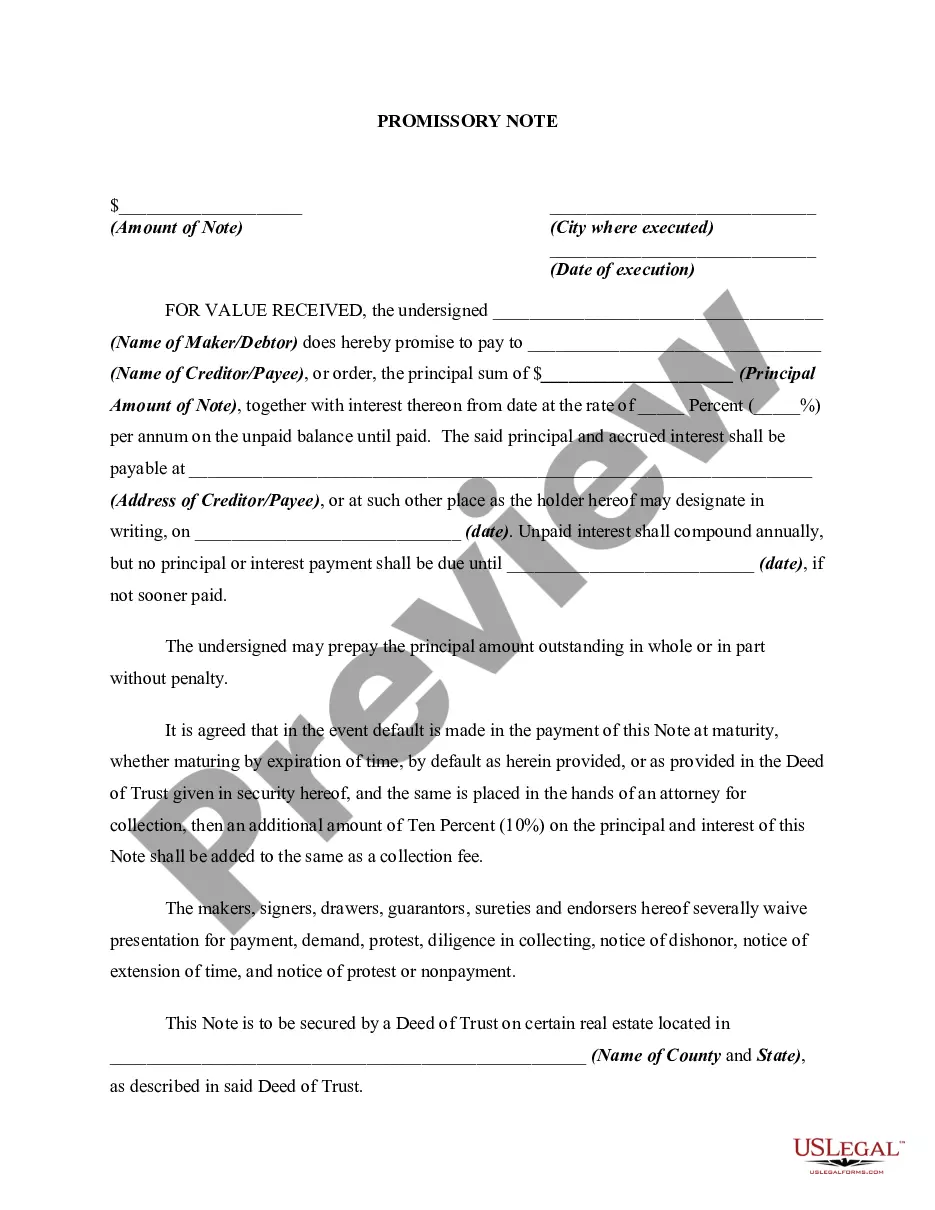

Secured Promissory Notes By assuring that the property attached to the note is of sufficient value to cover the amount of the loan, the payee thus has a guarantee of being repaid. The property that secures a note is called collateral, which can be either real estate or personal property.

A promissory note must include the date of the loan, the dollar amount, the names of both parties, the rate of interest, any collateral involved, and the timeline for repayment. When this document is signed by the borrower, it becomes a legally binding contract.

A promissory note and deed of trust have one simple function to secure the repayment of a loan by placing a lien on the property as collateral. If the loan is not paid, then the lender has the right to sell the property. Both documents are used to make sure the seller secures the repayment of the loan.

Promissory notes are legally binding contracts. That means when you don't pay back your loan, you could lose your collateral. If there's no collateral to secure the loan, the lender on the promissory note can take the borrower to court seeking repayment.

If you are owed money under a promissory note that has not been repaid in full, it may be necessary to file a breach of contract lawsuit.

A promissory note can become invalid if it excludes A) the total sum of money the borrower owes the lender (aka the amount of the note) or B) the number of payments due and the date each increment is due.

With a deed of trust, the lender gives the borrower the funds to make the purchase. The borrower provides the lender with a promissory note. The promissory note outlines the terms of the loan and the borrower's promise to pay. At this point, the borrower transfers the real property interest to the trustee.

What Happens When a Promissory Note Is Not Paid? Promissory notes are legally binding documents. Someone who fails to repay a loan detailed in a promissory note can lose an asset that secures the loan, such as a home, or face other actions.

Promissory notes are a valuable legal tool that any individual can use to legally bind another individual to an agreement for purchasing goods or borrowing money. A well-executed promissory note has the full effect of law behind it and is legally binding on both parties.

Loans from banks or other institutional lenders are always made using a number of documents, two of which are a promissory and security agreement. In general, the promissory note is your written promise to repay the loan and a security agreement is used when collateral is given for the loan.