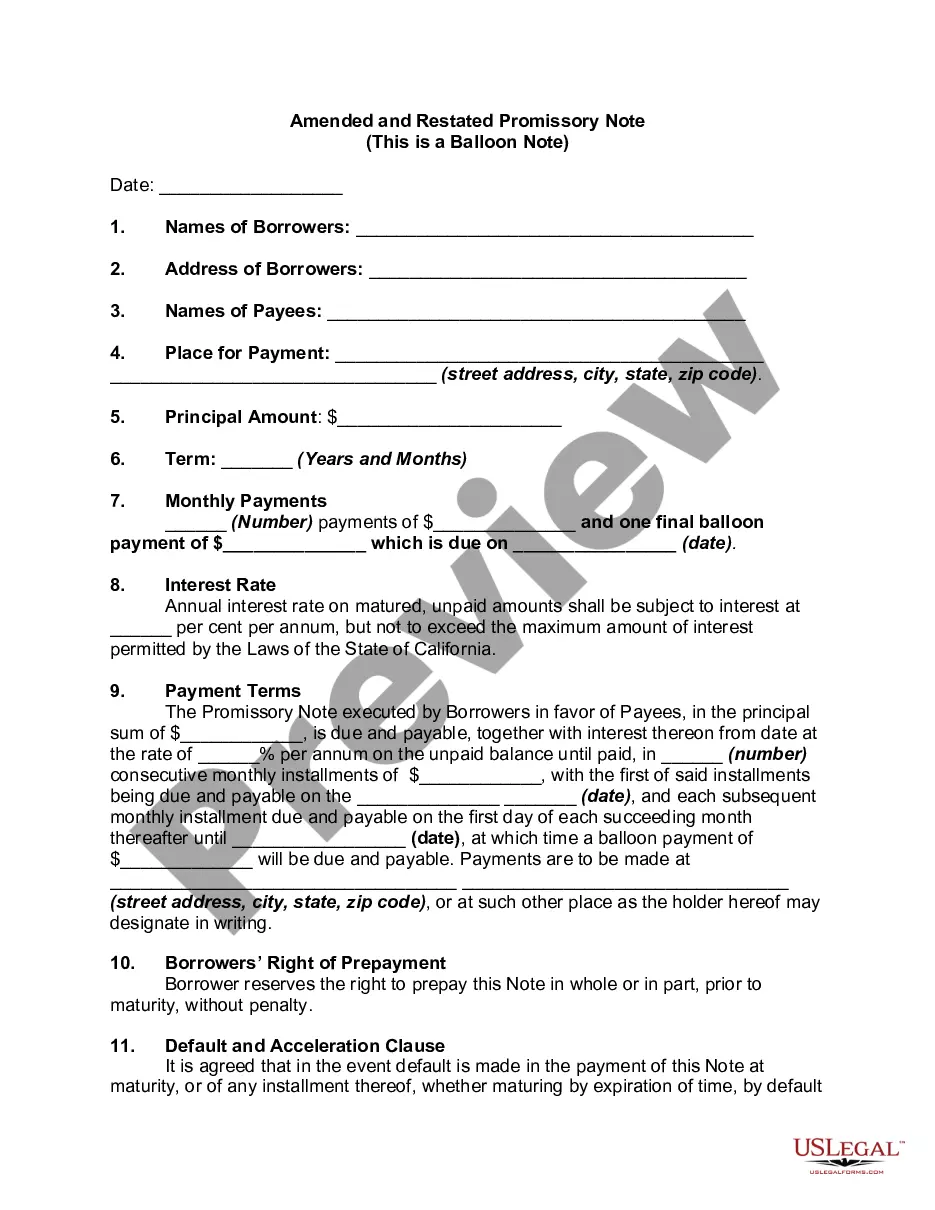

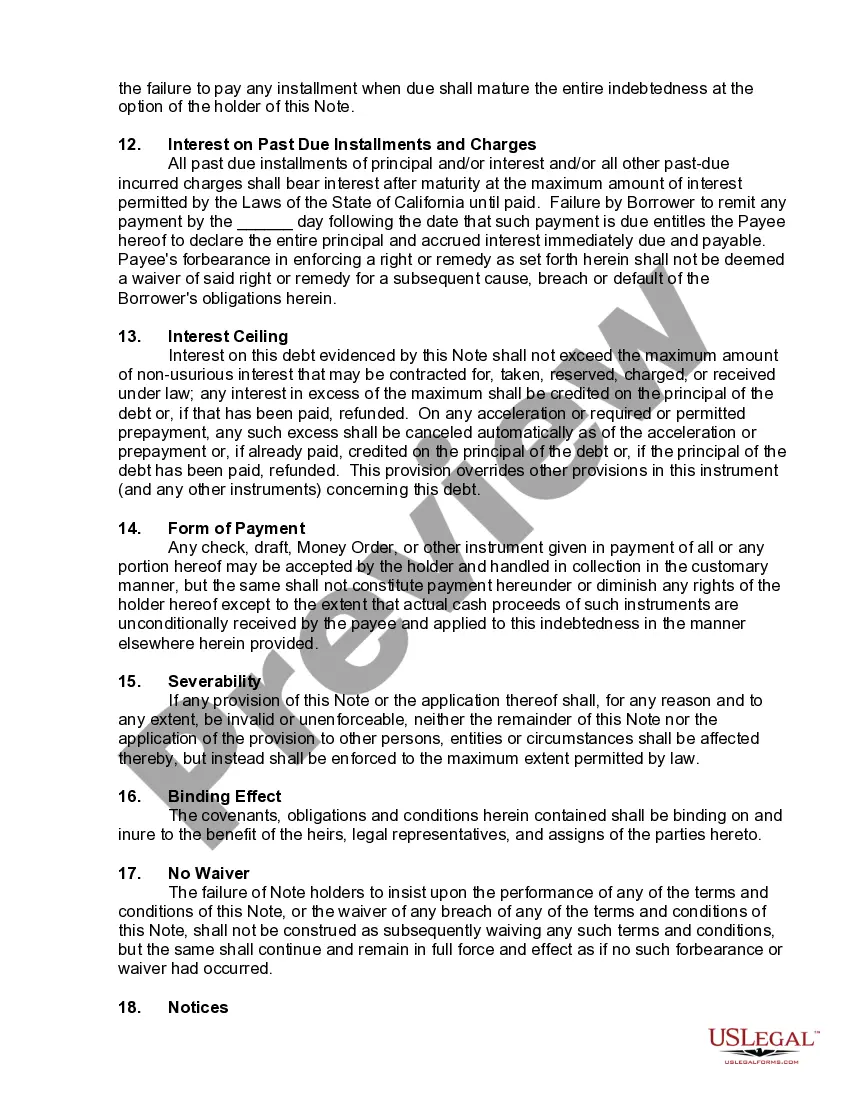

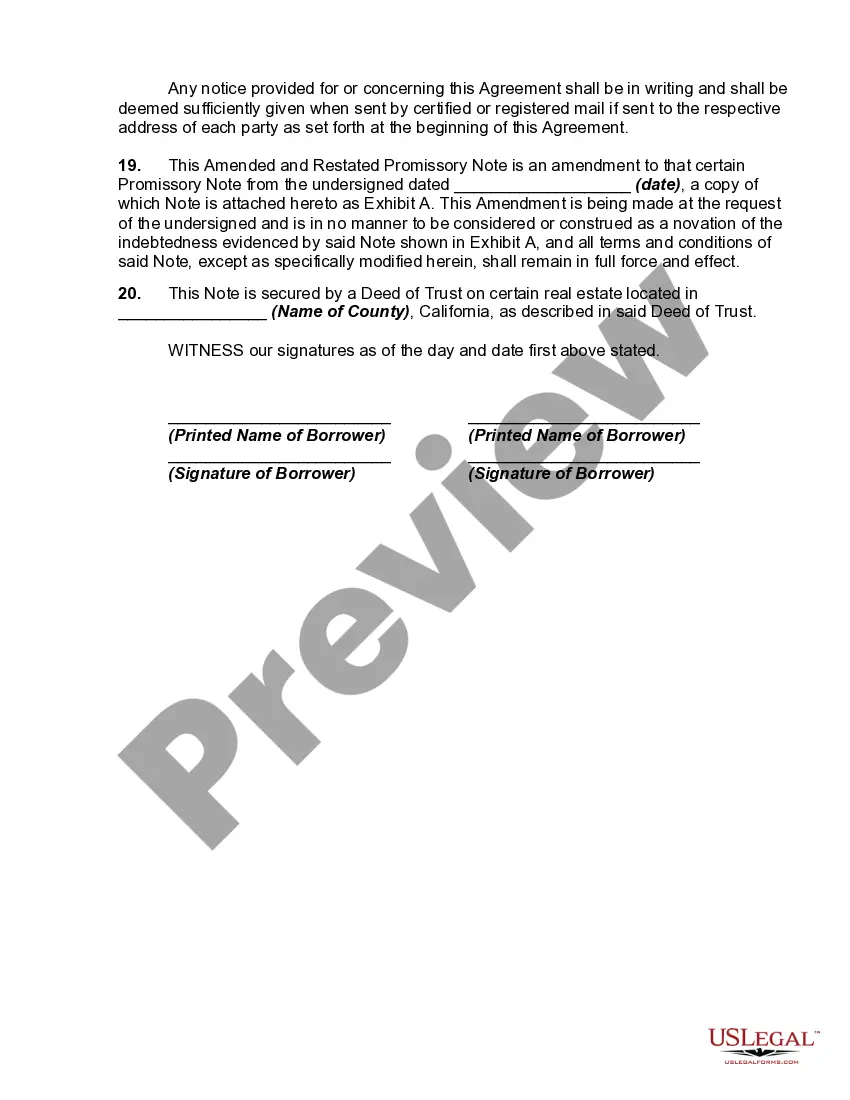

An amendment to a document is a change in a legal document made by adding, altering, or omitting a certain part or term. Amended documents, when properly executed (signed by all parties concerned), retain the legal validity of the original document.

A Santa Maria California Amended and Restated Promissory Note refers to a legal document that outlines the terms and conditions of a loan agreement between two parties in Santa Maria, California. This note serves as an amendment and restatement of a previously existing promissory note, updating and revising the terms to accommodate changes in the loan agreement. The Santa Maria California Amended and Restated Promissory Note specifies the amount of money borrowed, the interest rate, repayment schedule, and any additional terms agreed upon by the lender and borrower. By amending and restating the promissory note, both parties agree to supersede the previous note with the new terms. Common types of Santa Maria California Amended and Restated Promissory Notes include: 1. Real Estate Promissory Note: This type of promissory note is used when the loan is specifically intended for the purchase or refinancing of real estate properties in Santa Maria, California. It may include details related to the property, such as its address, legal description, and any collateral provided. 2. Business Promissory Note: This type of promissory note is used when the loan is provided for business purposes, such as financing equipment, expanding operations, or covering working capital needs. It may contain additional provisions specific to the borrower's business, such as personal guarantees or default clauses related to the success of the business. 3. Personal Promissory Note: This type of promissory note is used when the loan is made for personal reasons, such as funding education, consolidating debts, or covering medical expenses. The terms and conditions of the note are generally based on the borrower's creditworthiness and personal financial situation. 4. Secured Promissory Note: A secured promissory note involves the provision of collateral by the borrower to secure the loan. If the borrower fails to repay the loan according to the agreed terms, the lender has the right to seize and sell the collateral to recover their investment. Collateral can include assets such as real estate, vehicles, or valuable personal possessions. 5. Unsecured Promissory Note: In contrast to a secured promissory note, an unsecured promissory note does not require collateral. The borrower's ability to repay the loan is assessed solely based on their creditworthiness and financial standing. Consequently, the interest rate on an unsecured promissory note is generally higher compared to a secured one, as it carries greater risk for the lender. The use of a Santa Maria California Amended and Restated Promissory Note provides a clear and legally binding agreement between the lender and borrower, ensuring that both parties are aware of their obligations and rights. It is essential for borrowers to carefully review the terms and conditions before signing the note to ensure they are comfortable with the repayment plan and can fulfill their obligations. Likewise, lenders must accurately outline the terms to protect their interests and enforce their rights in case of default.A Santa Maria California Amended and Restated Promissory Note refers to a legal document that outlines the terms and conditions of a loan agreement between two parties in Santa Maria, California. This note serves as an amendment and restatement of a previously existing promissory note, updating and revising the terms to accommodate changes in the loan agreement. The Santa Maria California Amended and Restated Promissory Note specifies the amount of money borrowed, the interest rate, repayment schedule, and any additional terms agreed upon by the lender and borrower. By amending and restating the promissory note, both parties agree to supersede the previous note with the new terms. Common types of Santa Maria California Amended and Restated Promissory Notes include: 1. Real Estate Promissory Note: This type of promissory note is used when the loan is specifically intended for the purchase or refinancing of real estate properties in Santa Maria, California. It may include details related to the property, such as its address, legal description, and any collateral provided. 2. Business Promissory Note: This type of promissory note is used when the loan is provided for business purposes, such as financing equipment, expanding operations, or covering working capital needs. It may contain additional provisions specific to the borrower's business, such as personal guarantees or default clauses related to the success of the business. 3. Personal Promissory Note: This type of promissory note is used when the loan is made for personal reasons, such as funding education, consolidating debts, or covering medical expenses. The terms and conditions of the note are generally based on the borrower's creditworthiness and personal financial situation. 4. Secured Promissory Note: A secured promissory note involves the provision of collateral by the borrower to secure the loan. If the borrower fails to repay the loan according to the agreed terms, the lender has the right to seize and sell the collateral to recover their investment. Collateral can include assets such as real estate, vehicles, or valuable personal possessions. 5. Unsecured Promissory Note: In contrast to a secured promissory note, an unsecured promissory note does not require collateral. The borrower's ability to repay the loan is assessed solely based on their creditworthiness and financial standing. Consequently, the interest rate on an unsecured promissory note is generally higher compared to a secured one, as it carries greater risk for the lender. The use of a Santa Maria California Amended and Restated Promissory Note provides a clear and legally binding agreement between the lender and borrower, ensuring that both parties are aware of their obligations and rights. It is essential for borrowers to carefully review the terms and conditions before signing the note to ensure they are comfortable with the repayment plan and can fulfill their obligations. Likewise, lenders must accurately outline the terms to protect their interests and enforce their rights in case of default.