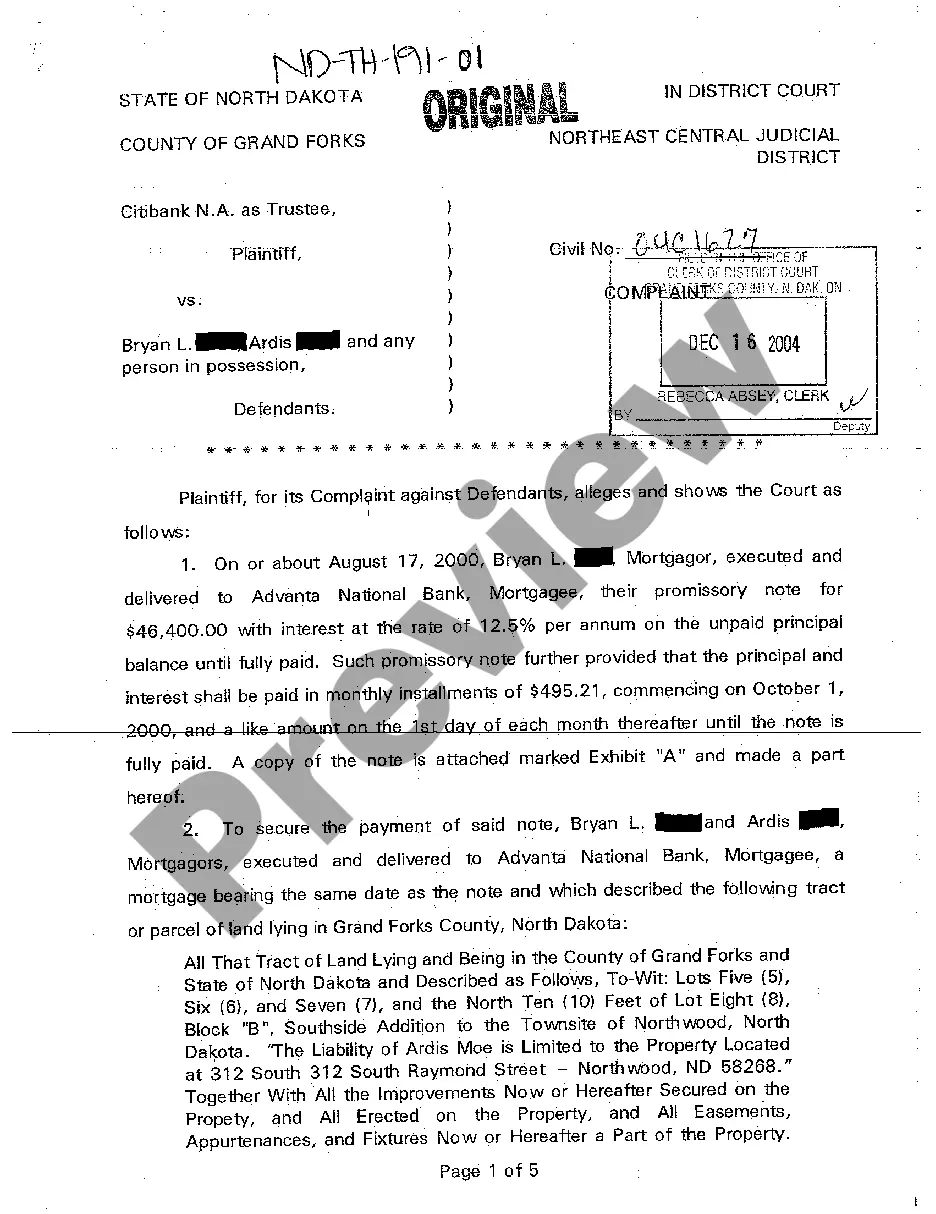

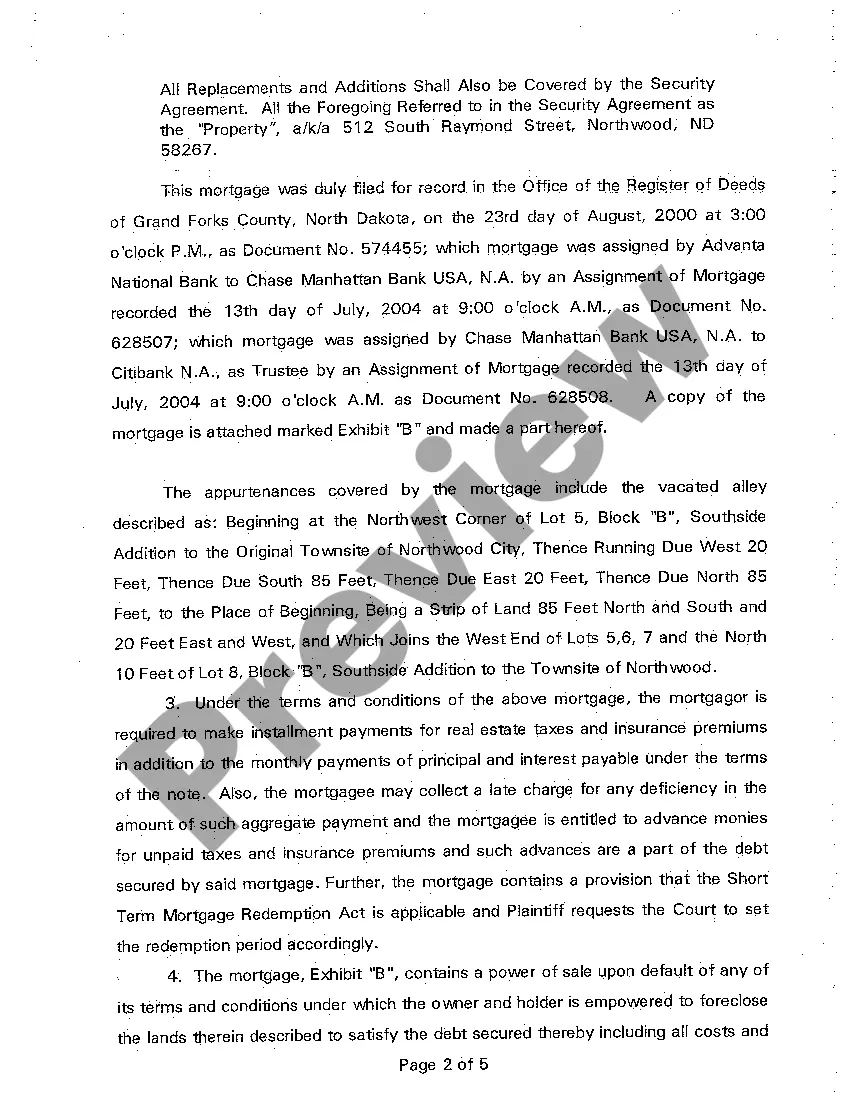

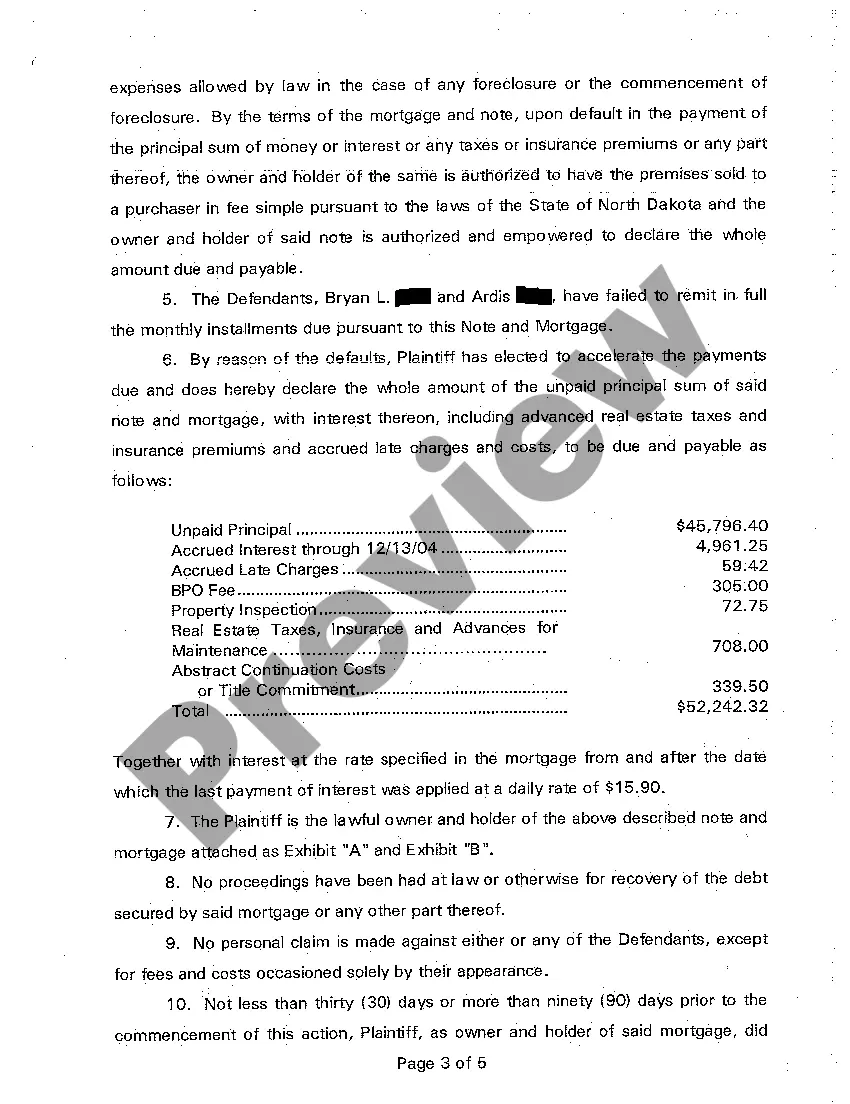

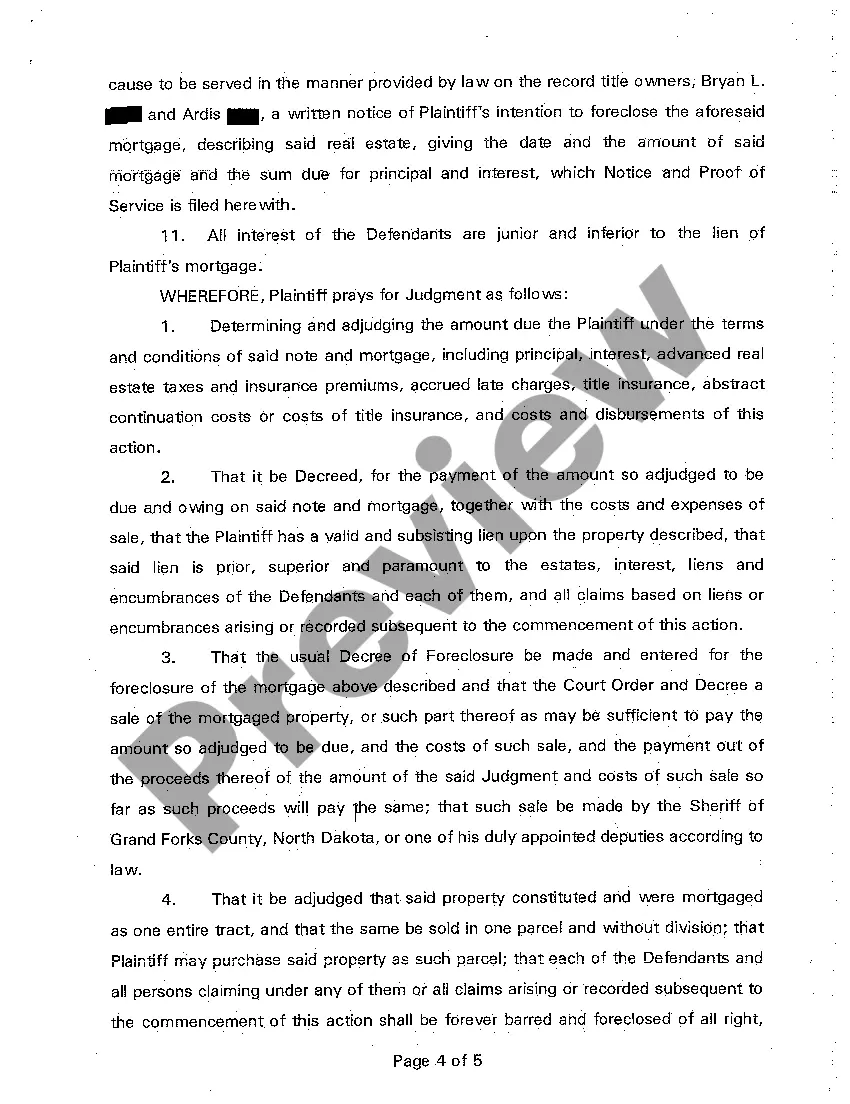

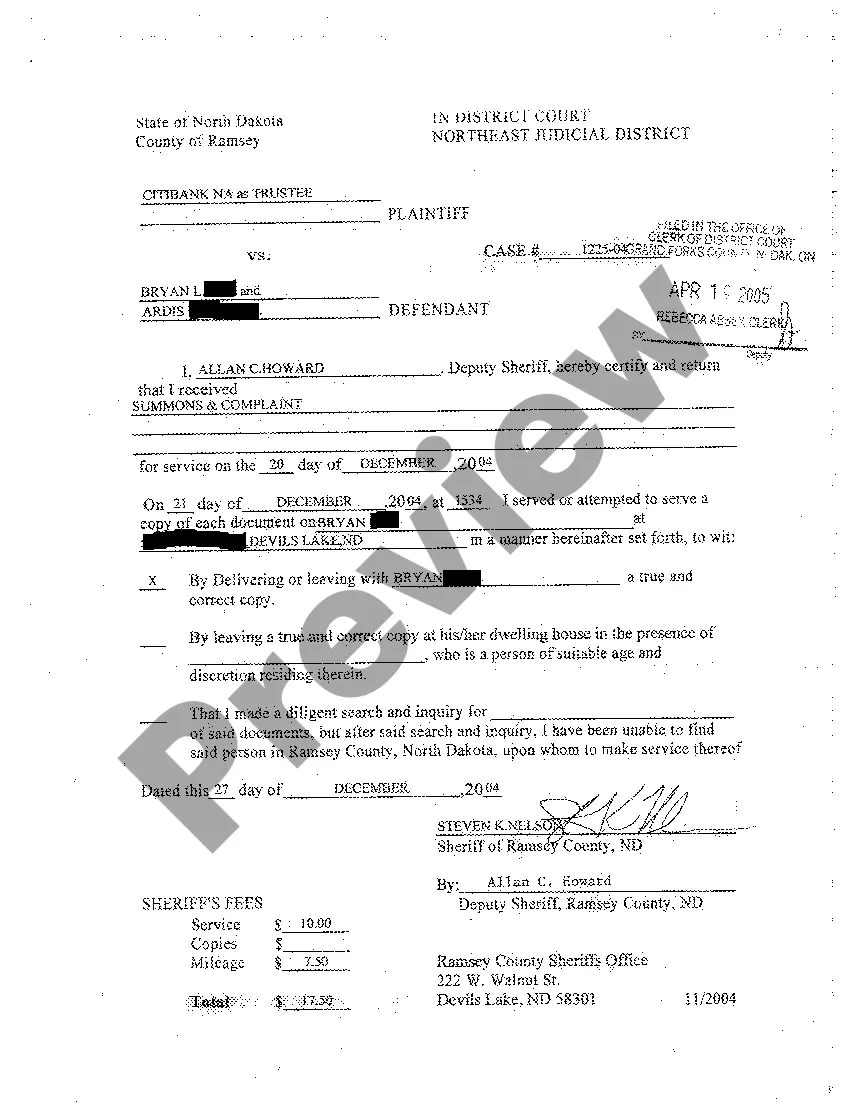

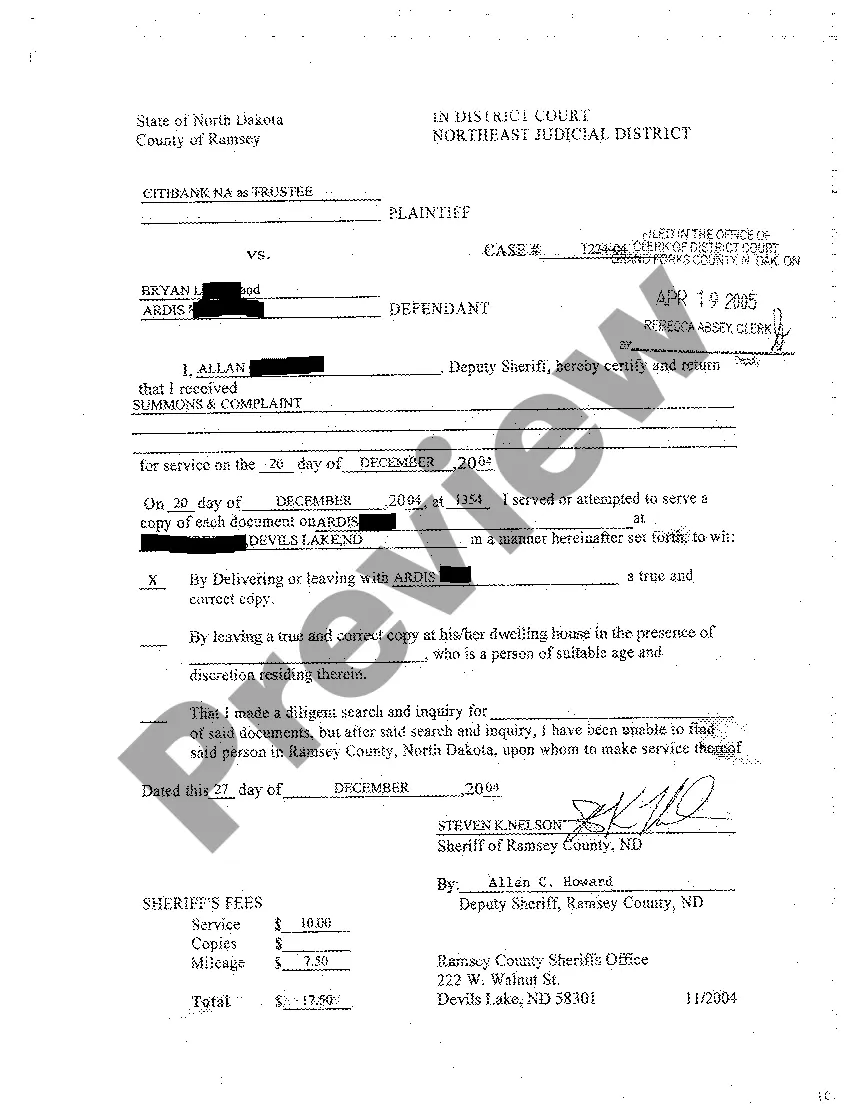

Title: Fargo, North Dakota Complaint for Foreclosure by Sale and Deficiency Judgment: Understanding the Process and Types Introduction: In Fargo, North Dakota, when a borrower fails to make mortgage payments, the lender may initiate foreclosure proceedings to recover the outstanding debt. This content aims to provide a detailed description of the Fargo North Dakota Complaint for Foreclosure by Sale and Deficiency Judgment process, along with relevant keywords. Additionally, we will explore the different types of foreclosure complaints that can be filed in Fargo, North Dakota. 1. What is a Foreclosure by Sale and Deficiency Judgment? Foreclosure by Sale and Deficiency Judgment is a legal process through which a lender, usually a mortgage company or bank, can reclaim a property from a borrower (mortgagor) who has defaulted on their mortgage payments. By obtaining a court order, the lender can auction the property to recover the remaining loan balance, including interest, fees, and costs. If the sale does not fully cover the debt, the lender may seek a deficiency judgment to collect the remaining amount from the borrower. 2. The Fargo, North Dakota Foreclosure Process: a. Initiation of Foreclosure: The lender must file a Complaint for Foreclosure by Sale and Deficiency Judgment with the appropriate court to begin the foreclosure process. b. Service of Complaint: The borrower (mortgagor) is served with a copy of the Complaint, outlining the lender's intention to foreclose. c. Opportunity to Respond: The borrower has a specified time frame to respond to the Complaint, typically by filing an answer with the court. d. Foreclosure Auction: If the court finds in favor of the lender, a foreclosure auction is scheduled where the property is sold to the highest bidder. e. Deficiency Judgment: If the sale proceeds are insufficient to cover the outstanding debt, the lender may file for a deficiency judgment to collect the remaining balance from the borrower. 3. Types of Fargo North Dakota Complaint for Foreclosure by Sale and Deficiency Judgment: a. Judicial Foreclosure Complaint: Filed with the court system and involves a lawsuit, court hearings, and judicial oversight. b. Non-Judicial Foreclosure Complaint: Occurs outside the court system, and the lender follows a specific process outlined in the mortgage or deed of trust contract. c. Residential Foreclosure Complaint: Specific to residential properties, involving homes or multifamily units. d. Commercial Foreclosure Complaint: Pertains to commercial properties, such as office buildings, retail centers, or industrial spaces. Conclusion: Understanding the Fargo, North Dakota Complaint for Foreclosure by Sale and Deficiency Judgment process is essential for borrowers and lenders alike. By comprehending the different types of foreclosure complaints, individuals can navigate the foreclosure process more effectively. Seeking legal advice from foreclosure specialists can provide invaluable guidance to borrowers facing foreclosure, helping them explore options and potentially mitigate the financial impact.

Fargo North Dakota Complaint for Foreclosure by Sale and Deficiency Judgment

Description

How to fill out Fargo North Dakota Complaint For Foreclosure By Sale And Deficiency Judgment?

Regardless of social or professional status, filling out law-related forms is an unfortunate necessity in today’s world. Too often, it’s virtually impossible for someone without any law education to create this sort of paperwork from scratch, mostly due to the convoluted terminology and legal subtleties they entail. This is where US Legal Forms comes in handy. Our platform provides a massive library with more than 85,000 ready-to-use state-specific forms that work for pretty much any legal scenario. US Legal Forms also is a great resource for associates or legal counsels who want to to be more efficient time-wise utilizing our DYI forms.

No matter if you require the Fargo North Dakota Complaint for Foreclosure by Sale and Deficiency Judgment or any other paperwork that will be good in your state or county, with US Legal Forms, everything is on hand. Here’s how to get the Fargo North Dakota Complaint for Foreclosure by Sale and Deficiency Judgment in minutes employing our trusted platform. If you are already a subscriber, you can proceed to log in to your account to download the needed form.

However, in case you are new to our platform, make sure to follow these steps before obtaining the Fargo North Dakota Complaint for Foreclosure by Sale and Deficiency Judgment:

- Be sure the template you have chosen is suitable for your location since the regulations of one state or county do not work for another state or county.

- Preview the document and read a quick outline (if available) of scenarios the paper can be used for.

- If the form you picked doesn’t meet your requirements, you can start again and search for the necessary document.

- Click Buy now and pick the subscription option you prefer the best.

- Access an account {using your credentials or register for one from scratch.

- Pick the payment gateway and proceed to download the Fargo North Dakota Complaint for Foreclosure by Sale and Deficiency Judgment as soon as the payment is completed.

You’re good to go! Now you can proceed to print out the document or complete it online. Should you have any problems locating your purchased forms, you can quickly find them in the My Forms tab.

Whatever case you’re trying to sort out, US Legal Forms has got you covered. Try it out now and see for yourself.