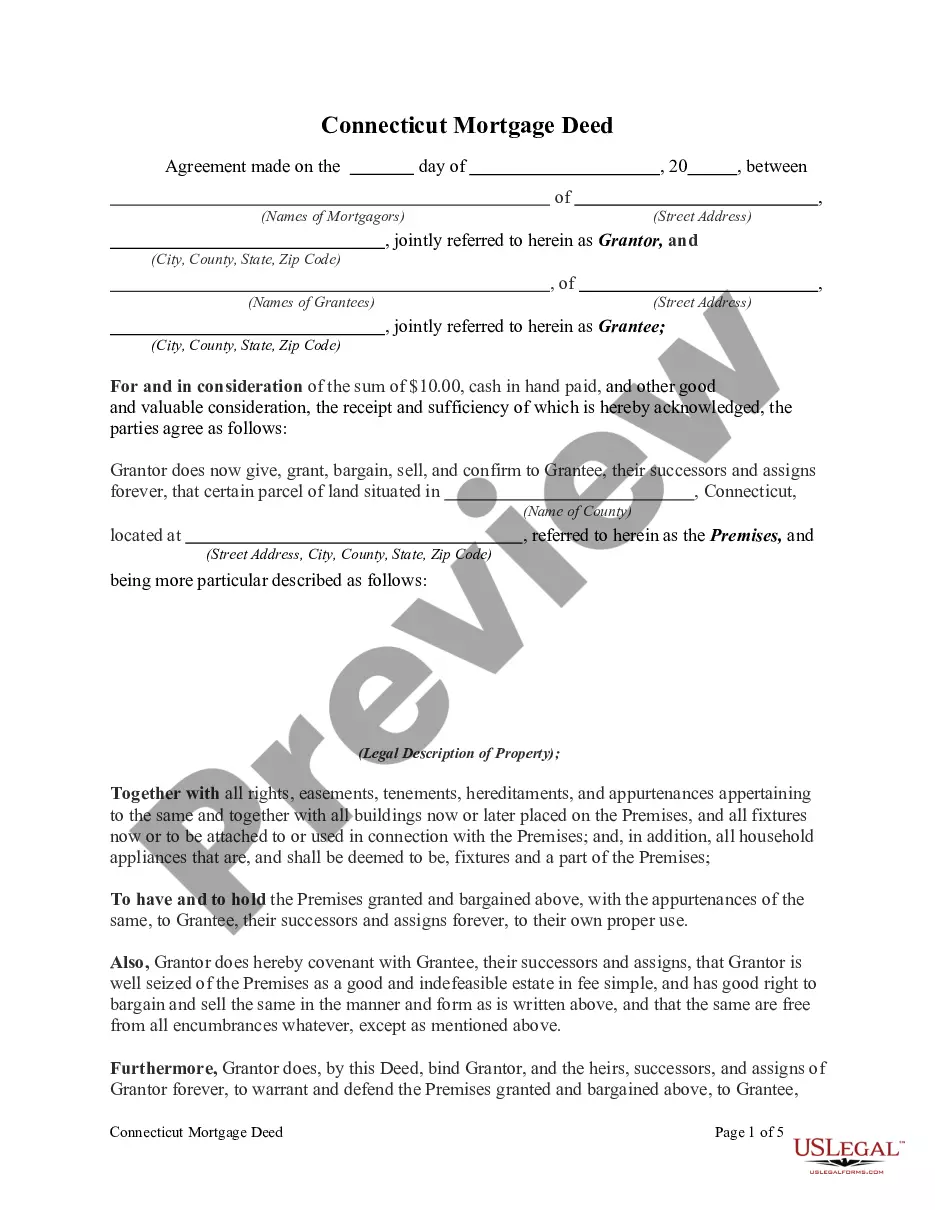

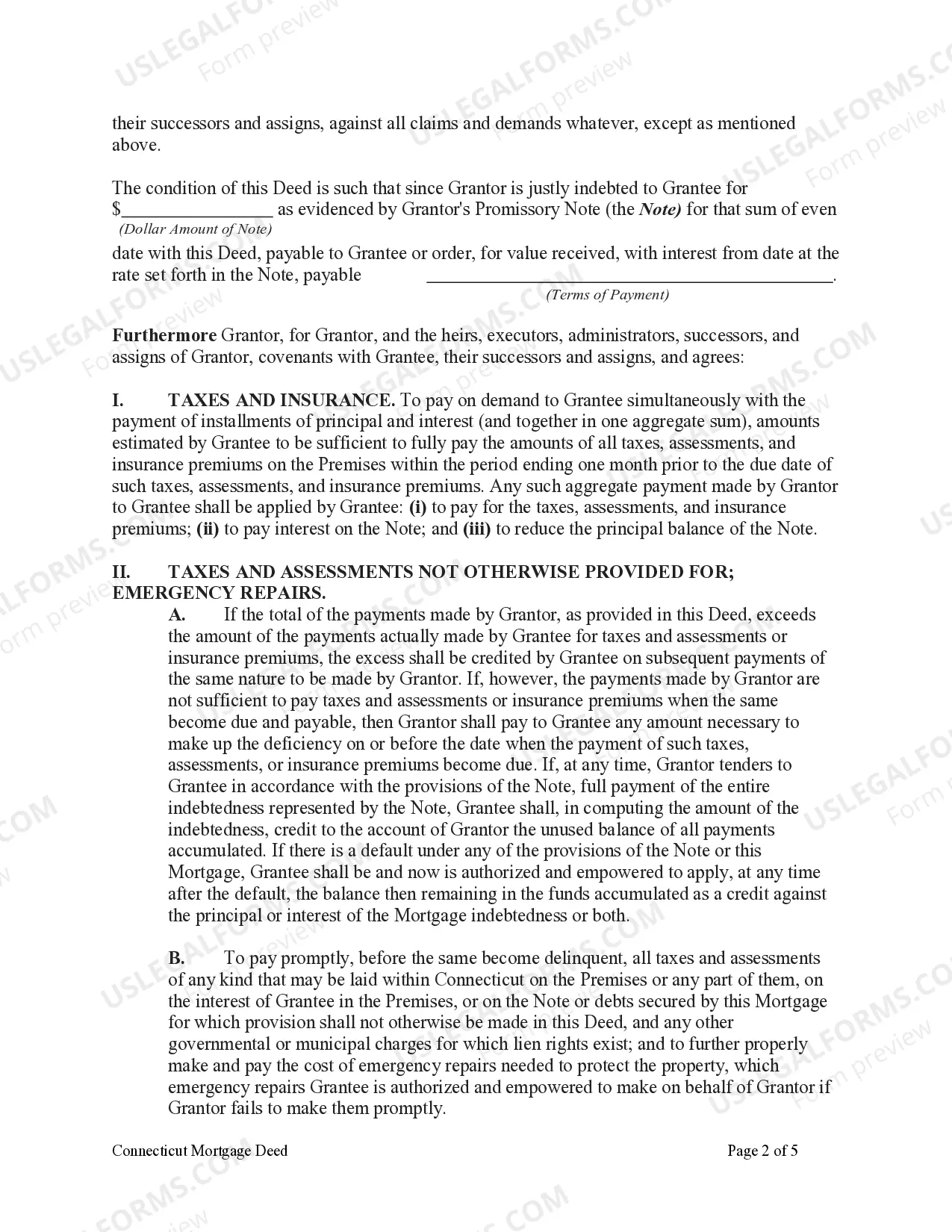

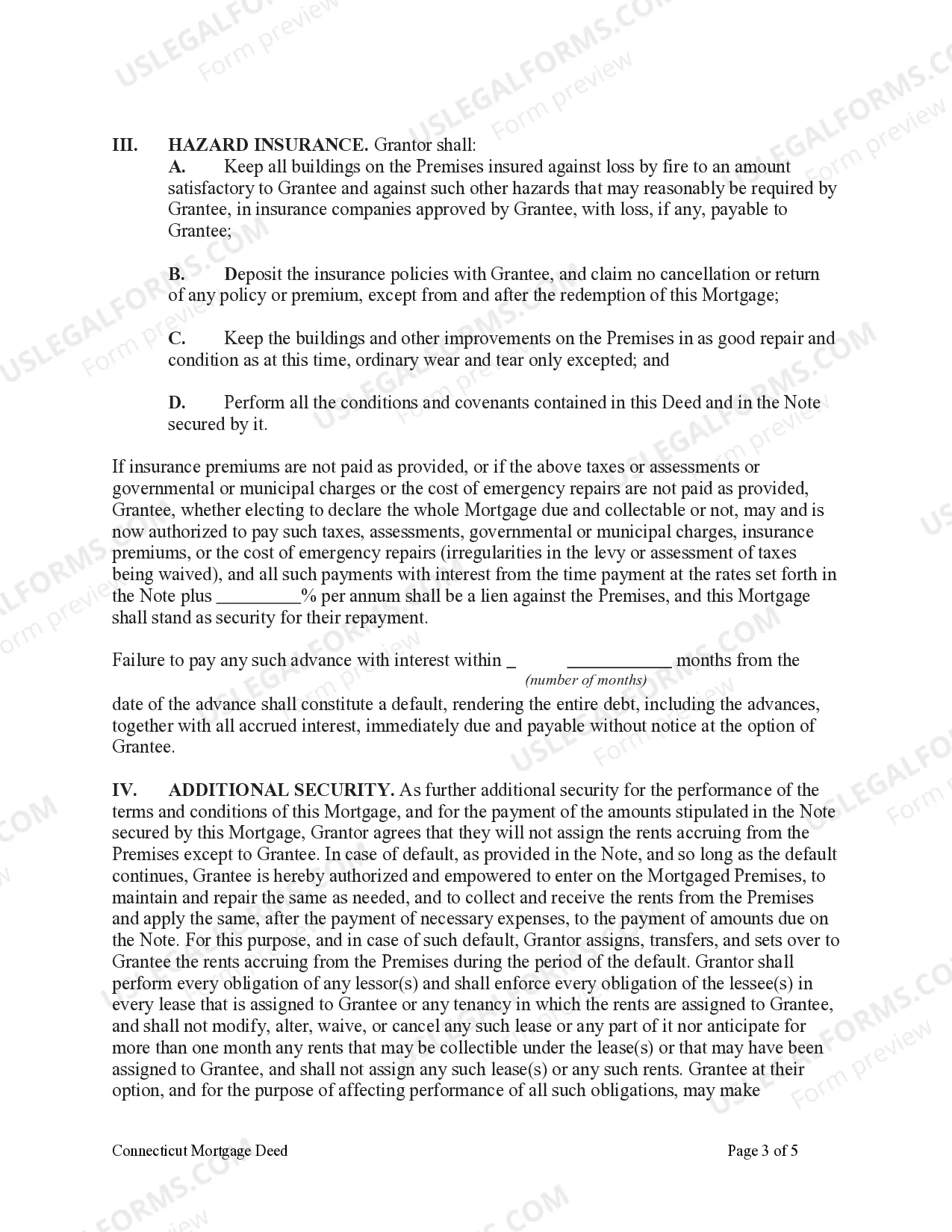

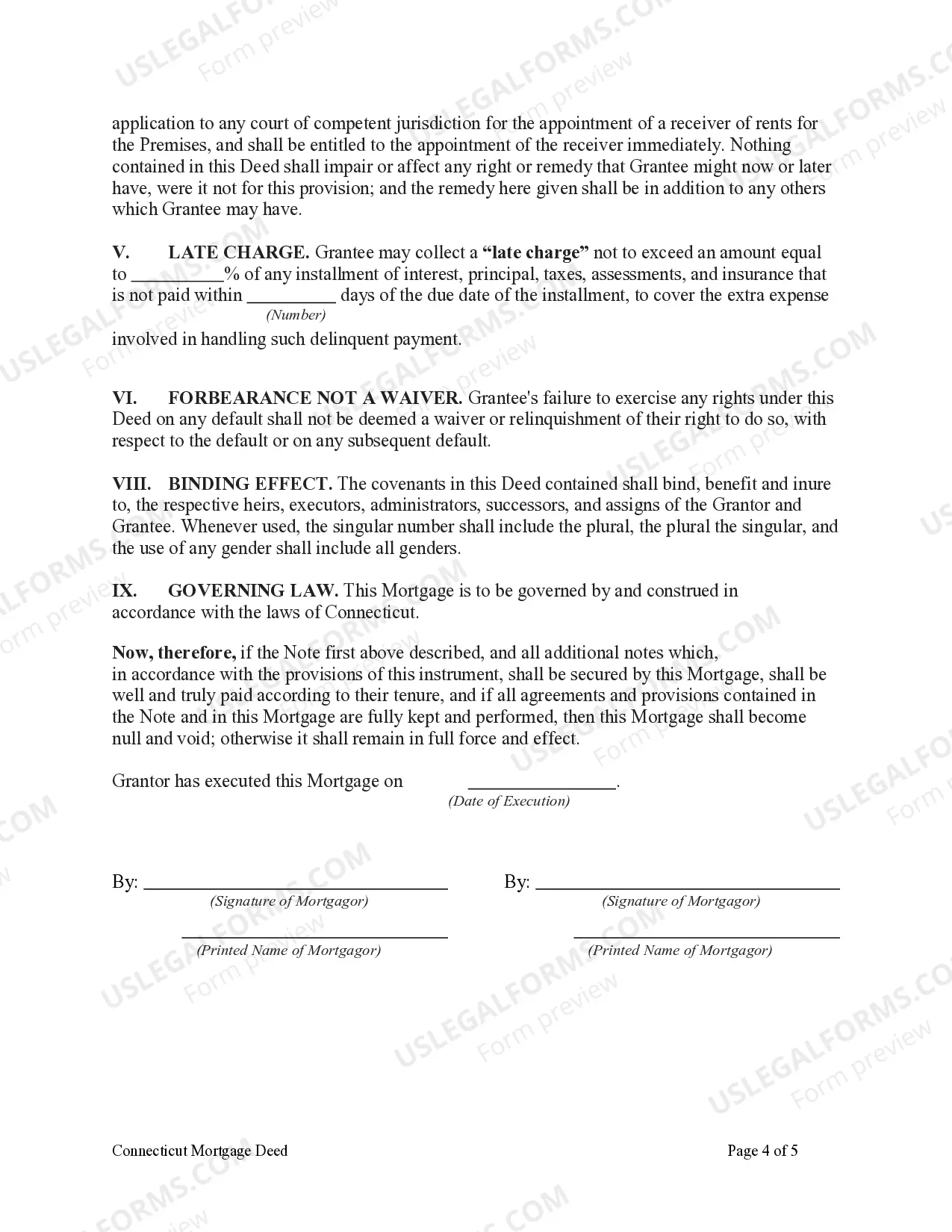

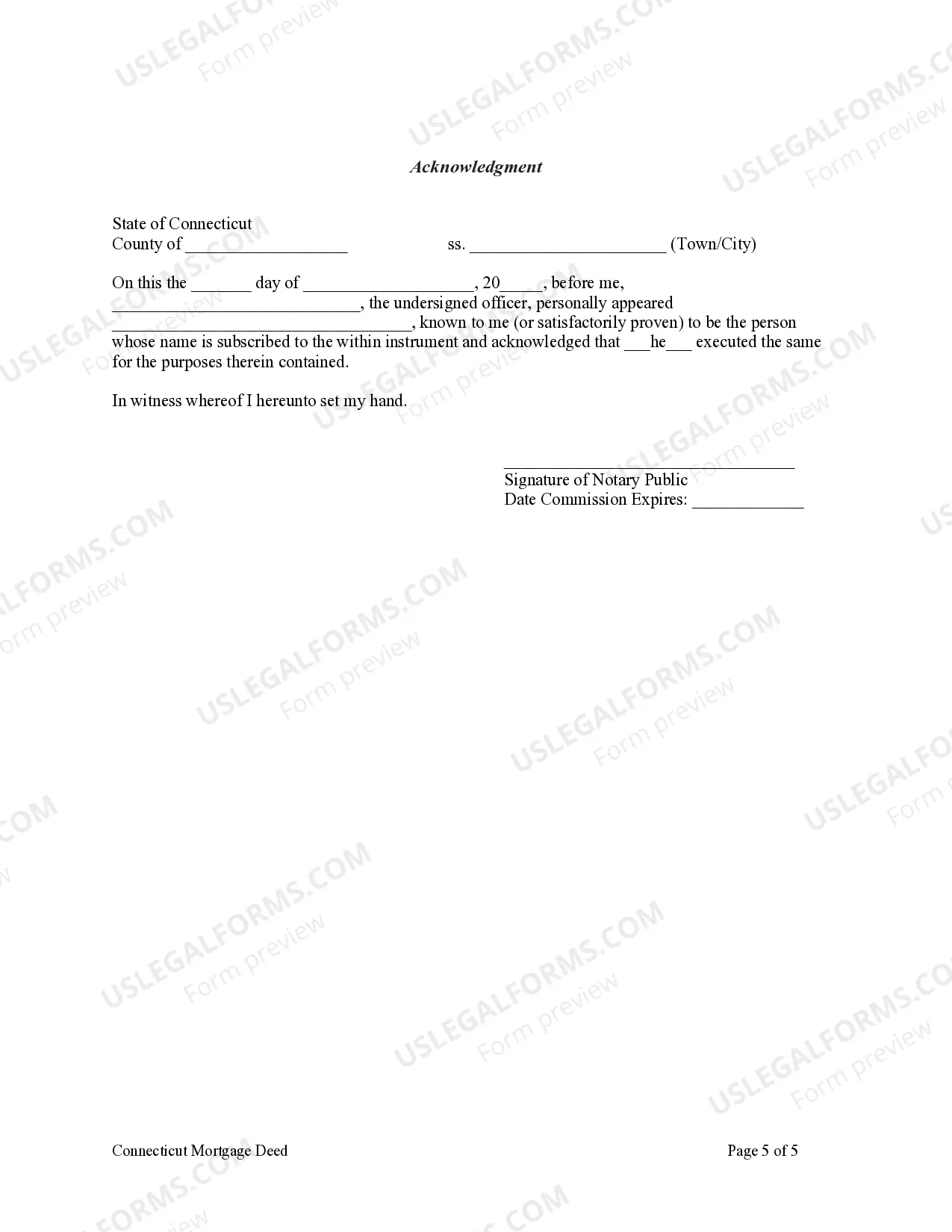

The Waterbury Connecticut Mortgage Deed is a legal document that serves as evidence of a borrower's agreement to transfer the title of real property to a lender as collateral for a loan. It establishes a lien on the property, enabling the lender to foreclose and sell the property in the event of loan default. Waterbury Connecticut Mortgage Deed serves as a binding contract between the borrower (mortgagor) and the lender (mortgagee), outlining the terms and conditions of the mortgage agreement. It typically includes information such as the names and addresses of the parties involved, details of the property being mortgaged, the loan amount, interest rates, repayment terms, and any additional provisions specific to the mortgage agreement. The Waterbury Connecticut Mortgage Deed serves as a crucial legal document in the home buying process, protecting the lender's interests and ensuring loan repayment. It also provides the borrower with necessary financing to purchase or refinance a property. There are different types of Waterbury Connecticut Mortgage Deeds that homeowners and lenders can utilize based on their specific needs: 1. Fixed-Rate Mortgage Deed: This type of mortgage deed offers a fixed interest rate throughout the loan term, providing borrowers with predictable monthly payments. 2. Adjustable-Rate Mortgage Deed: With this type of mortgage deed, the interest rate fluctuates according to prevailing market conditions, often resulting in varying monthly payments. 3. Balloon Mortgage Deed: A balloon mortgage deed requires borrowers to make small monthly payments for a fixed period, typically 5 to 7 years, after which the remaining loan balance is due in one lump sum payment. 4. Interest-Only Mortgage Deed: This mortgage deed allows borrowers to make interest-only payments for a specific period, usually between 5 and 10 years, after which regular principal and interest payments kick in. 5. Reverse Mortgage Deed: Primarily designed for senior homeowners, this mortgage deed allows individuals aged 62 or older to convert a portion of their home equity into loan proceeds without the need for monthly payments. The loan is repaid when the borrower sells the property, moves out or passes away. It's important to consult with a licensed attorney or mortgage professional to ensure a complete understanding of the specific terms and conditions outlined in a Waterbury Connecticut Mortgage Deed.

Waterbury Connecticut Mortgage Deed

Description

How to fill out Waterbury Connecticut Mortgage Deed?

Do you need a reliable and inexpensive legal forms provider to get the Waterbury Connecticut Mortgage Deed? US Legal Forms is your go-to solution.

No matter if you require a simple agreement to set rules for cohabitating with your partner or a package of documents to advance your divorce through the court, we got you covered. Our website provides more than 85,000 up-to-date legal document templates for personal and business use. All templates that we give access to aren’t generic and frameworked based on the requirements of particular state and county.

To download the form, you need to log in account, locate the needed template, and click the Download button next to it. Please remember that you can download your previously purchased document templates anytime in the My Forms tab.

Are you new to our website? No worries. You can set up an account in minutes, but before that, make sure to do the following:

- Check if the Waterbury Connecticut Mortgage Deed conforms to the laws of your state and local area.

- Read the form’s description (if provided) to learn who and what the form is good for.

- Start the search over if the template isn’t suitable for your legal situation.

Now you can register your account. Then pick the subscription option and proceed to payment. As soon as the payment is completed, download the Waterbury Connecticut Mortgage Deed in any provided format. You can get back to the website when you need and redownload the form free of charge.

Finding up-to-date legal documents has never been easier. Give US Legal Forms a go today, and forget about wasting your valuable time researching legal paperwork online once and for all.