A junior or second deed of trust is a deed of trust which is subordinate to existing liens on the securing property, usually because the junior deed of trust was made, executed and recorded after one or more earlier deeds of trust or other encumbrances.

Junior deeds of trust can be created in several ways. For example, such deeds of trust often arise as the result of a sale of real property, either when a new loan in the full amount of the purchase price cannot be obtained or when an existing loan on the securing property is assumed. In this situation, a junior deed of trust is given to secure the portion of the purchase price which exceeds the balance of the new or existing loan.

Additionally, a junior deed of trust may be created where an existing lienholder, typically a seller, subordinates to another secured debt, usually a construction loan. Finally, junior deeds of trust may arise where the owner of real property obtains a loan secured by the property after its purchase.

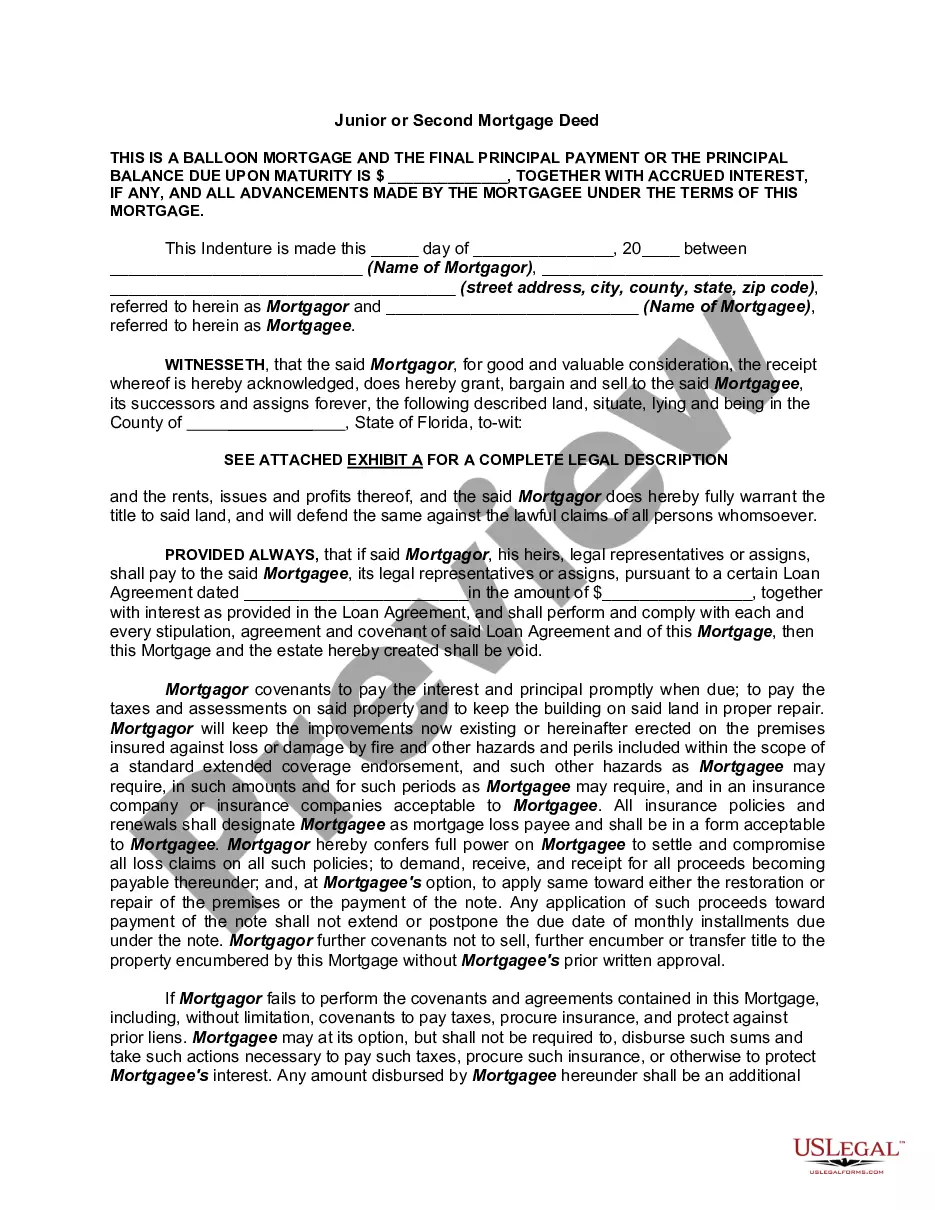

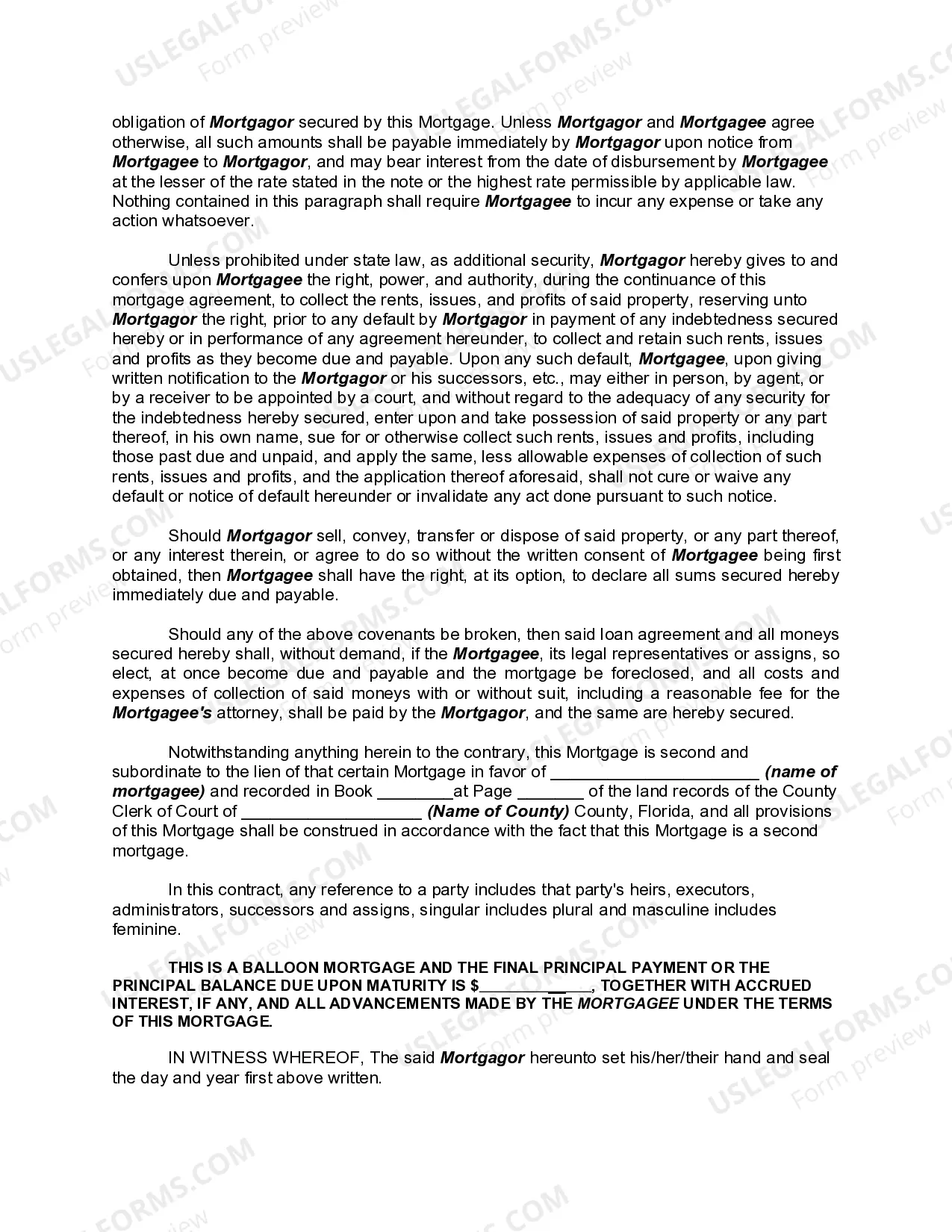

Lakeland Florida Junior or Second Mortgage Deed is a legal document used in real estate transactions that involves borrowing money against a property with an existing mortgage. This type of mortgage deed is commonly employed when homeowners need additional funds for various purposes such as home improvements, debt consolidation, or financing education. The primary purpose of a junior or second mortgage deed is to allow homeowners to access the equity they have built in their property without necessarily refinancing their existing mortgage. Unlike a primary mortgage, which takes precedence over all other liens on the property, a junior or second mortgage deed ranks lower in priority, hence the term "junior." In the event of a foreclosure, the primary mortgage holder is entitled to receive repayment first, followed by the junior mortgage holder. There are two main types of Lakeland Florida junior or second mortgage deeds: 1. Home Equity Line of Credit (HELOT): This type of mortgage deed provides homeowners with a line of credit that they can draw from as needed. The available credit is determined based on the homeowner's equity in the property. Interest rates on Helots are typically variable and may have a draw period during which the homeowner can borrow from the line of credit. Repayment terms can vary, but often include a combination of interest-only payments during the draw period, followed by principal and interest payments during the repayment period. 2. Fixed Rate Second Mortgage: Unlike a HELOT, a fixed rate second mortgage provides homeowners with a lump sum of money upfront. The interest rate on this type of mortgage deed is fixed and the repayment terms are generally structured over a set period of time with equal monthly payments. This makes it easier for homeowners to budget since the payments remain consistent throughout the loan term. When considering a junior or second mortgage deed in Lakeland, Florida, it is essential for homeowners to carefully evaluate the terms, interest rates, fees, and repayment options offered by different lenders. Seeking advice from a qualified mortgage professional and conducting thorough research is crucial to make informed decisions and select the most suitable option for their financial needs. By understanding and considering the nuances associated with Lakeland Florida junior or second mortgage deeds, homeowners can leverage their property's equity strategically and responsibly to achieve their financial goals while maintaining ownership of their home.Lakeland Florida Junior or Second Mortgage Deed is a legal document used in real estate transactions that involves borrowing money against a property with an existing mortgage. This type of mortgage deed is commonly employed when homeowners need additional funds for various purposes such as home improvements, debt consolidation, or financing education. The primary purpose of a junior or second mortgage deed is to allow homeowners to access the equity they have built in their property without necessarily refinancing their existing mortgage. Unlike a primary mortgage, which takes precedence over all other liens on the property, a junior or second mortgage deed ranks lower in priority, hence the term "junior." In the event of a foreclosure, the primary mortgage holder is entitled to receive repayment first, followed by the junior mortgage holder. There are two main types of Lakeland Florida junior or second mortgage deeds: 1. Home Equity Line of Credit (HELOT): This type of mortgage deed provides homeowners with a line of credit that they can draw from as needed. The available credit is determined based on the homeowner's equity in the property. Interest rates on Helots are typically variable and may have a draw period during which the homeowner can borrow from the line of credit. Repayment terms can vary, but often include a combination of interest-only payments during the draw period, followed by principal and interest payments during the repayment period. 2. Fixed Rate Second Mortgage: Unlike a HELOT, a fixed rate second mortgage provides homeowners with a lump sum of money upfront. The interest rate on this type of mortgage deed is fixed and the repayment terms are generally structured over a set period of time with equal monthly payments. This makes it easier for homeowners to budget since the payments remain consistent throughout the loan term. When considering a junior or second mortgage deed in Lakeland, Florida, it is essential for homeowners to carefully evaluate the terms, interest rates, fees, and repayment options offered by different lenders. Seeking advice from a qualified mortgage professional and conducting thorough research is crucial to make informed decisions and select the most suitable option for their financial needs. By understanding and considering the nuances associated with Lakeland Florida junior or second mortgage deeds, homeowners can leverage their property's equity strategically and responsibly to achieve their financial goals while maintaining ownership of their home.