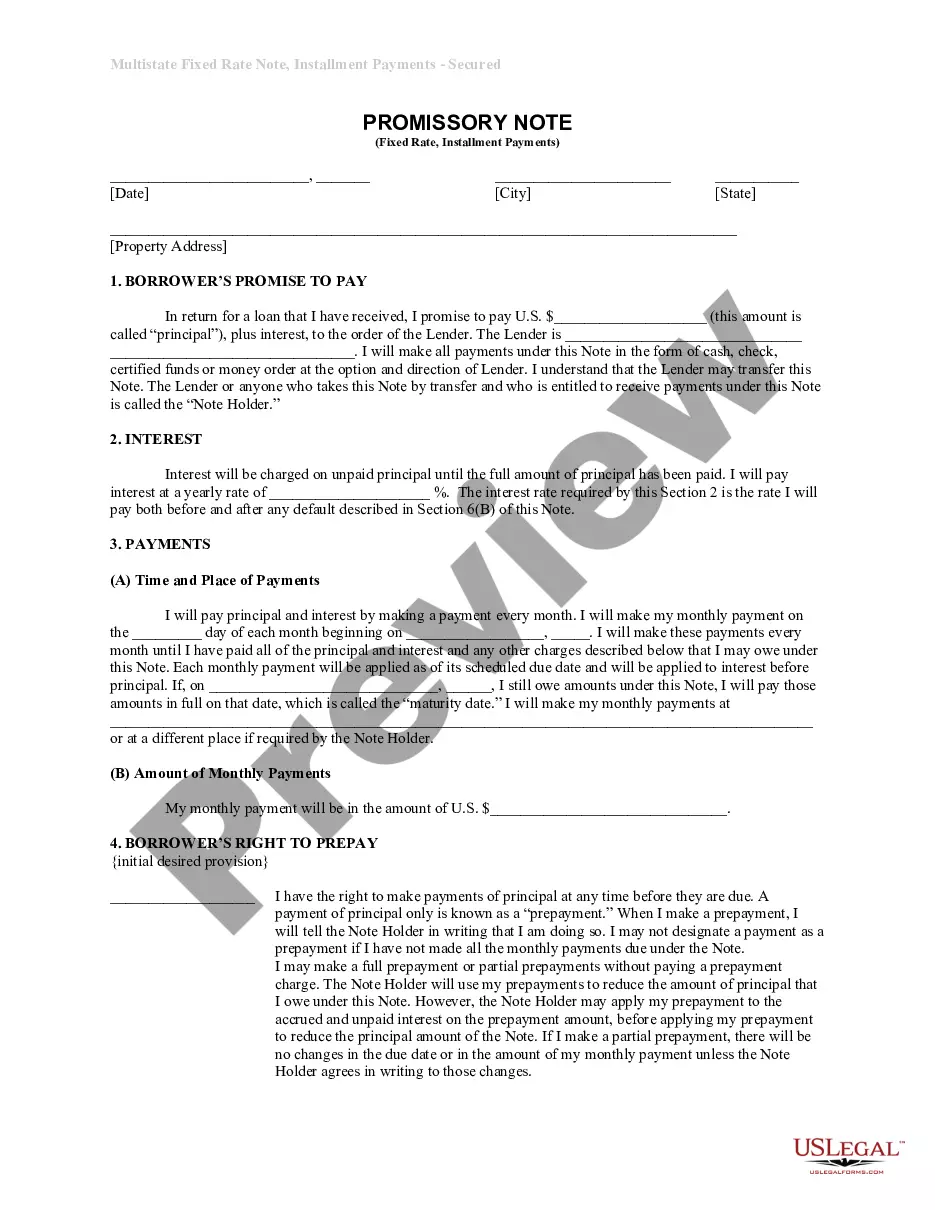

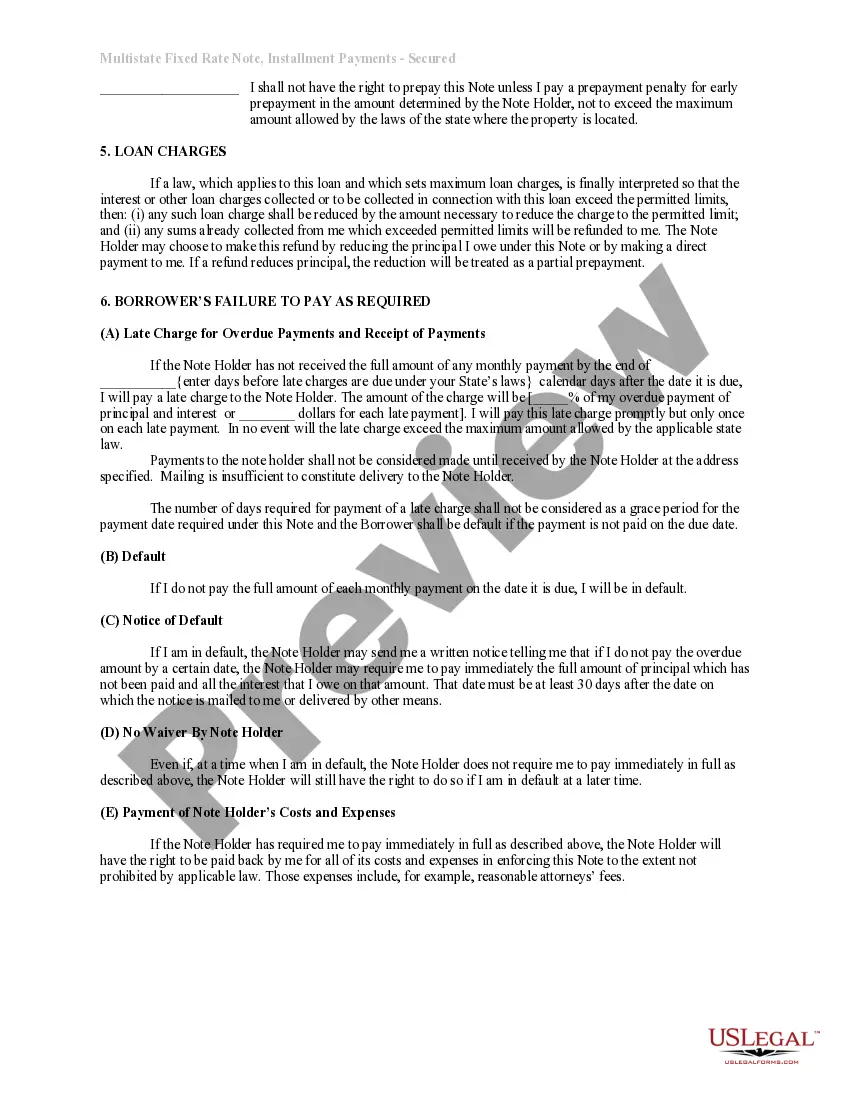

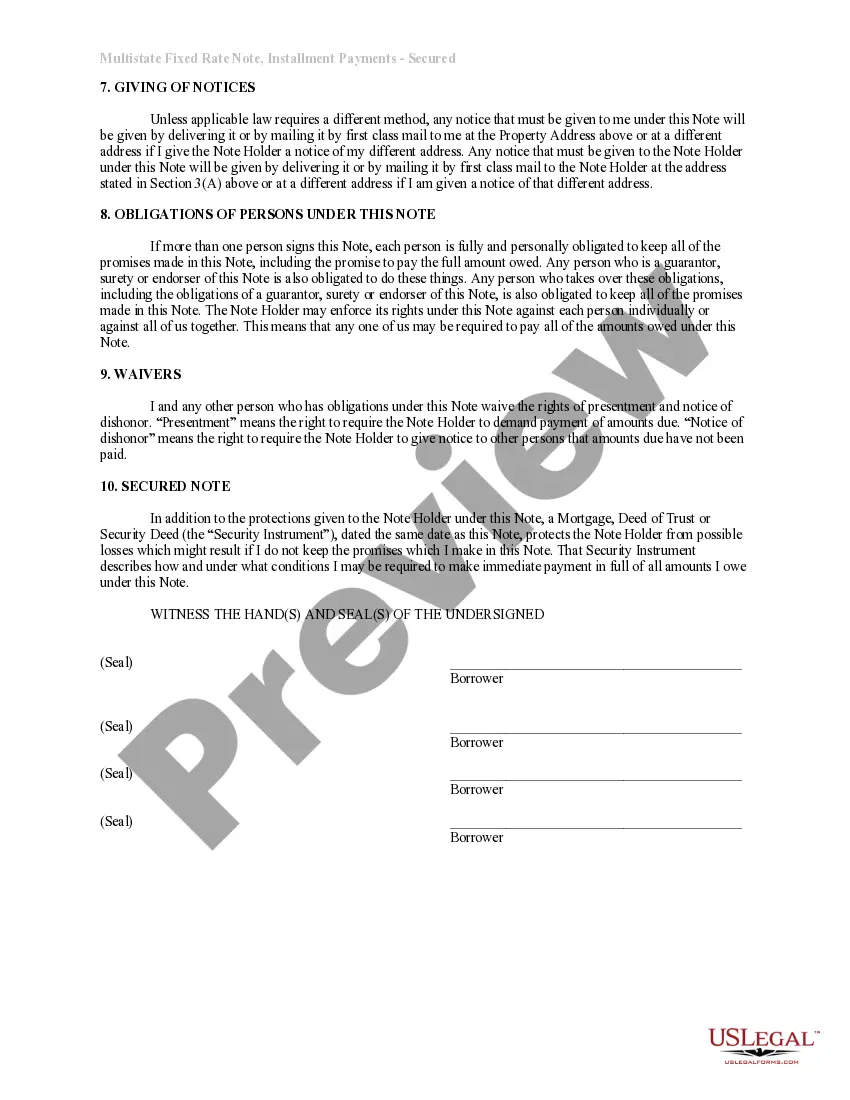

Topeka Kansas Installments Fixed Rate Promissory Note Secured by Residential Real Estate is a legal document that outlines the terms and conditions of a loan agreement in Topeka, Kansas. This promissory note serves as evidence of the borrower's promise to repay a specific amount of money borrowed, along with any accrued interest, in regular installments over a fixed period of time. The loan is secured by residential real estate, meaning that the borrower pledges their property as collateral for the loan. In Topeka, Kansas, there may be different types of Installments Fixed Rate Promissory Notes Secured by Residential Real Estate, depending on various factors such as the loan amount, interest rate, repayment terms, and the borrower's creditworthiness. Some common types include: 1. Topeka Kansas Installments Fixed Rate Promissory Note with a Balloon Payment: This type of promissory note requires the borrower to make regular installments over a fixed period, with a larger final payment known as a balloon payment due at the end of the loan term. 2. Topeka Kansas Installments Fixed Rate Promissory Note with Adjustable Interest Rate: Unlike a traditional fixed-rate promissory note, this type of note allows for adjustable interest rates, which may change periodically based on market conditions and predetermined indexes. 3. Topeka Kansas Installments Fixed Rate Promissory Note with Prepayment Penalty: This type of promissory note may include a provision that imposes a penalty on the borrower if they choose to pay off the loan before its maturity date. 4. Topeka Kansas Installments Fixed Rate Promissory Note with Interest-Only Payments: In some cases, borrowers may opt for a promissory note that allows them to make interest-only payments for a certain period before beginning to repay the principal amount. It is important for both the lender and the borrower to carefully review and understand the terms stated in the Topeka Kansas Installments Fixed Rate Promissory Note Secured by Residential Real Estate before signing the agreement. Consulting with a qualified attorney or financial advisor can help ensure that all parties involved are protected and that the loan agreement meets legal requirements.

Topeka Kansas Installments Fixed Rate Promissory Note Secured by Residential Real Estate

Description

How to fill out Topeka Kansas Installments Fixed Rate Promissory Note Secured By Residential Real Estate?

If you are searching for a valid form, it’s impossible to choose a more convenient place than the US Legal Forms website – one of the most extensive libraries on the internet. With this library, you can get thousands of form samples for company and personal purposes by categories and regions, or keywords. Using our high-quality search function, finding the latest Topeka Kansas Installments Fixed Rate Promissory Note Secured by Residential Real Estate is as elementary as 1-2-3. In addition, the relevance of each and every document is proved by a group of expert lawyers that on a regular basis check the templates on our website and revise them based on the most recent state and county laws.

If you already know about our system and have an account, all you need to get the Topeka Kansas Installments Fixed Rate Promissory Note Secured by Residential Real Estate is to log in to your profile and click the Download button.

If you use US Legal Forms for the first time, just follow the guidelines listed below:

- Make sure you have found the sample you need. Check its description and utilize the Preview function to explore its content. If it doesn’t suit your needs, use the Search option at the top of the screen to discover the proper document.

- Affirm your selection. Click the Buy now button. Following that, pick your preferred subscription plan and provide credentials to sign up for an account.

- Make the purchase. Make use of your credit card or PayPal account to finish the registration procedure.

- Get the template. Select the format and download it to your system.

- Make modifications. Fill out, revise, print, and sign the received Topeka Kansas Installments Fixed Rate Promissory Note Secured by Residential Real Estate.

Each and every template you save in your profile does not have an expiry date and is yours permanently. You can easily gain access to them via the My Forms menu, so if you want to receive an extra version for modifying or creating a hard copy, feel free to return and export it once again anytime.

Take advantage of the US Legal Forms extensive catalogue to get access to the Topeka Kansas Installments Fixed Rate Promissory Note Secured by Residential Real Estate you were looking for and thousands of other professional and state-specific samples on a single website!