A junior or second deed of trust is a deed of trust which is subordinate to existing liens on the securing property, usually because the junior deed of trust was made, executed and recorded after one or more earlier deeds of trust or other encumbrances.

Junior deeds of trust can be created in several ways. For example, such deeds of trust often arise as the result of a sale of real property, either when a new loan in the full amount of the purchase price cannot be obtained or when an existing loan on the securing property is assumed. In this situation, a junior deed of trust is given to secure the portion of the purchase price which exceeds the balance of the new or existing loan.

Additionally, a junior deed of trust may be created where an existing lienholder, typically a seller, subordinates to another secured debt, usually a construction loan. Finally, junior deeds of trust may arise where the owner of real property obtains a loan secured by the property after its purchase.

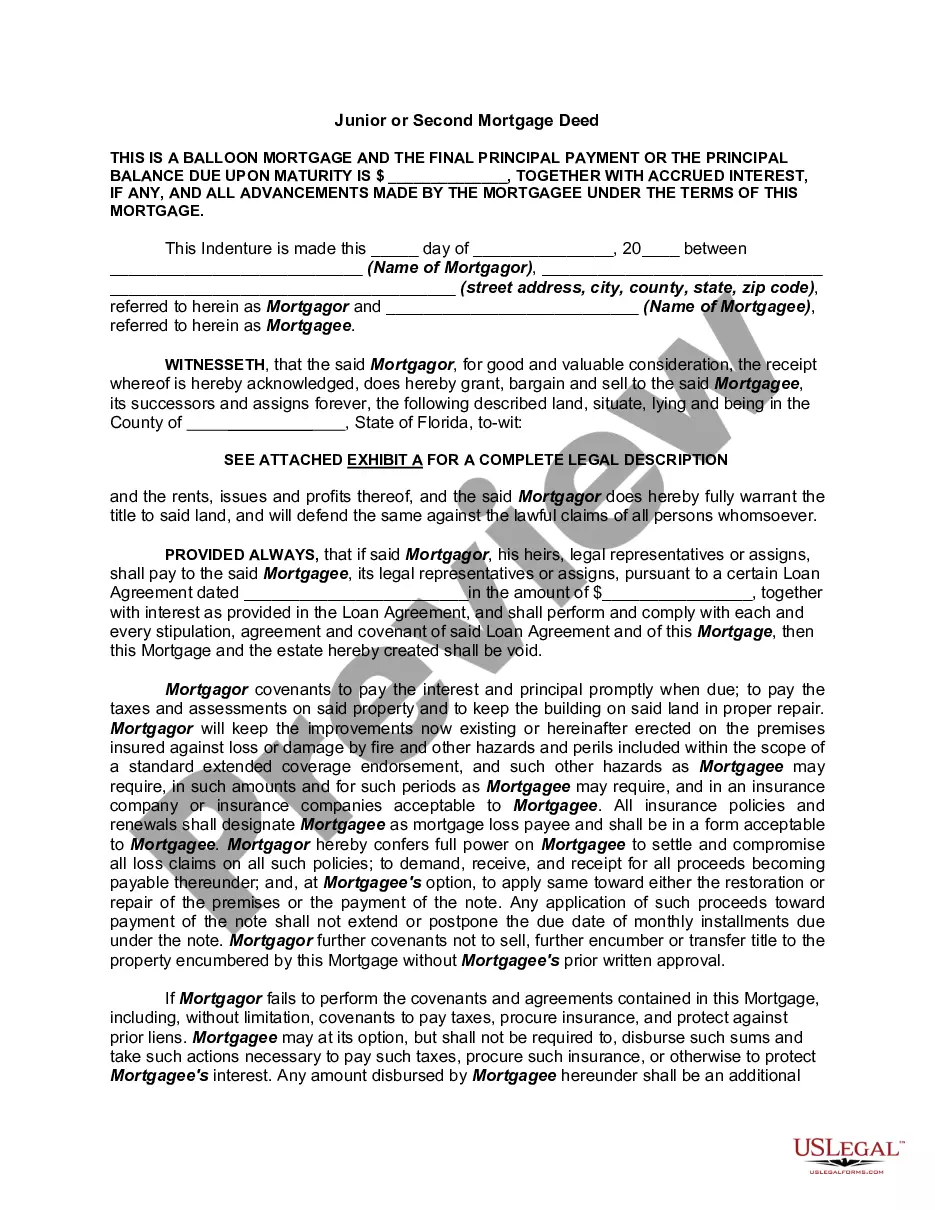

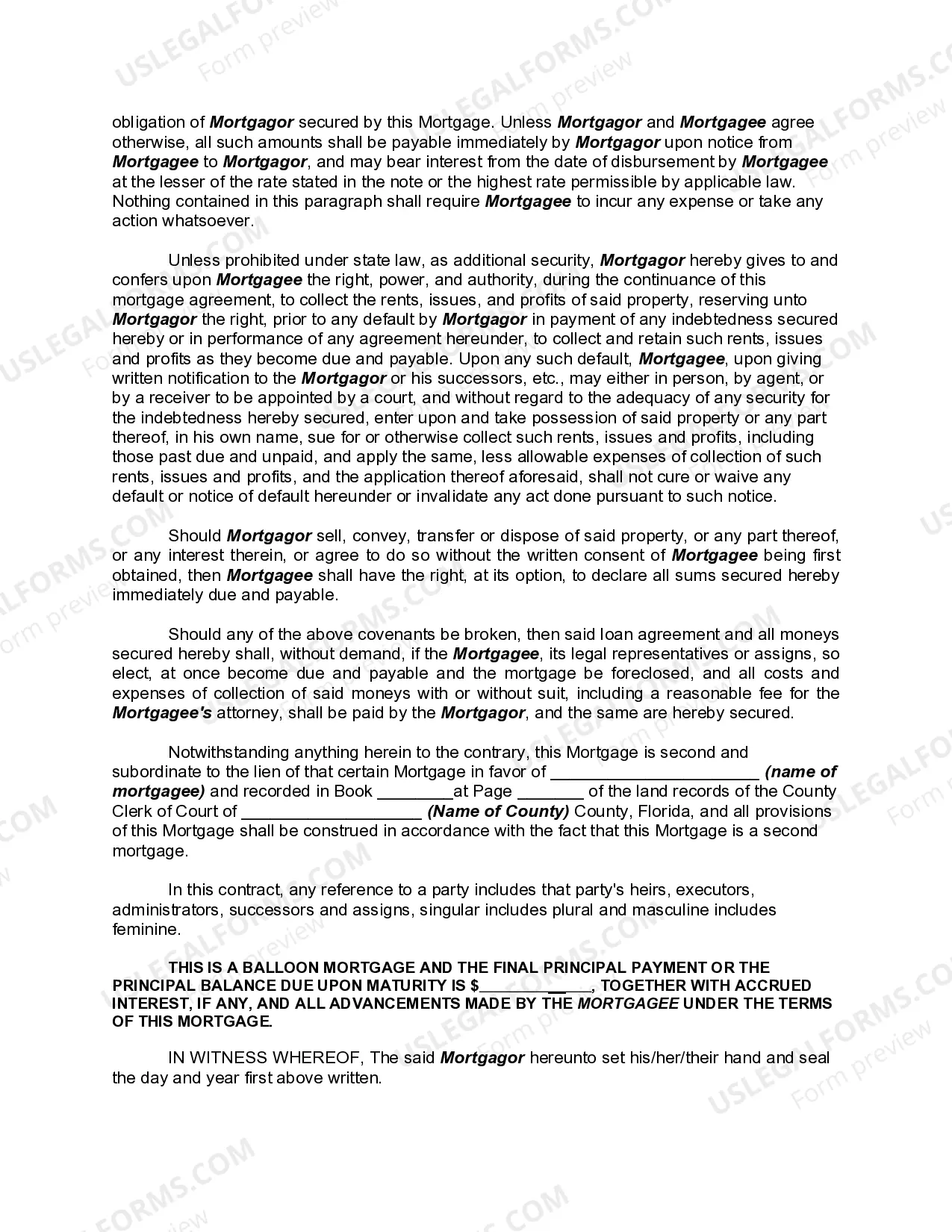

A West Palm Beach Florida Junior Mortgage Deed is a legal document that grants a lender with a secondary lien on a property located in West Palm Beach, Florida. This type of mortgage deed is obtained after the primary or first mortgage has been issued. It is often used for a variety of purposes such as home improvements, debt consolidation, or funding educational expenses. Keywords: West Palm Beach Florida, junior mortgage deed, second mortgage, property, lender, lien, legal document, primary, first mortgage, home improvements, debt consolidation, educational expenses. There are different types of West Palm Beach Florida Junior or Second Mortgage Deeds, each catering to specific needs and circumstances. Some notable variations include: 1. Fixed-Rate Second Mortgage: This type of mortgage deed involves a fixed interest rate throughout the loan term, ensuring predictable monthly payments and providing stability for borrowers. 2. Adjustable-Rate Second Mortgage: Unlike a fixed-rate mortgage, an adjustable-rate second mortgage has an interest rate that is subject to change periodically. This option may be appealing to borrowers who expect their financial situation to improve in the future. 3. Home Equity Line of Credit (HELOT): A HELOT allows homeowners to borrow against the equity they have built in their property. It establishes a line of credit that can be accessed by homeowners as needed, making it an ideal choice for ongoing expenses or projects. 4. Combined Loan-to-Value (CTV) Second Mortgage: This type of mortgage deed lets homeowners borrow against the equity in their property, taking into account the outstanding balance of their primary mortgage as well. It allows borrowers to exceed the value of their property, up to a certain limit. 5. Standalone Second Mortgage: This mortgage option involves obtaining a completely separate loan, distinct from the primary mortgage, and is commonly used when homeowners want to avoid changing the terms of their existing primary mortgage. Irrespective of the type, West Palm Beach Florida Junior or Second Mortgage Deeds require a thorough understanding of the terms, repayment schedules, and potential risks involved. It is crucial for borrowers to carefully evaluate their financial situation and seek professional advice to determine whether a junior or second mortgage is the right choice for their specific needs.A West Palm Beach Florida Junior Mortgage Deed is a legal document that grants a lender with a secondary lien on a property located in West Palm Beach, Florida. This type of mortgage deed is obtained after the primary or first mortgage has been issued. It is often used for a variety of purposes such as home improvements, debt consolidation, or funding educational expenses. Keywords: West Palm Beach Florida, junior mortgage deed, second mortgage, property, lender, lien, legal document, primary, first mortgage, home improvements, debt consolidation, educational expenses. There are different types of West Palm Beach Florida Junior or Second Mortgage Deeds, each catering to specific needs and circumstances. Some notable variations include: 1. Fixed-Rate Second Mortgage: This type of mortgage deed involves a fixed interest rate throughout the loan term, ensuring predictable monthly payments and providing stability for borrowers. 2. Adjustable-Rate Second Mortgage: Unlike a fixed-rate mortgage, an adjustable-rate second mortgage has an interest rate that is subject to change periodically. This option may be appealing to borrowers who expect their financial situation to improve in the future. 3. Home Equity Line of Credit (HELOT): A HELOT allows homeowners to borrow against the equity they have built in their property. It establishes a line of credit that can be accessed by homeowners as needed, making it an ideal choice for ongoing expenses or projects. 4. Combined Loan-to-Value (CTV) Second Mortgage: This type of mortgage deed lets homeowners borrow against the equity in their property, taking into account the outstanding balance of their primary mortgage as well. It allows borrowers to exceed the value of their property, up to a certain limit. 5. Standalone Second Mortgage: This mortgage option involves obtaining a completely separate loan, distinct from the primary mortgage, and is commonly used when homeowners want to avoid changing the terms of their existing primary mortgage. Irrespective of the type, West Palm Beach Florida Junior or Second Mortgage Deeds require a thorough understanding of the terms, repayment schedules, and potential risks involved. It is crucial for borrowers to carefully evaluate their financial situation and seek professional advice to determine whether a junior or second mortgage is the right choice for their specific needs.