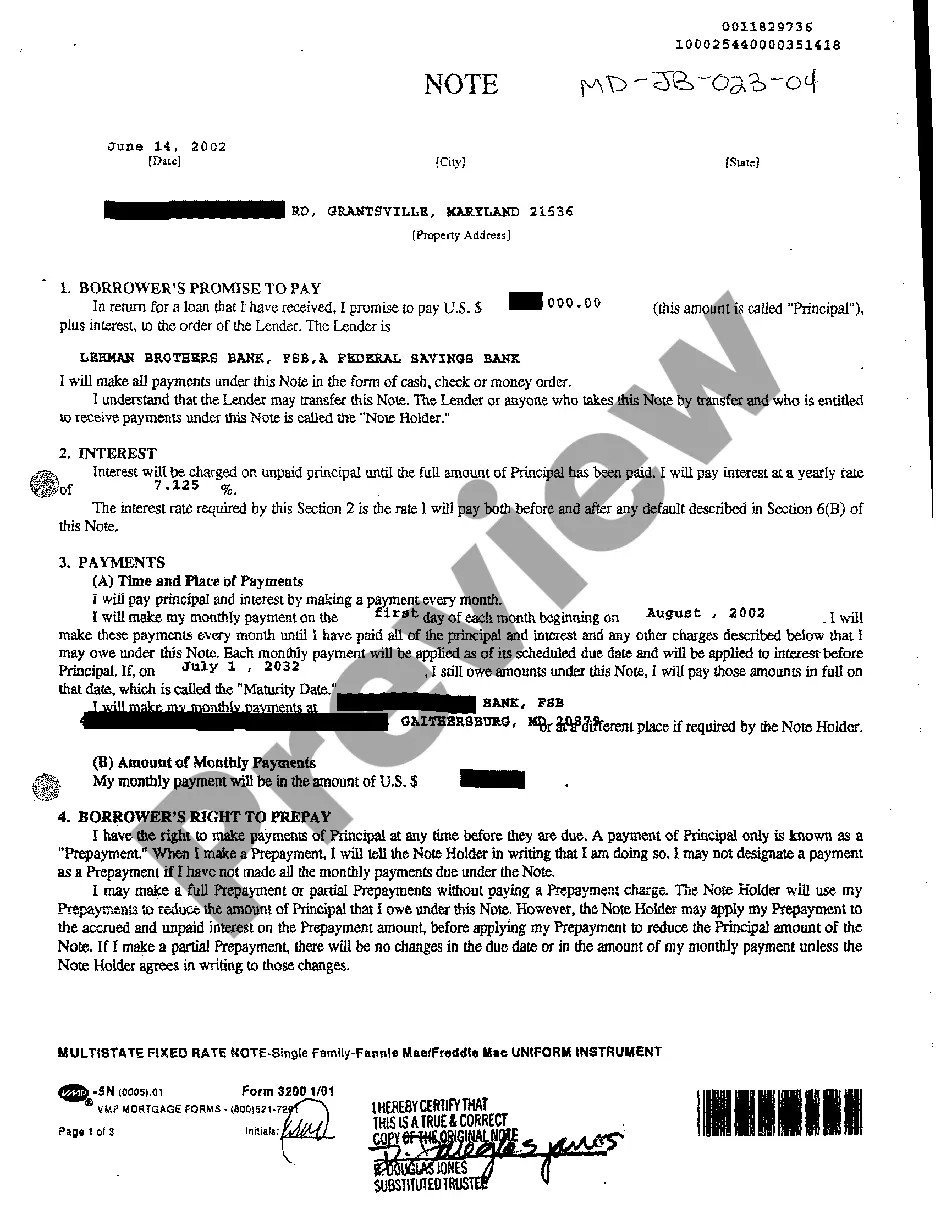

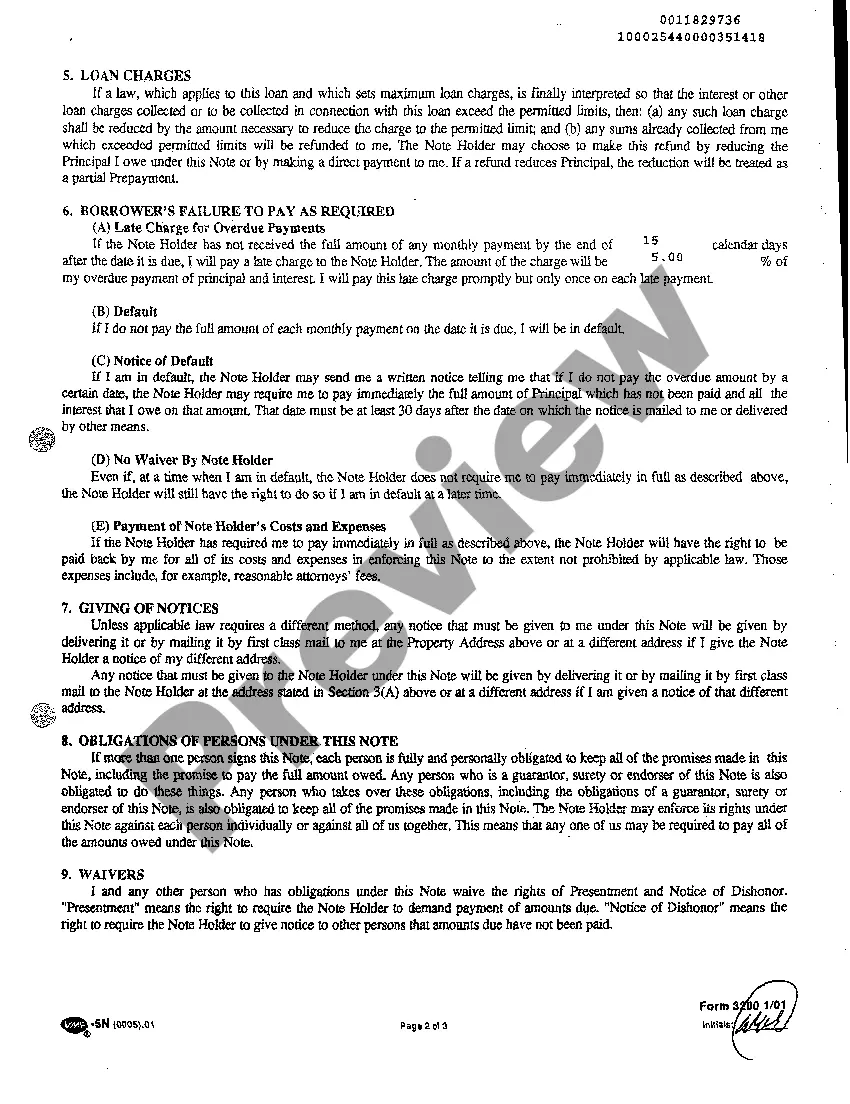

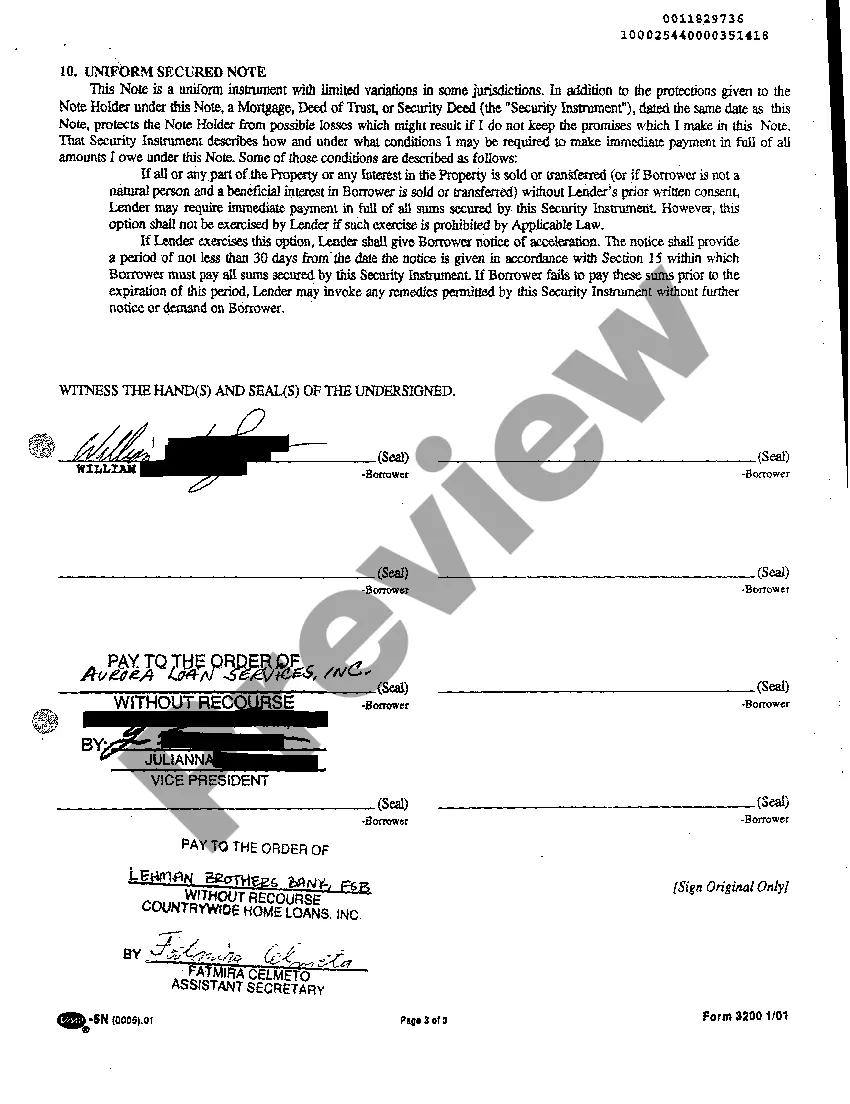

A Montgomery Maryland Promissory Note is a legally binding document that outlines the terms and conditions of a loan agreement between a lender and a borrower in Montgomery County, Maryland. It is a written promise to repay a specific amount of money borrowed, including any applicable interest, within a specified period. The Montgomery Maryland Promissory Note contains details such as the names and contact information of both parties involved, the principal loan amount, the interest rate (if applicable), the repayment schedule, the due dates, and any collateral or security provided for the loan. There are different types of Montgomery Maryland Promissory Notes, depending on the specific circumstances of the loan agreement: 1. Installment Promissory Note: This type of note sets out a predefined repayment schedule, dividing the loan amount into equal installments to be paid at regular intervals, typically monthly or quarterly. 2. Balloon Promissory Note: This note enables borrowers to make smaller periodic payments throughout the loan term, with a large final payment, the balloon payment, due at the end of the term. It allows borrowers to manage their cash flow more effectively but may involve higher interest rates. 3. Secured Promissory Note: This note includes collateral or security provided by the borrower to secure the loan. It ensures that if the borrower defaults, the lender has the right to seize the specified asset to recover the outstanding debt. Common forms of collateral include real estate, vehicles, or valuable personal property. 4. Unsecured Promissory Note: Unlike a secured note, an unsecured note does not require collateral. This type of note relies solely on the borrower's creditworthiness and personal guarantee to ensure repayment. It is crucial for both parties to carefully read and understand the terms and conditions outlined in the Montgomery Maryland Promissory Note before signing. Consulting with a legal professional might be advisable to ensure compliance with local laws and regulations and to protect the interests of both the borrower and the lender.

Montgomery Maryland Promissory Note

Description

How to fill out Montgomery Maryland Promissory Note?

We always strive to minimize or prevent legal damage when dealing with nuanced legal or financial matters. To do so, we apply for legal solutions that, usually, are extremely costly. Nevertheless, not all legal matters are equally complex. Most of them can be taken care of by ourselves.

US Legal Forms is a web-based library of updated DIY legal forms covering anything from wills and powers of attorney to articles of incorporation and petitions for dissolution. Our library helps you take your matters into your own hands without the need of turning to an attorney. We provide access to legal document templates that aren’t always openly accessible. Our templates are state- and area-specific, which considerably facilitates the search process.

Take advantage of US Legal Forms whenever you need to get and download the Montgomery Maryland Promissory Note or any other document easily and securely. Simply log in to your account and click the Get button next to it. If you happened to lose the form, you can always re-download it in the My Forms tab.

The process is just as straightforward if you’re new to the platform! You can create your account in a matter of minutes.

- Make sure to check if the Montgomery Maryland Promissory Note complies with the laws and regulations of your your state and area.

- Also, it’s imperative that you check out the form’s description (if available), and if you notice any discrepancies with what you were looking for in the first place, search for a different form.

- As soon as you’ve made sure that the Montgomery Maryland Promissory Note would work for you, you can choose the subscription plan and make a payment.

- Then you can download the form in any available format.

For over 24 years of our existence, we’ve helped millions of people by providing ready to customize and up-to-date legal forms. Make the most of US Legal Forms now to save efforts and resources!