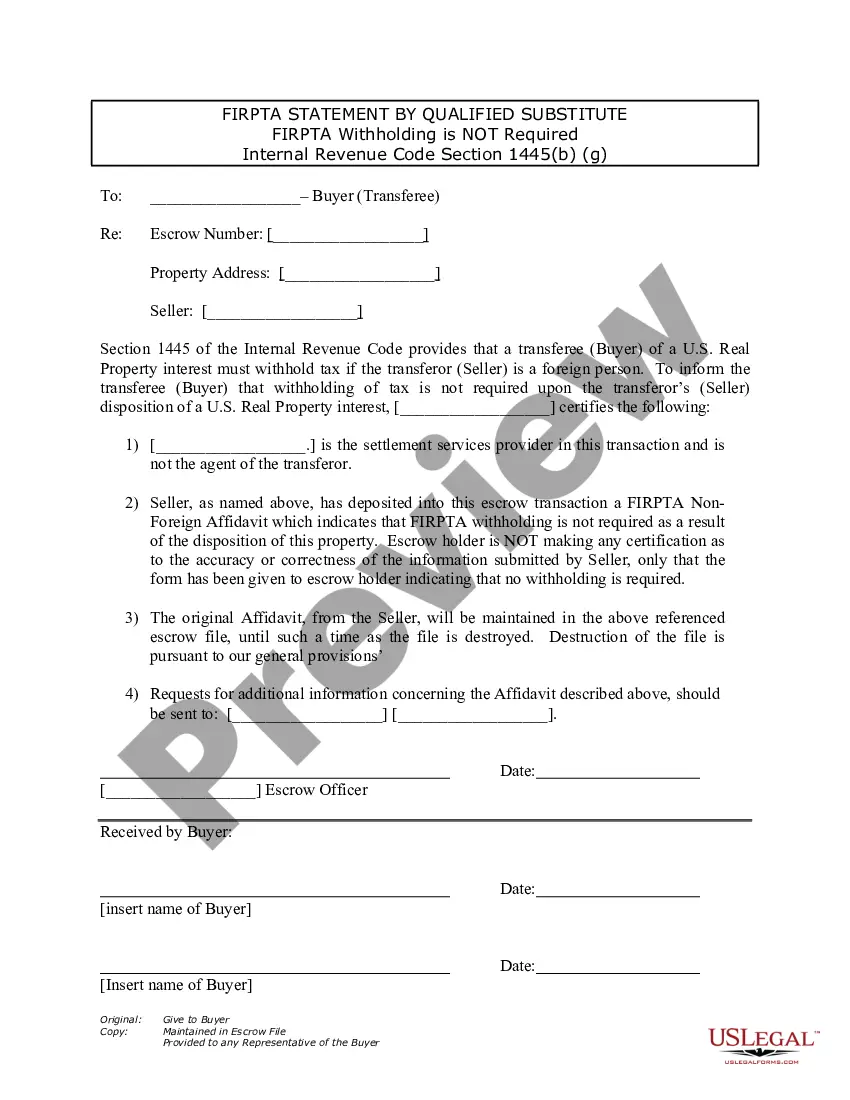

This Non-Foreign Affdavit Under Internal Revenue Code 1445 is for a seller of real property to sign stating that he or she is not a foreign person as defined by the Internal Revenue Code Section 26 USC 1445. This document must be signed and notarized.

San Jose California Non-Foreign Affidavit Under IRC 1445

Category:

State:

California

City:

San Jose

Control #:

CA-CLOSE7

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out California Non-Foreign Affidavit Under IRC 1445?

We consistently aim to lessen or avert legal complications when navigating intricate legal or financial issues.

To achieve this, we seek attorney options that are often very expensive.

Nevertheless, not every legal situation is equally intricate; many can be handled by ourselves.

US Legal Forms is an online repository of current DIY legal documents encompassing everything from wills and power of attorney to articles of incorporation and petitions for dissolution.

Simply Log In to your account and click the Get button next to it. If you happen to misplace the document, you can re-download it any time in the My documents section. The process is just as simple if you are a newcomer to the platform! You can create your account in just a few minutes. Ensure to verify if the San Jose California Non-Foreign Affidavit Under IRC 1445 aligns with the legislation and requirements of your state and area. Additionally, it's vital that you review the form's outline (if available), and if you find any inconsistencies with what you initially sought, search for an alternative form. Once you've confirmed that the San Jose California Non-Foreign Affidavit Under IRC 1445 suits your situation, you can choose the subscription plan and proceed to the payment. You can then download the document in any provided format. For over 24 years of our operation, we've assisted millions by offering customizable and current legal forms. Make the most of US Legal Forms now to conserve time and resources!

- Our repository empowers you to manage your affairs independently without relying on legal assistance.

- We offer access to legal form templates that are not always accessible to the public.

- Our templates are tailored to your state and region, significantly easing the search process.

- Utilize US Legal Forms whenever you need to locate and download the San Jose California Non-Foreign Affidavit Under IRC 1445 or any other form quickly and securely.

Form popularity

FAQ

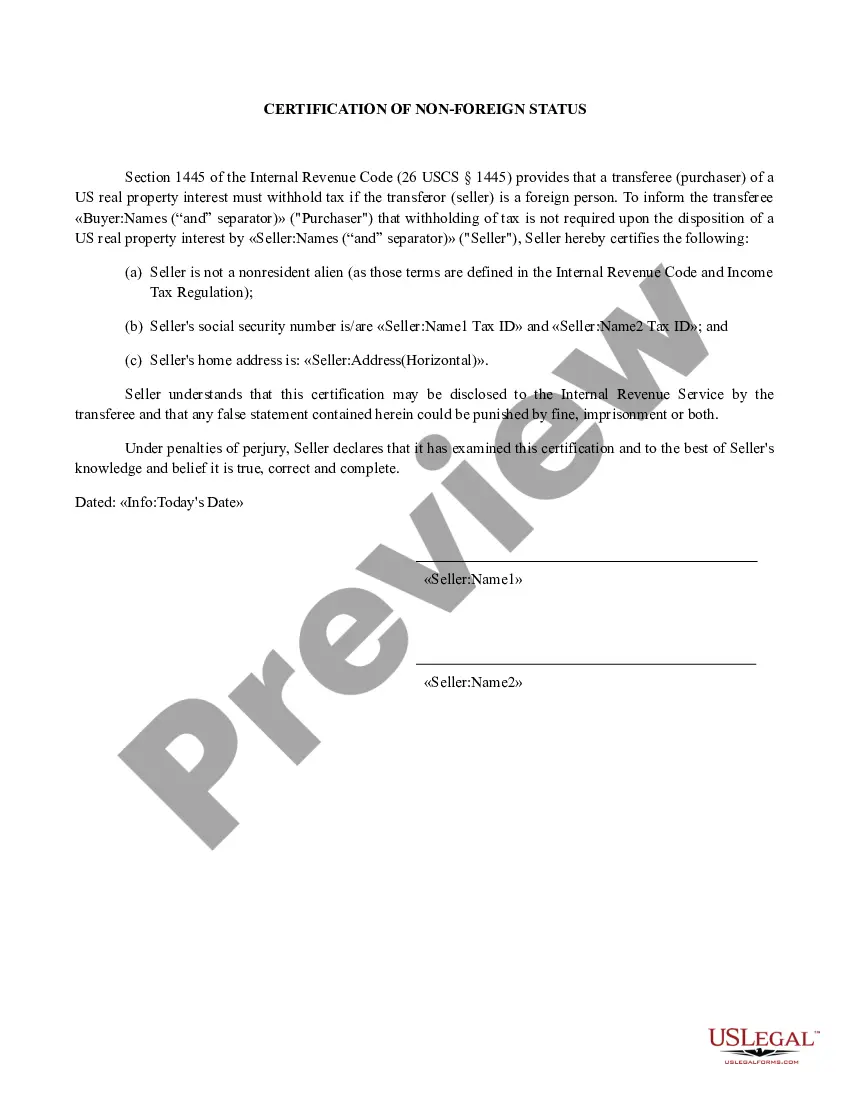

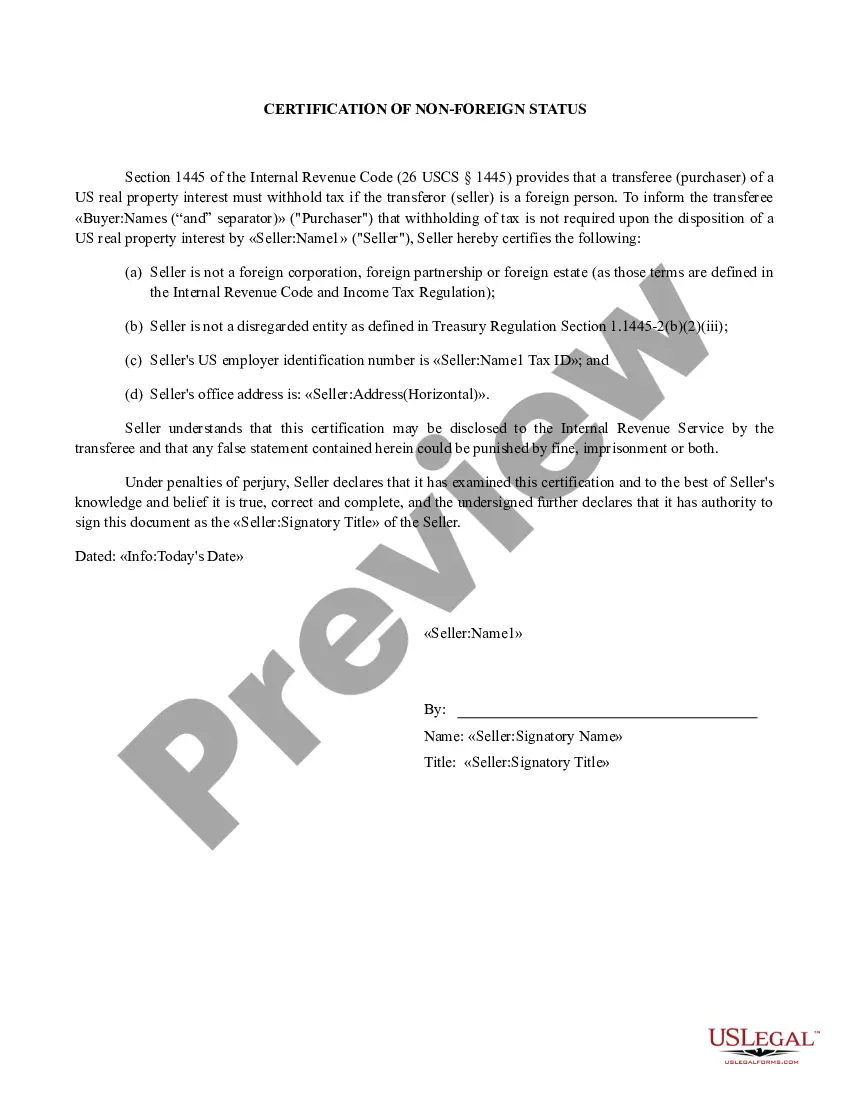

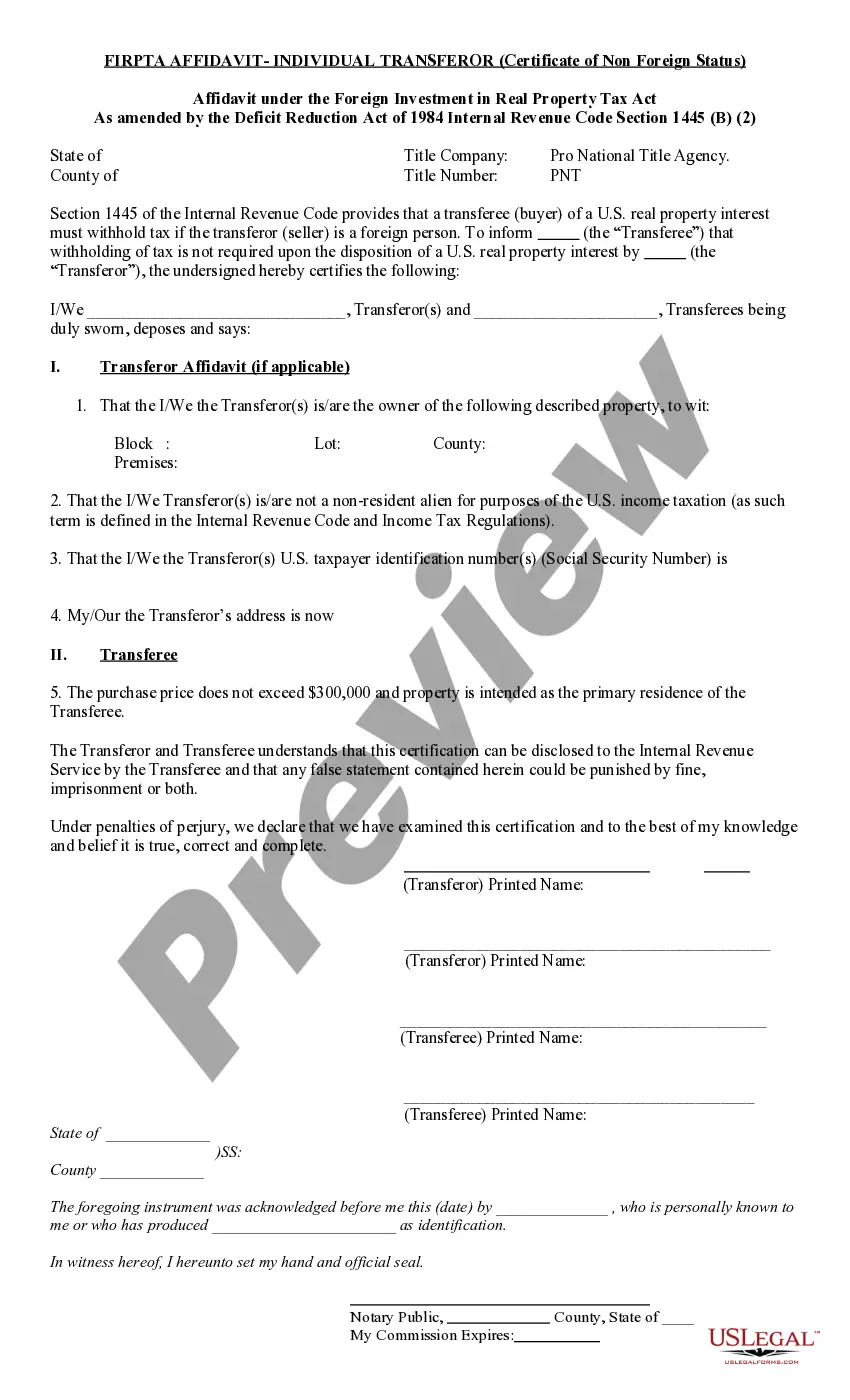

Certification of Non-Foreign Status means an affidavit, signed under penalty of perjury by an authorized officer of Borrower, stating (a) that Borrower is not a ?foreign corporation,? ?foreign partnership,? ?foreign trust,? or ?foreign estate,? as those terms are defined in the Code and the regulations promulgated

How to Complete a FIRPTA form - Seller's affidavit of non-foreign status YouTube Start of suggested clip End of suggested clip Just go the listing agent. And say then send me over a qualified substitute a qs form. And that'sMoreJust go the listing agent. And say then send me over a qualified substitute a qs form. And that's going to have the name of the escort teller company that's in possession of this affidavit.

A FIRPTA affidavit, also known as Affidavit of Non-Foreign Status, is a form a seller purchasing a U.S. property uses to certify under oath that they aren't a foreign citizen. The form includes the seller's name, U.S. taxpayer identification number and home address.

A citizen or resident of the United States, ? A domestic partnership, or ? A domestic corporation, or ? An estate or trust (other than a foreign estate of foreign trust as those terms are defined in Section 7701 (a) (31) of the Code.

In general, IRC § 1445 requires the purchaser of a USRPI from a foreign person to withhold 10 percent (or more) of the amount realized on the disposition.

Certification of Non-Foreign Status means an affidavit, signed under penalty of perjury by an authorized officer of Borrower, stating (a) that Borrower is not a ?foreign corporation,? ?foreign partnership,? ?foreign trust,? or ?foreign estate,? as those terms are defined in the Code and the regulations promulgated

In order to avoid issues with FIRPTA, the seller will sign an Affidavit and certify status. Otherwise, various pesky IRS forms, such as Form 8288 may be required.

A foreign corporation that distributes a U.S. real property interest must withhold a tax equal to 21% of the gain it recognizes on the distribution to its shareholders.

The Foreign Investment in Real Property Tax Act (FIRPTA) is a tax imposed on the amount realized from the sale of real property owned by a foreign seller. There are exceptions to this tax-withholding requirement.