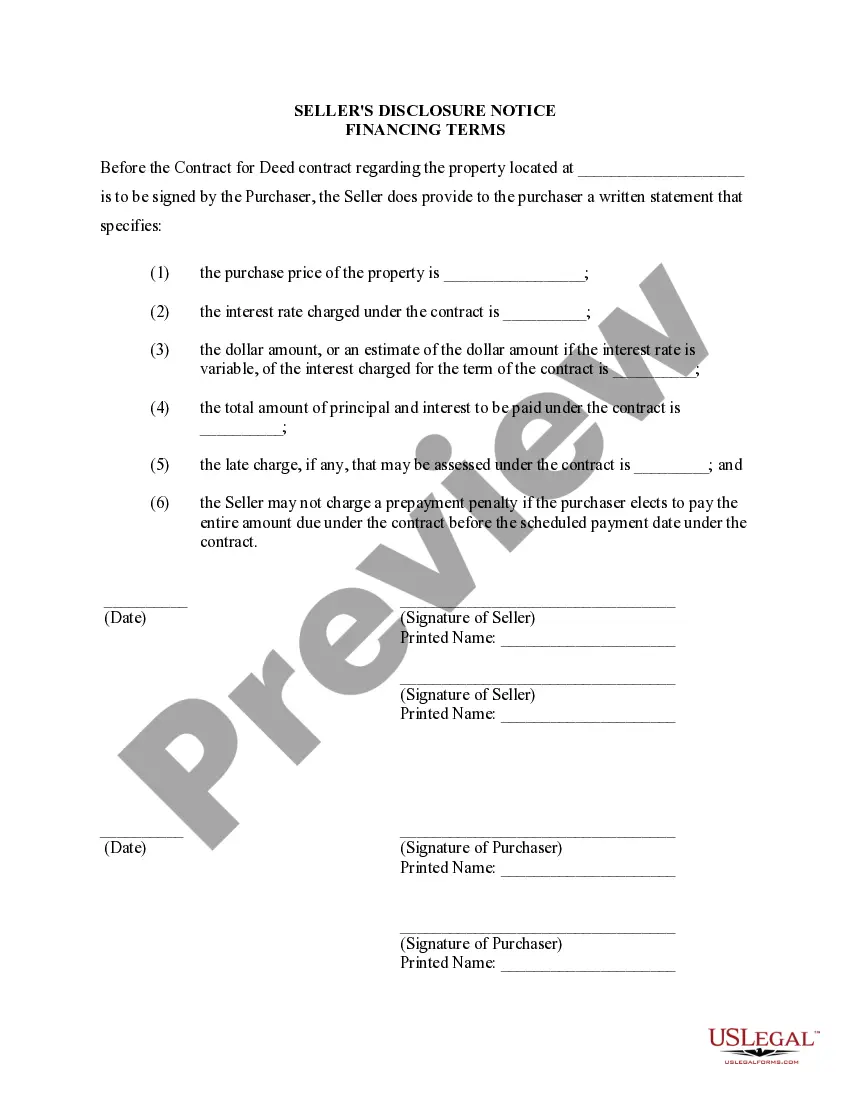

This Seller's Disclosure Notice of Financing Terms Contract for Deed serves as notice to Purchaser of the purchase price of property and how payments, interest, and late charges are set. This document should be completed by Seller of property and provided to the Purchaser at or before the signing of the contract for deed.

Port St. Lucie, located in Florida, has specific regulations and requirements for sellers to disclose financing terms when entering into a contract or agreement for deed, also known as a land contract. This disclosure ensures that potential buyers are aware of the financing arrangement and terms associated with the purchase of residential property. Here are various types of Port St. Lucie Florida Seller's Disclosures of Financing Terms for Residential Property in connection with Contract or Agreement for Deed: 1. Down Payment: The seller must disclose the amount of the down payment required for the purchase of the property. This includes specifying whether the down payment is a fixed amount or a percentage of the property's price. 2. Interest Rate: The disclosure should mention the interest rate that will be applicable to the financing terms. This interest rate may be fixed or adjustable, depending on the agreement between the buyer and seller. 3. Loan Duration: Sellers need to disclose the length of the loan term, indicating the number of years the buyer will have to repay the financing amount. This helps buyers understand the timeline for their financial commitment. 4. Payment Schedule: The disclosure should outline the payment schedule, including the frequency (monthly, quarterly, etc.) and due dates for the payments. Clear information about when the first payment is due is crucial for both parties. 5. Balloon Payment: If applicable, the seller's disclosure must specify whether there is a balloon payment involved. A balloon payment is a larger payment due at the end of the loan term, which can significantly affect the buyer's finances. 6. Default and Foreclosure Terms: The disclosure should outline the consequences of defaulting on payments and the corresponding actions that the seller may take, such as initiating foreclosure proceedings. 7. Prepayment Penalty: Any prepayment penalty clauses should be explicitly stated in the disclosure. This clause outlines additional charges that may apply if the buyer wants to pay off the loan before the agreed-upon time. 8. Escrow Account: If an escrow account is required, the disclosure should explain its purpose and how funds will be managed for items such as property taxes and insurance. 9. Seller Financing Conditions: In some cases, the disclosure may include specific conditions set by the seller for offering financing options. These conditions generally refer to creditworthiness requirements or other pertinent qualifications. By ensuring that the seller's disclosure of financing terms for residential property in Port St. Lucie follows these guidelines, both buyers and sellers can have a transparent and informed understanding of the financing arrangement. It is essential for buyers to review and understand the disclosure thoroughly and seek legal or financial advice if needed before entering into a contract or agreement for deed.