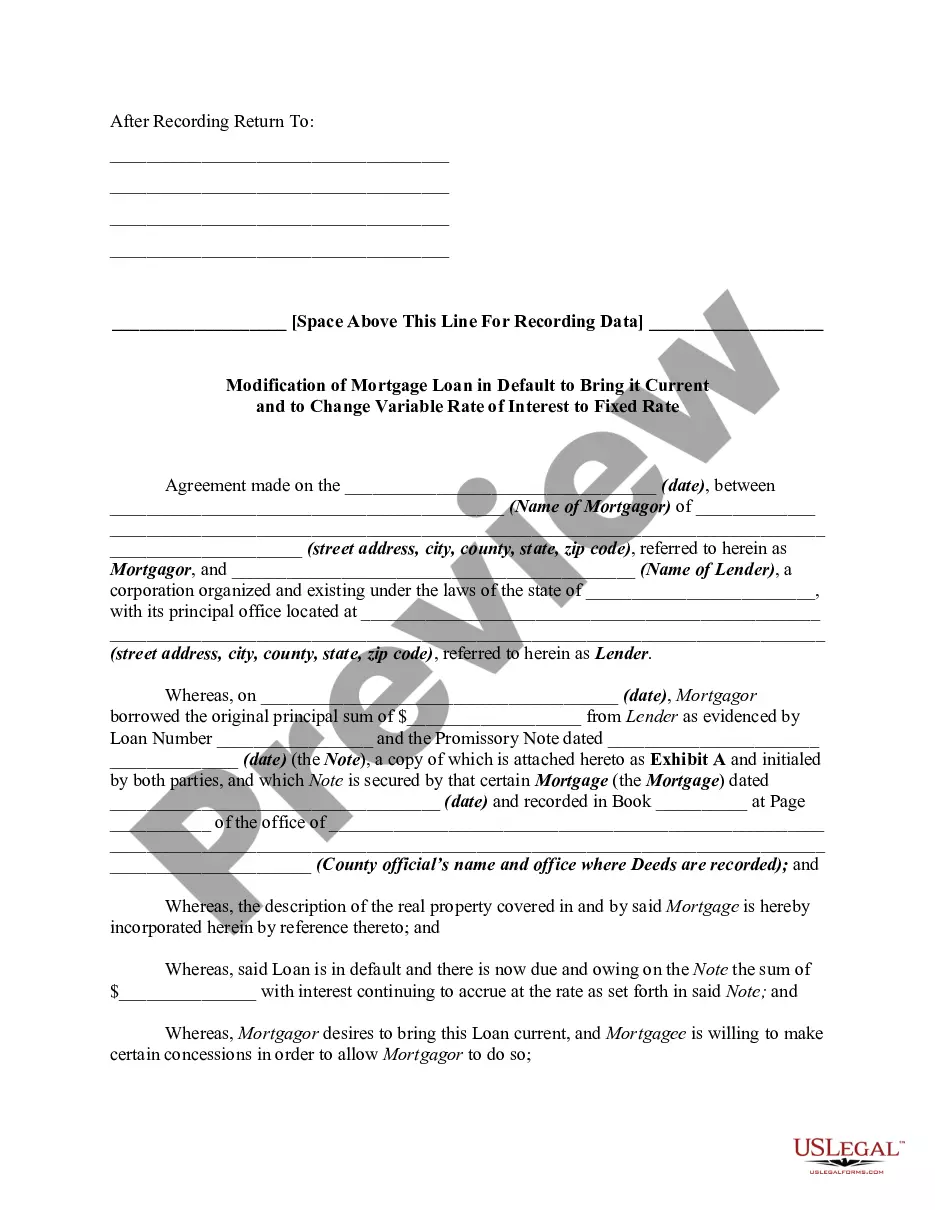

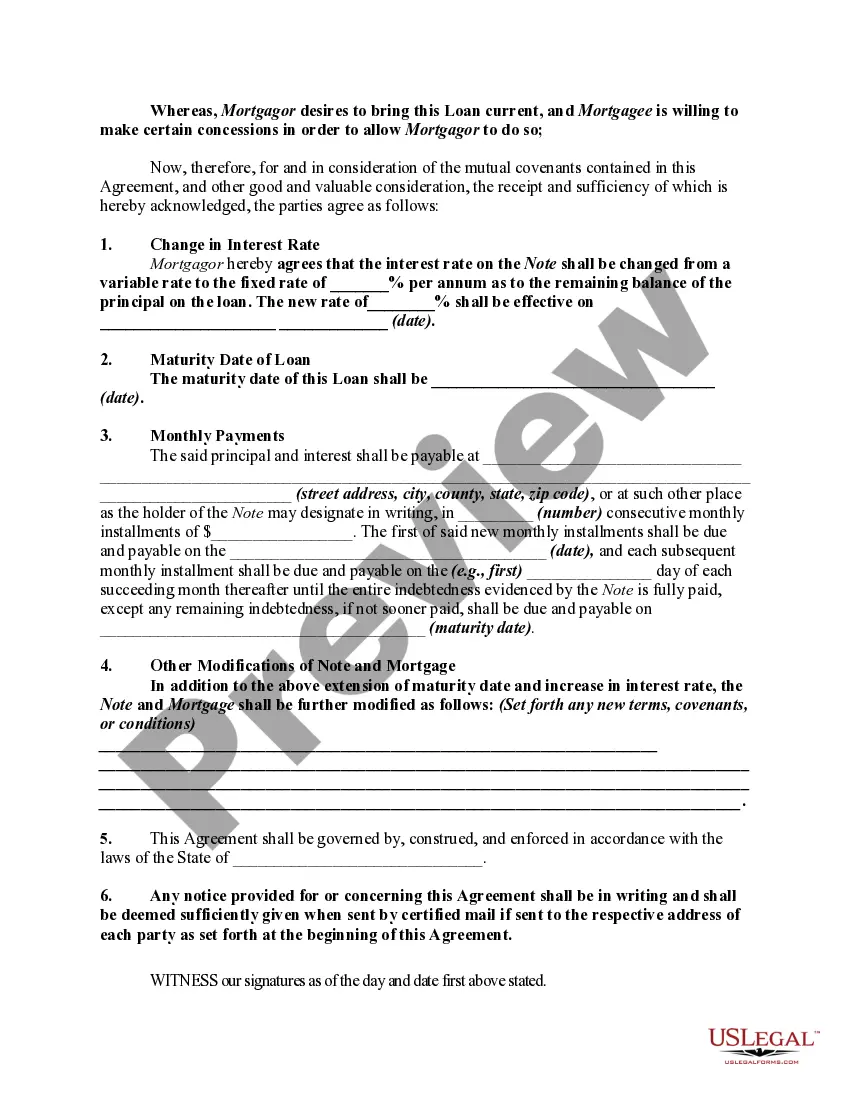

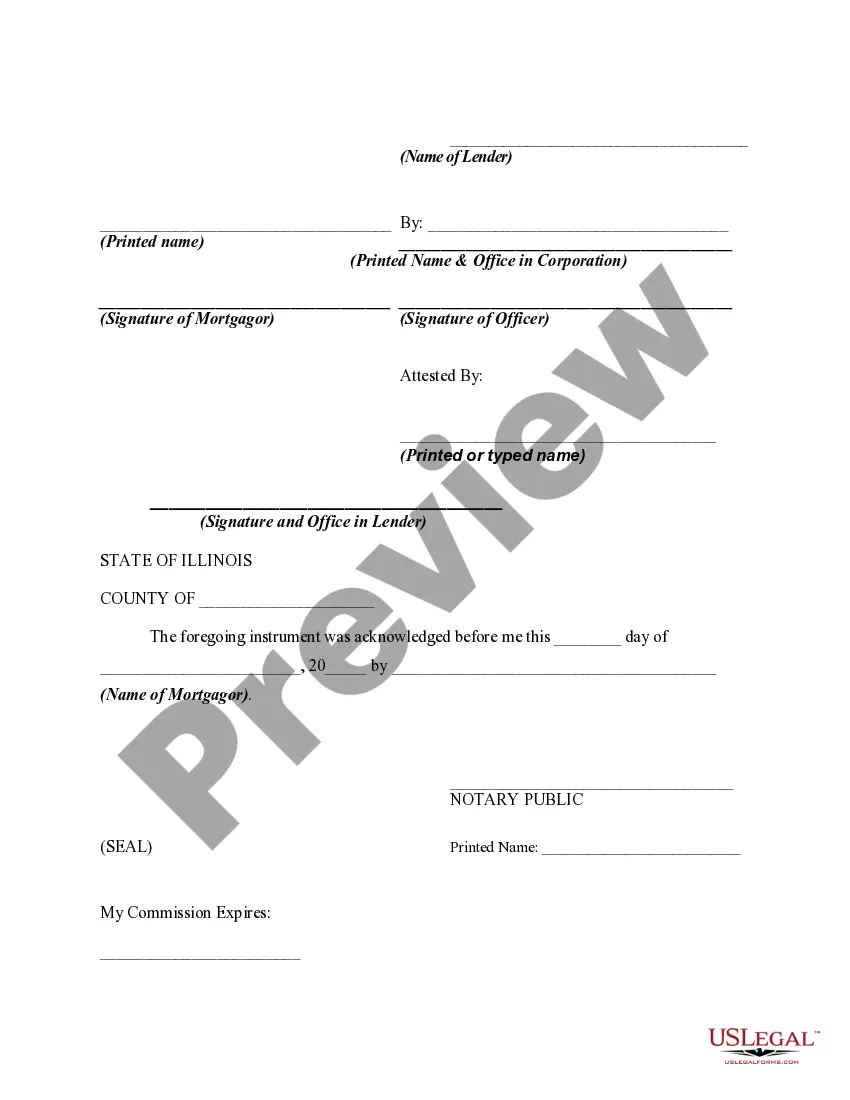

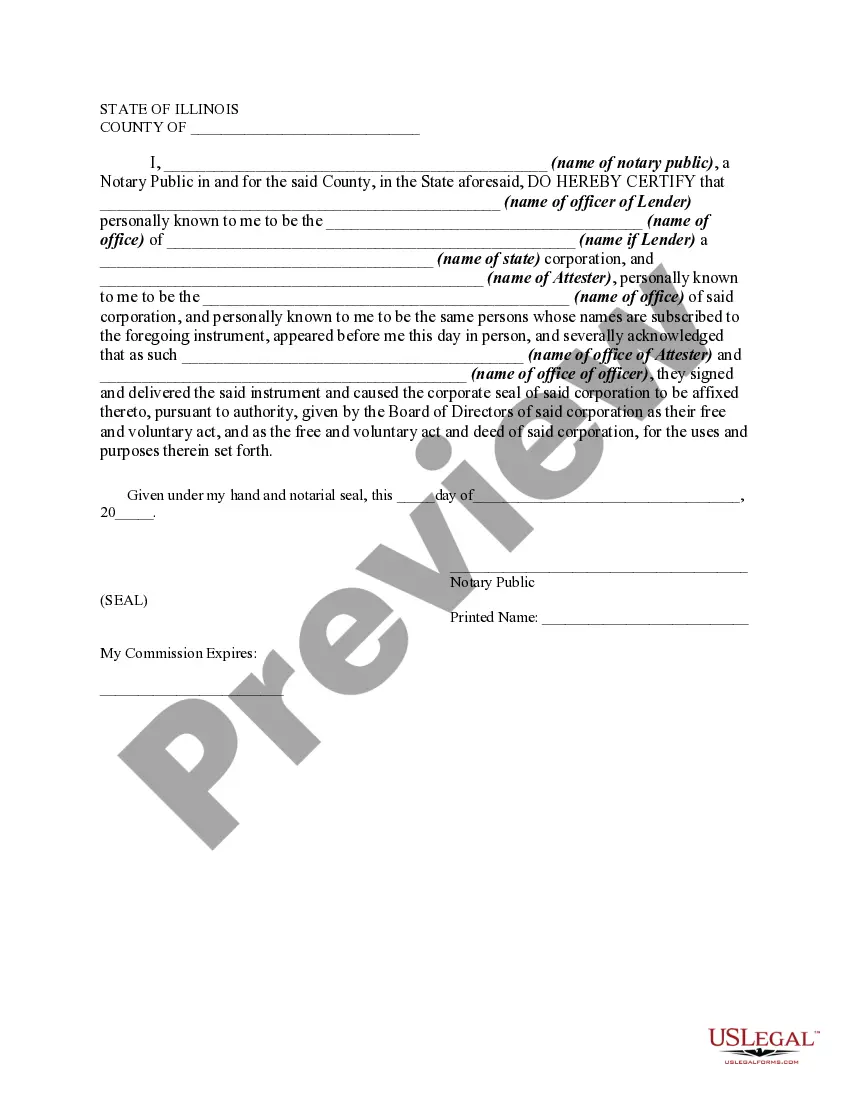

An agreement modifying a loan agreement and mortgage should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original mortgage was recorded. Such a modification is contractual in nature and should be supported by consideration.

A Chicago Illinois Modification of Mortgage Loan in Default to Bring it Current and to Change Variable Rate of Interest to Fixed Rate refers to a process in which the terms of a mortgage loan that is in default are modified in order to bring it up to date and alter the interest rate from a variable rate to a fixed rate. This modification is typically sought by homeowners who are facing financial difficulties and have fallen behind on their mortgage payments. There are several types of Chicago Illinois Modification of Mortgage Loan in Default to Bring it Current and to Change Variable Rate of Interest to Fixed Rate, including: 1. Loan Modification: This type of modification involves adjusting the terms of the mortgage loan to make it more affordable for the borrower. This can include reducing the interest rate, extending the loan term, or even reducing the principal balance owed. 2. Reinstatement: In this type of modification, the borrower pays the past-due amount on the mortgage loan, along with any associated fees, to bring the loan current. The interest rate may also be changed from a variable rate to a fixed rate during this process. 3. Forbearance Agreement: This modification allows the borrower to temporarily suspend or reduce their mortgage payments for a specified period of time. At the end of the forbearance period, the borrower may be required to make a lump sum payment or higher monthly payments to catch up on the past-due amount. 4. Refinance: In some cases, borrowers may choose to refinance their mortgage loan in order to bring it current and change the interest rate to a fixed one. Refinancing involves taking out a new mortgage loan with updated terms, paying off the original loan in the process. When applying for a Chicago Illinois Modification of Mortgage Loan in Default to Bring it Current and to Change Variable Rate of Interest to Fixed Rate, it is important to provide accurate and up-to-date financial documentation, including proof of income, expenses, and any extenuating circumstances that have led to the default. It is also crucial to work closely with the mortgage lender or a qualified housing counselor to navigate the modification process and negotiate favorable terms.