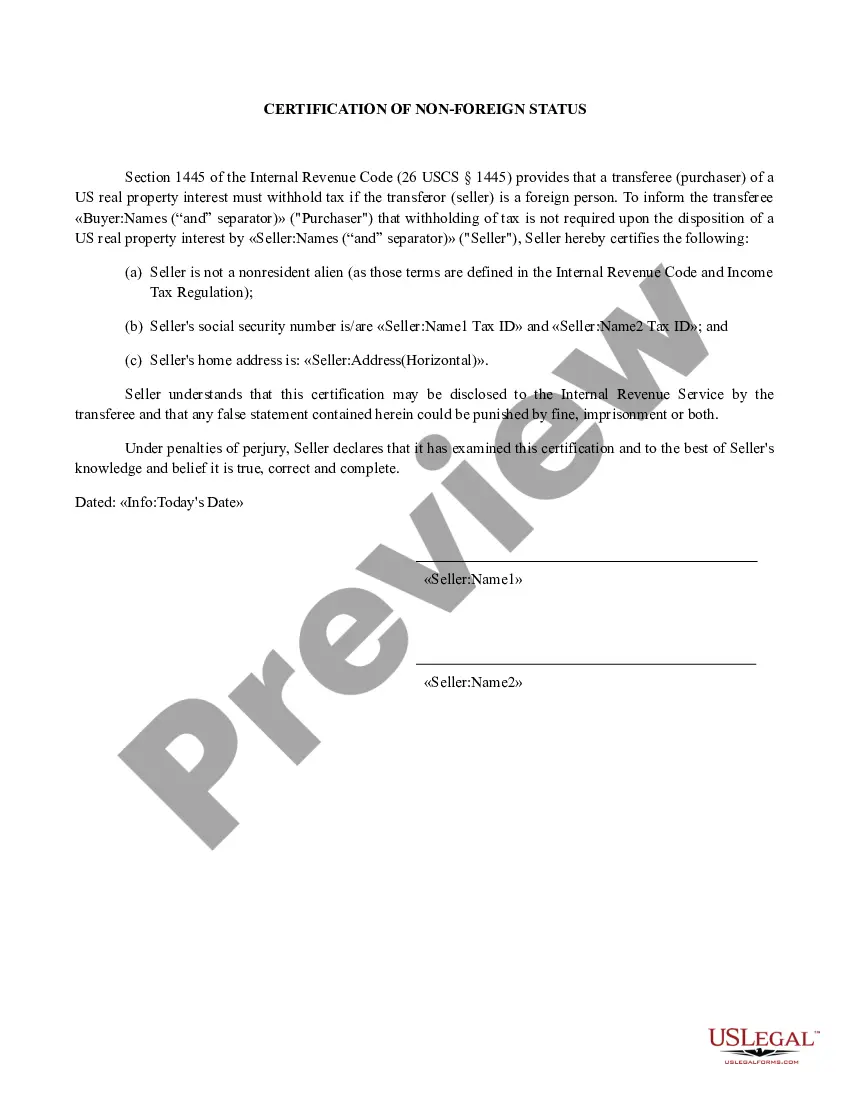

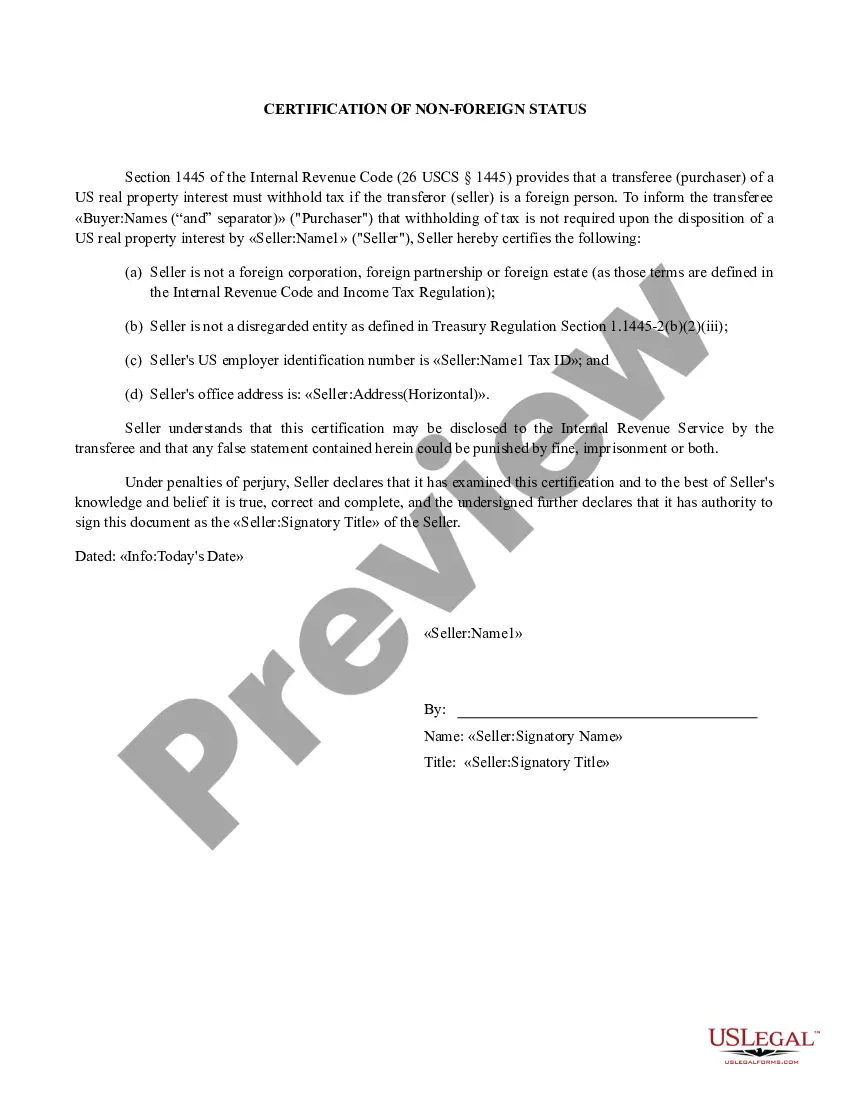

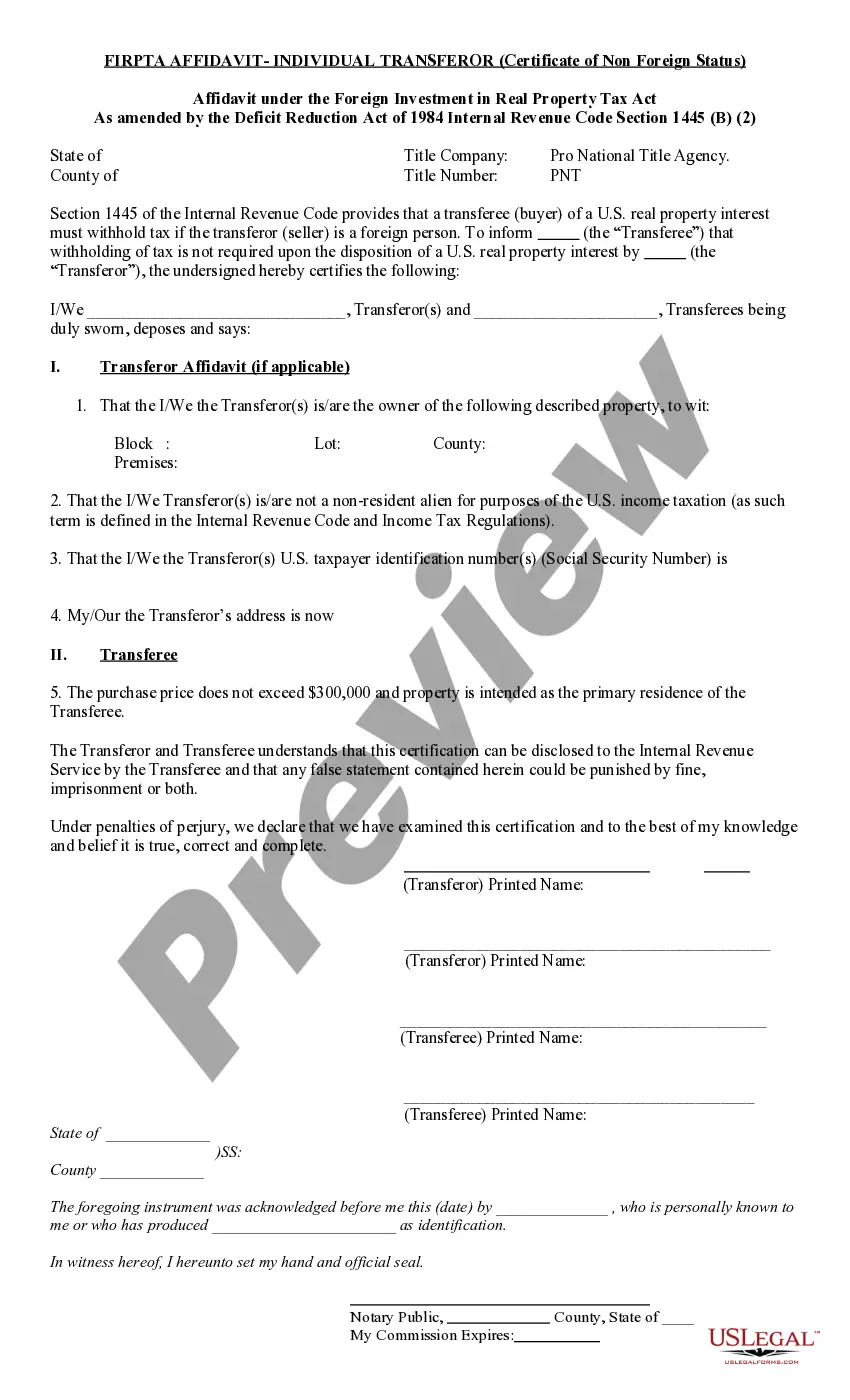

This Non-Foreign Affdavit Under Internal Revenue Code 1445 is for a seller of real property to sign stating that he or she is not a foreign person as defined by the Internal Revenue Code Section 26 USC 1445. This document must be signed and notarized.

Fullerton California Non-Foreign Affidavit Under IRC 1445

Category:

State:

California

City:

Fullerton

Control #:

CA-CLOSE7

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out California Non-Foreign Affidavit Under IRC 1445?

We consistently aim to minimize or evade legal repercussions in relation to intricate law-related or financial issues.

To achieve this, we enroll in legal services which are typically very costly.

Nonetheless, not all legal issues are equally intricate; many can be managed independently.

US Legal Forms is an online directory of current DIY legal templates covering a range of topics from wills and powers of attorney to articles of incorporation and petitions for dissolution.

Simply Log In to your account and click the Get button next to it. If you happen to misplace the document, you can always retrieve it again in the My documents section. The procedure is just as simple if you're new to the platform! You can create an account in just a few minutes. Ensure that the Fullerton California Non-Foreign Affidavit Under IRC 1445 complies with the laws and regulations of your state and locality. Additionally, it’s essential to review the form’s outline (if available), and if you find any inconsistencies with your initial requirements, search for an alternative form. Once you confirm that the Fullerton California Non-Foreign Affidavit Under IRC 1445 meets your needs, you can choose a subscription option and proceed to payment. Then, you can download the document in any compatible format. For over 24 years, we’ve assisted millions by offering customizable and up-to-date legal documents. Maximize your benefits from US Legal Forms now to conserve time and resources!

- Our repository empowers you to handle your affairs without the assistance of legal advisors.

- We provide access to legal document templates that are often not publicly available.

- Our templates are tailored to specific states and regions, greatly simplifying the search process.

- Take advantage of US Legal Forms whenever you need to easily and securely find and download the Fullerton California Non-Foreign Affidavit Under IRC 1445 or any other document.

Form popularity

FAQ

To avoid capital gains tax on foreign property, you should be aware of certain exemptions and strategies. Utilizing a Fullerton California Non-Foreign Affidavit Under IRC 1445 can play a vital role, especially if you can demonstrate that you are not a foreign investor. Consider consulting with a tax advisor or using platforms like uslegalforms to navigate your options effectively and ensure compliance with tax regulations.

Avoiding FIRPTA tax requires you to file a Fullerton California Non-Foreign Affidavit Under IRC 1445 before the sale of your property. By doing so, you can assert that you are not a foreign individual and, consequently, avoid the withholding requirements associated with FIRPTA. Accurate and timely submission of this affidavit is crucial, and utilizing resources like uslegalforms can assist you in this process.

You can obtain a FIRPTA exemption by properly completing a Fullerton California Non-Foreign Affidavit Under IRC 1445. This affidavit allows you to confirm that you are not classified as a foreign person, thus qualifying for the exemption. Ensure that your documentation is thorough, as this will help facilitate a smoother process during your real estate transaction.

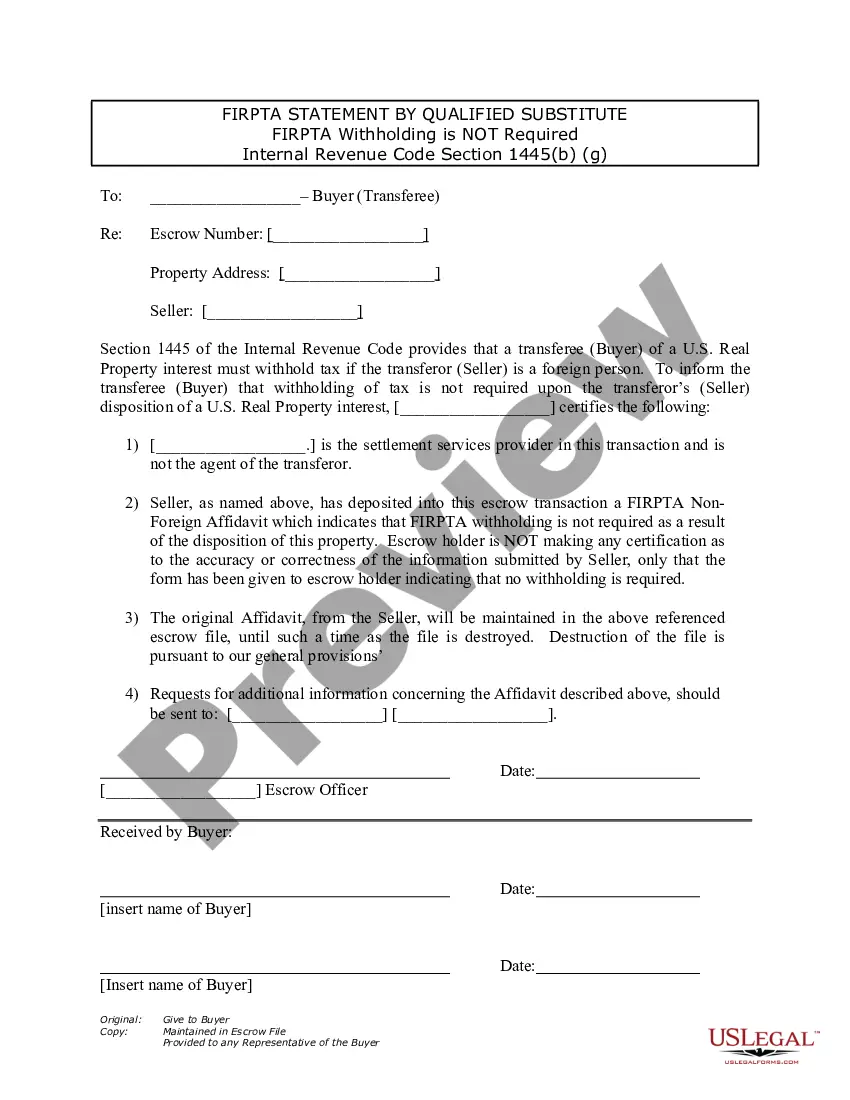

To avoid the 15% withholding tax under the Foreign Investment in Real Property Tax Act (FIRPTA), you can file a Fullerton California Non-Foreign Affidavit Under IRC 1445. This affidavit certifies that you are not a foreign person and helps eliminate the withholding requirement. It's essential to complete the affidavit accurately and submit it in a timely manner to the appropriate parties involved in the transaction.

foreign status affidavit is a document that verifies a seller is not a foreign person under IRS rules. This affidavit is essential in real estate transactions to exempt buyers from FIRPTA withholding requirements. Utilizing the Fullerton California NonForeign Affidavit Under IRC 1445 provides assurance to buyers that they do not need to withhold funds, facilitating smoother transactions. This document is a valuable tool for both buyers and sellers in real estate dealings.

The buyer of the property is primarily responsible for FIRPTA withholding when the seller is a foreign person. This responsibility is crucial to ensure that IRS regulations are met during the transaction. The buyer may request the seller to complete a Fullerton California Non-Foreign Affidavit Under IRC 1445 to confirm that they are not a foreign seller. Understanding this responsibility can help streamline the buying process and mitigate potential tax risks.

You can report foreign withholding on your annual U.S. tax return using Form 1040 or 1040NR. This includes any FIRPTA withholdings where a sale or exchange of U.S. real property occurred. Be sure to keep accurate records, including the amounts reported on the Fullerton California Non-Foreign Affidavit Under IRC 1445, as this may affect your reporting. Properly reporting withholding ensures compliance with IRS regulations and helps prevent future complications.

To reclaim FIRPTA withholding, you must file a U.S. tax return for the year in which the withholding occurred. You'll report the amount withheld and any applicable deductions or credits. If you meet the criteria for a refund, the IRS will process your return and return the withheld funds. Utilizing a Fullerton California Non-Foreign Affidavit Under IRC 1445 can help support your case if you qualify for a refund.

Filing FIRPTA withholding involves several steps to comply with the IRS requirements. First, you need to determine if the seller is a foreign person, which may require the use of the Fullerton California Non-Foreign Affidavit Under IRC 1445. Then, complete and submit IRS Form 8288 along with payment of the required withholding amount. Lastly, provide the seller with a copy of the form to ensure proper records are maintained for IRS purposes.

Section 1445 of the Internal Revenue Code (IRC) deals with withholding tax requirements on foreign persons selling U.S. real estate. This section mandates that buyers withhold a specific percentage of the amount realized on the sale if the seller is a foreign person. By understanding Section 1445, you can better navigate the process of dealing with foreign buyers and avoid potential tax issues when handling property transactions. Ensure you utilize a Fullerton California Non-Foreign Affidavit Under IRC 1445 to confirm your non-foreign status and simplify your dealings.