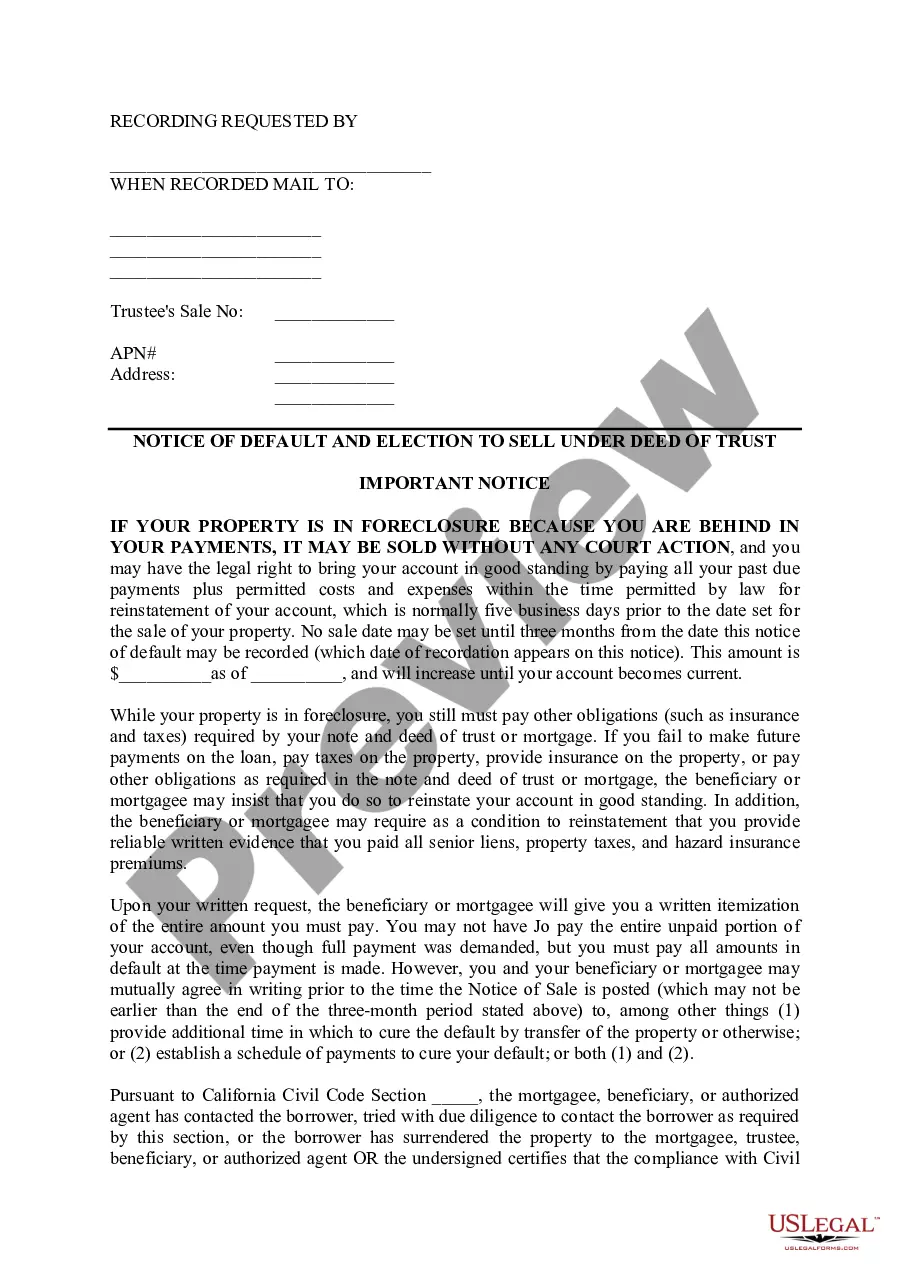

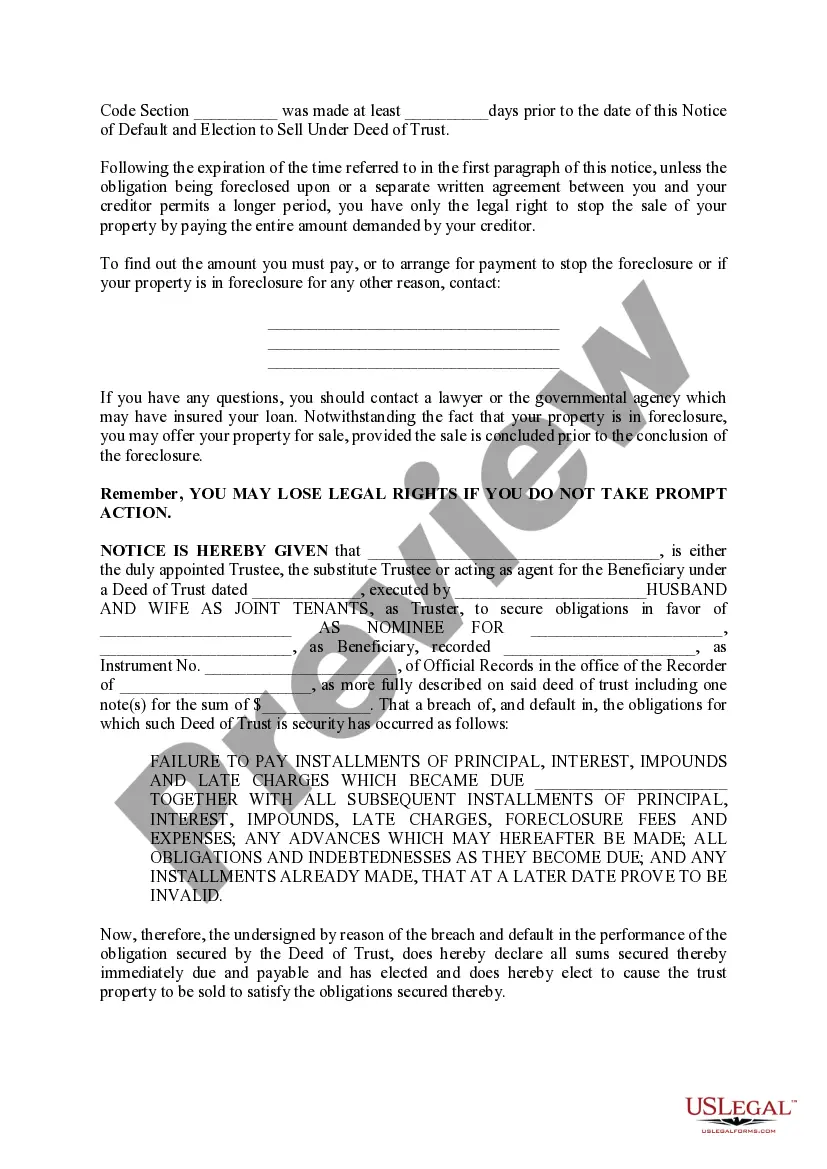

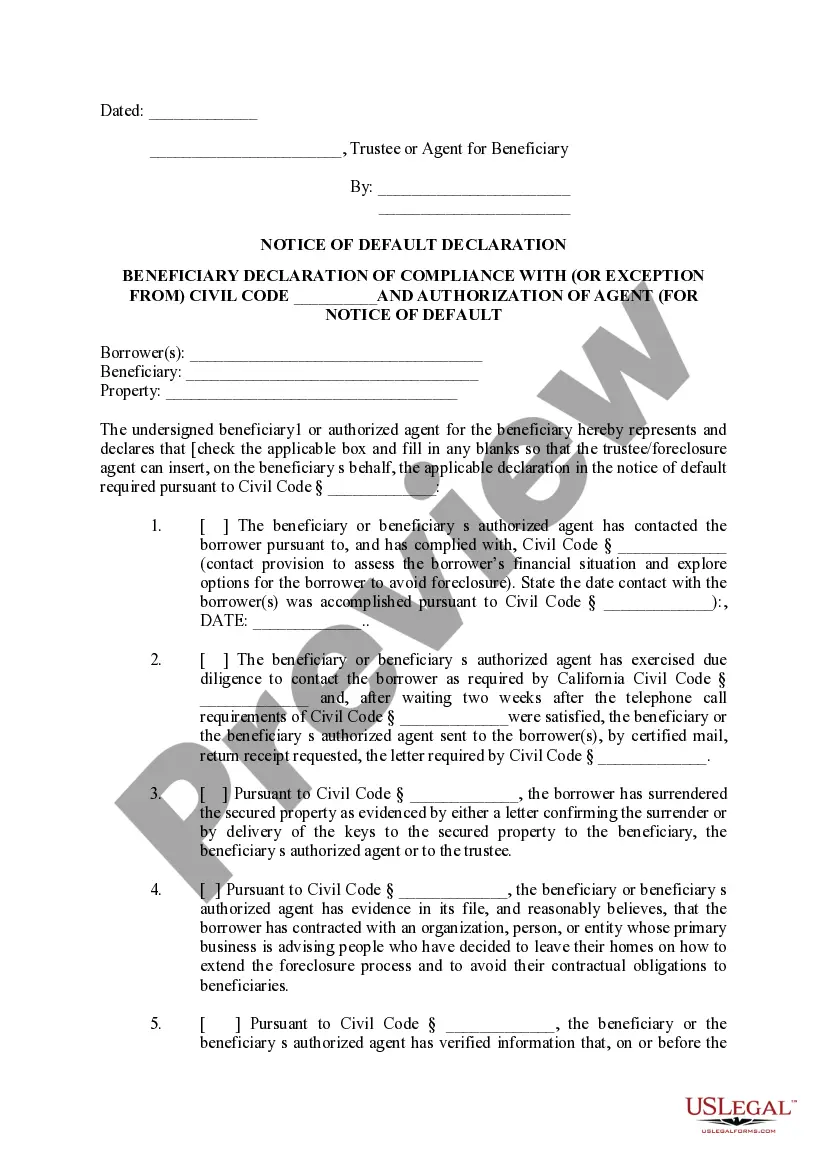

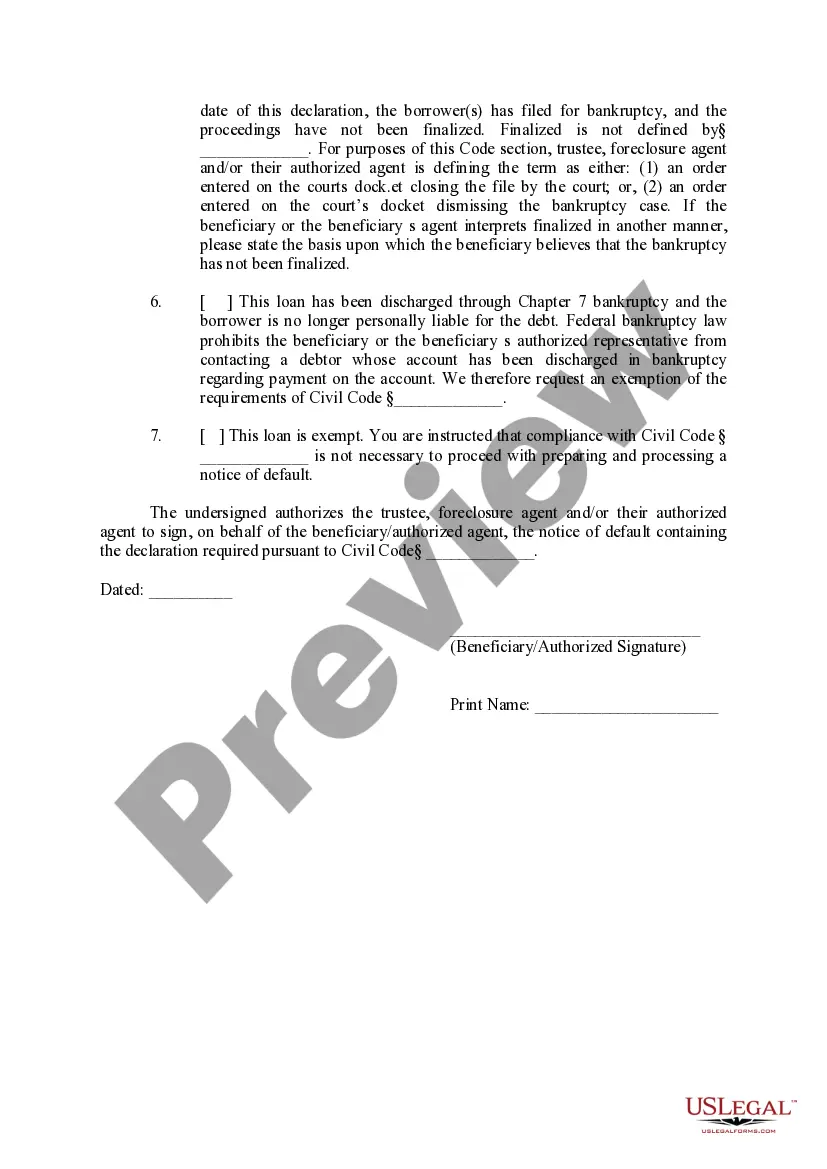

Hayward California Notice of Default and Election to Sell Under Deed of Trust is a legal document filed by a lender when a borrower defaults on their mortgage payments. This notice initiates the foreclosure process and gives the borrower a specified period to remedy the default or face the potential sale of their property. The Hayward California Notice of Default and Election to Sell Under Deed of Trust is a crucial step in the foreclosure process, as it formally notifies the borrower of their default and the lender's intent to sell the property. This notice is typically served to the borrower in person or via certified mail and is also recorded with the county recorder's office to create a public record. There are different types of Hayward California Notice of Default and Election to Sell Under Deed of Trust, including: 1. Standard Notice of Default: This is the initial notice sent to the borrower after a certain number of missed payments. It specifies the amount of arrears, the total amount due, and the timeline to reinstate the loan or face foreclosure. 2. Notice of Default and Opportunity to Cure: This notice notifies the borrower that they have an opportunity to cure the default by paying the overdue amount within a specific period. Once the default is cured, the foreclosure process is halted. 3. Notice of Default and Intent to Accelerate: This notice is issued when the borrower fails to cure the default within the specified period. It accelerates the loan, making the entire balance due immediately, and sets a date for the foreclosure sale. 4. Notice of Trustee's Sale: After the Notice of Default and Intent to Accelerate, the lender may issue a Notice of Trustee's Sale. This notice informs the borrower and the public about the upcoming auction of the property, disclosing the sale date, time, and location. It is important for borrowers to understand the implications of receiving a Hayward California Notice of Default and Election to Sell Under Deed of Trust. They should consult with legal professionals or housing counselors to explore options to avoid foreclosure, such as loan modification, repayment plans, or seeking assistance from government programs. Acting promptly and seeking guidance can help borrowers navigate the foreclosure process and potentially save their homes.

Hayward California Notice of Default and Election to Sell Under Deed of Trust

Description

How to fill out Hayward California Notice Of Default And Election To Sell Under Deed Of Trust?

If you are looking for a valid form template, it’s extremely hard to choose a more convenient service than the US Legal Forms site – one of the most considerable libraries on the internet. Here you can get thousands of form samples for business and personal purposes by categories and regions, or keywords. Using our high-quality search feature, discovering the most up-to-date Hayward California Notice of Default and Election to Sell Under Deed of Trust is as elementary as 1-2-3. Moreover, the relevance of each file is proved by a team of professional attorneys that regularly review the templates on our platform and update them based on the latest state and county requirements.

If you already know about our platform and have a registered account, all you should do to receive the Hayward California Notice of Default and Election to Sell Under Deed of Trust is to log in to your profile and click the Download button.

If you use US Legal Forms for the first time, just follow the guidelines below:

- Make sure you have chosen the sample you need. Look at its description and make use of the Preview function (if available) to see its content. If it doesn’t meet your requirements, use the Search field at the top of the screen to discover the proper record.

- Confirm your decision. Choose the Buy now button. After that, choose your preferred subscription plan and provide credentials to sign up for an account.

- Process the financial transaction. Use your credit card or PayPal account to complete the registration procedure.

- Get the form. Select the file format and download it to your system.

- Make modifications. Fill out, edit, print, and sign the acquired Hayward California Notice of Default and Election to Sell Under Deed of Trust.

Each form you add to your profile has no expiration date and is yours forever. You can easily access them using the My Forms menu, so if you want to get an additional duplicate for enhancing or creating a hard copy, you can come back and download it again at any time.

Take advantage of the US Legal Forms extensive catalogue to get access to the Hayward California Notice of Default and Election to Sell Under Deed of Trust you were looking for and thousands of other professional and state-specific templates on one platform!