A junior or second deed of trust is a deed of trust which is subordinate to existing liens on the securing property, usually because the junior deed of trust was made, executed and recorded after one or more earlier deeds of trust or other encumbrances.

Junior deeds of trust can be created in several ways. For example, such deeds of trust often arise as the result of a sale of real property, either when a new loan in the full amount of the purchase price cannot be obtained or when an existing loan on the securing property is assumed. In this situation, a junior deed of trust is given to secure the portion of the purchase price which exceeds the balance of the new or existing loan.

Additionally, a junior deed of trust may be created where an existing lienholder, typically a seller, subordinates to another secured debt, usually a construction loan. Finally, junior deeds of trust may arise where the owner of real property obtains a loan secured by the property after its purchase.

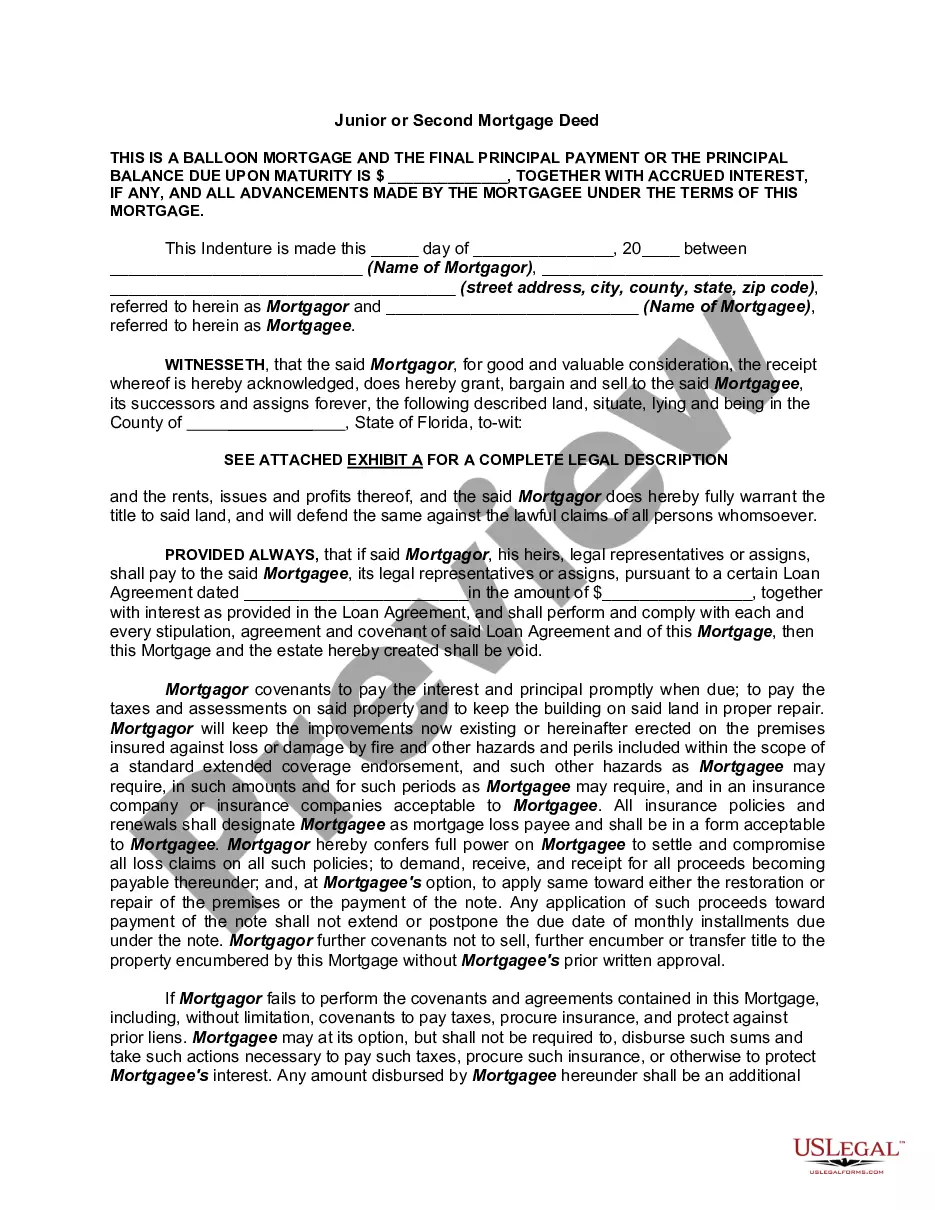

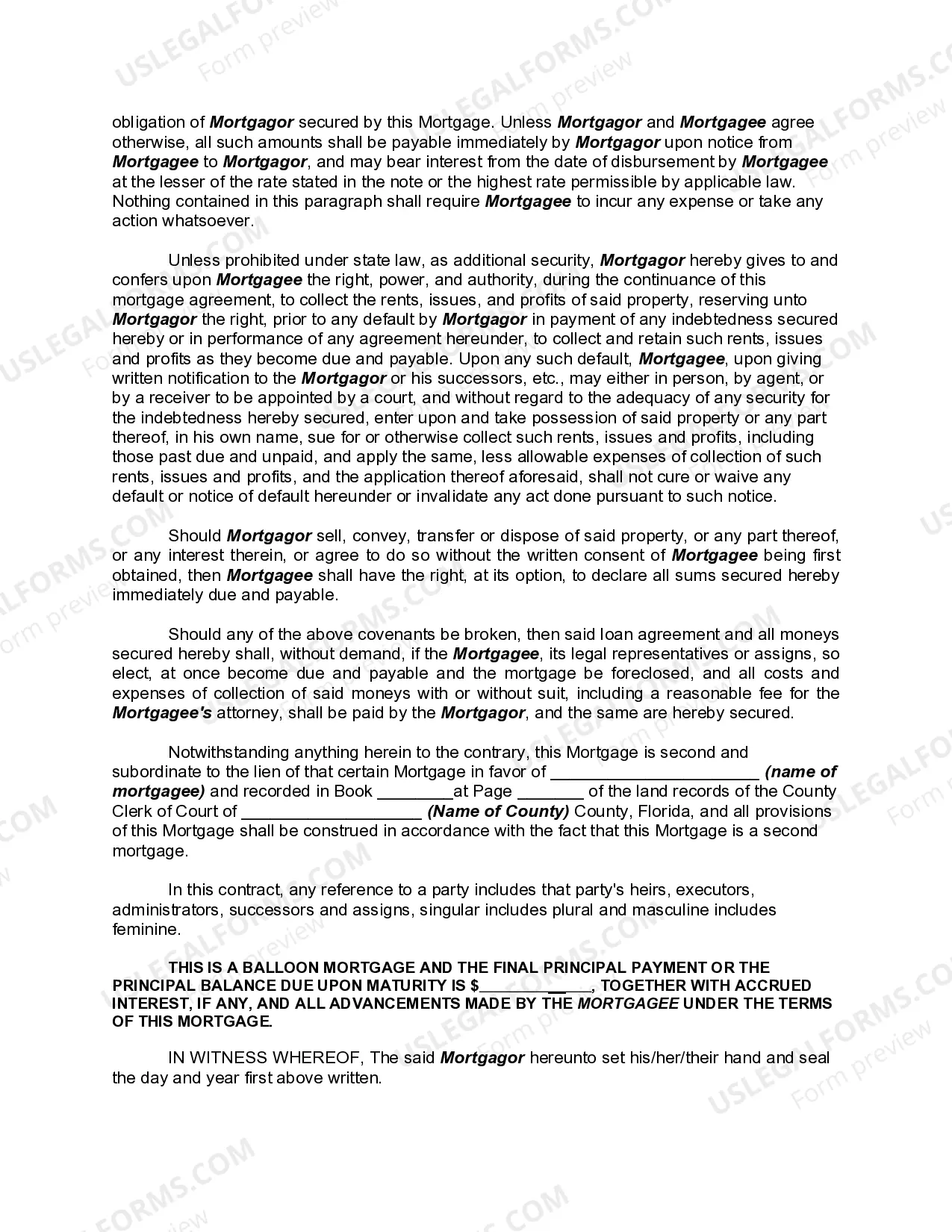

Pembroke Pines Florida Junior or Second Mortgage Deed refers to a legal document that allows borrowers to secure an additional loan against their property, in addition to their current or primary mortgage. This type of mortgage deed is commonly used by homeowners in Pembroke Pines, Florida, to access extra funds for various purposes such as home improvements, debt consolidation, or unexpected expenses. A second mortgage deed acts as a subordinate lien to the first mortgage and is recorded after the initial mortgage deed with the county clerk's office. This means that in the event of foreclosure, the primary mortgage lender gets priority in recovering their loan before the second mortgage lender. Different types of Pembroke Pines Florida Junior or Second Mortgage Deeds may include: 1. Home Equity Loan: Homeowners can utilize the equity they have accumulated in their property to obtain a fixed loan amount. The interest rates and terms on home equity loans are typically predetermined and come with monthly repayment plans. 2. Home Equity Line of Credit (HELOT): This type of second mortgage allows borrowers to access a line of credit, which they can draw upon as needed. With a HELOT, homeowners have the flexibility to borrow funds up to a predetermined credit limit and make interest-only payments during the initial draw period. 3. Piggyback Loan: Also known as an 80-10-10 or 80-15-5 loan, this type of mortgage allows borrowers to avoid paying private mortgage insurance (PMI) by combining a first mortgage for 80% of the home's value, a second mortgage for 10% or 15%, and a down payment for the remaining amount. 4. Reverse Mortgage: Available to senior homeowners aged 62 and older, a reverse mortgage allows them to convert a portion of their home equity into cash without selling the property. The loan is repaid when the homeowner sells the property, moves out permanently, or passes away. 5. Bridge Loan: This temporary financing option assists homeowners who plan to sell their current property and purchase a new one. A bridge loan bridges the financial gap between the sale of the old home and the purchase of the new one, providing the necessary funds for the down payment or closing costs. In Pembroke Pines, Florida, homeowners have various options when it comes to obtaining a second mortgage deed. However, it is crucial to carefully consider the terms, interest rates, and repayment plans associated with each type of loan. Consulting with a reputable mortgage lender or financial advisor can ensure borrowers make informed decisions based on their specific needs and financial objectives.Pembroke Pines Florida Junior or Second Mortgage Deed refers to a legal document that allows borrowers to secure an additional loan against their property, in addition to their current or primary mortgage. This type of mortgage deed is commonly used by homeowners in Pembroke Pines, Florida, to access extra funds for various purposes such as home improvements, debt consolidation, or unexpected expenses. A second mortgage deed acts as a subordinate lien to the first mortgage and is recorded after the initial mortgage deed with the county clerk's office. This means that in the event of foreclosure, the primary mortgage lender gets priority in recovering their loan before the second mortgage lender. Different types of Pembroke Pines Florida Junior or Second Mortgage Deeds may include: 1. Home Equity Loan: Homeowners can utilize the equity they have accumulated in their property to obtain a fixed loan amount. The interest rates and terms on home equity loans are typically predetermined and come with monthly repayment plans. 2. Home Equity Line of Credit (HELOT): This type of second mortgage allows borrowers to access a line of credit, which they can draw upon as needed. With a HELOT, homeowners have the flexibility to borrow funds up to a predetermined credit limit and make interest-only payments during the initial draw period. 3. Piggyback Loan: Also known as an 80-10-10 or 80-15-5 loan, this type of mortgage allows borrowers to avoid paying private mortgage insurance (PMI) by combining a first mortgage for 80% of the home's value, a second mortgage for 10% or 15%, and a down payment for the remaining amount. 4. Reverse Mortgage: Available to senior homeowners aged 62 and older, a reverse mortgage allows them to convert a portion of their home equity into cash without selling the property. The loan is repaid when the homeowner sells the property, moves out permanently, or passes away. 5. Bridge Loan: This temporary financing option assists homeowners who plan to sell their current property and purchase a new one. A bridge loan bridges the financial gap between the sale of the old home and the purchase of the new one, providing the necessary funds for the down payment or closing costs. In Pembroke Pines, Florida, homeowners have various options when it comes to obtaining a second mortgage deed. However, it is crucial to carefully consider the terms, interest rates, and repayment plans associated with each type of loan. Consulting with a reputable mortgage lender or financial advisor can ensure borrowers make informed decisions based on their specific needs and financial objectives.