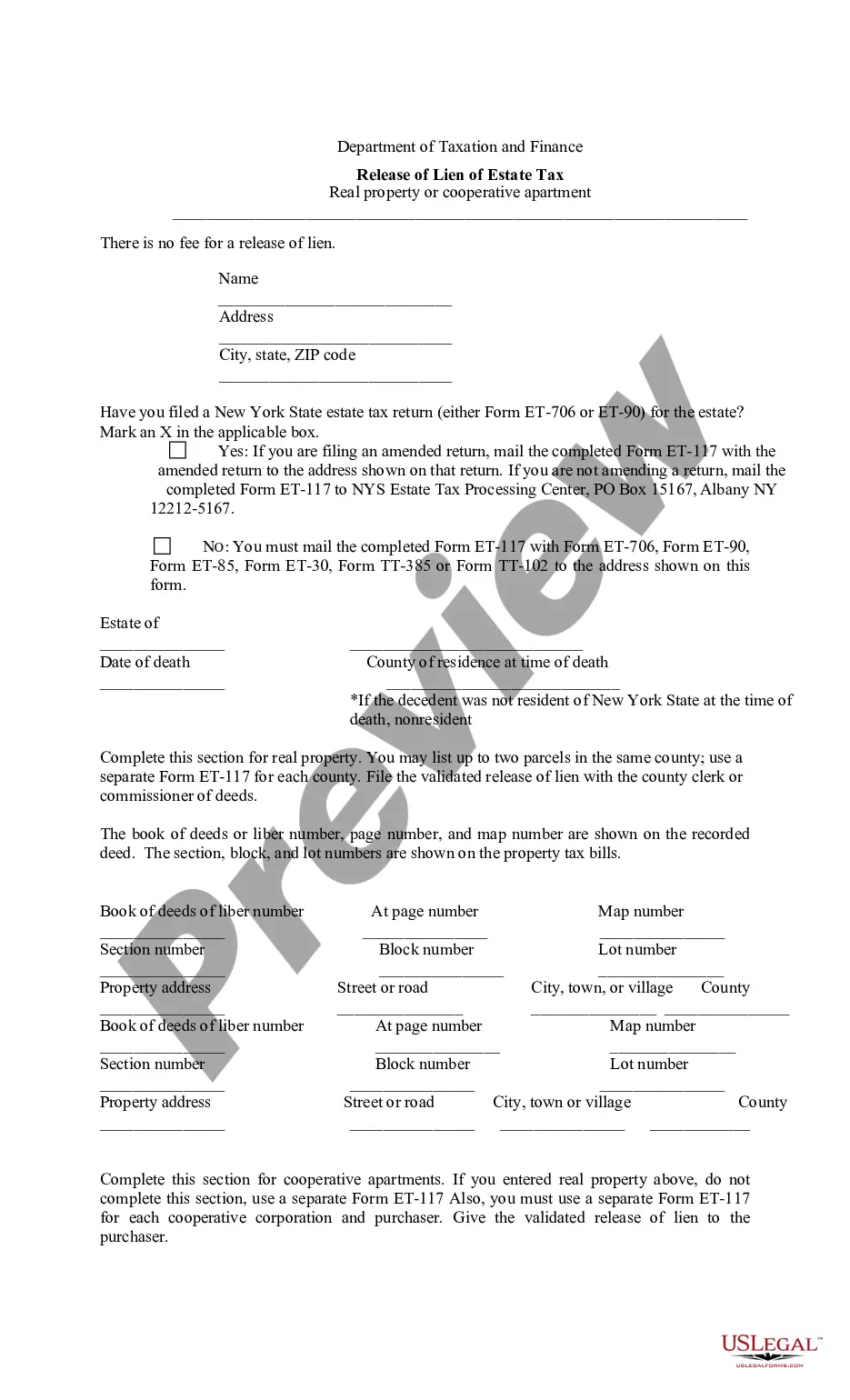

A Syracuse New York Release of Lien of Estate Tax is a legal document that indicates the removal or cancellation of a previously imposed lien on a property's estate due to unpaid estate taxes in Syracuse, New York. This document plays a crucial role in releasing the property from any encumbrance related to estate tax liens, allowing for smoother property transactions or transfers of ownership. The Syracuse New York Release of Lien of Estate Tax is typically issued by the relevant government authority responsible for collecting estate taxes in Onondaga County, Syracuse. This document serves as proof that the outstanding estate tax liabilities have been satisfied and the lien on the property is now released or discharged. Keywords: Syracuse New York, Release of Lien of Estate Tax, estate taxes, lien removal, property encumbrance, property transactions, transfers of ownership, Onondaga County, discharge of lien. Different Types of Syracuse New York Release of Lien of Estate Tax: 1. Full Discharge of Estate Tax Lien: This type of release of lien is issued when all estate tax liabilities related to the property have been fully paid, and the lien is completely removed. It provides a clean title for the property, ensuring no legal issues arise during subsequent ownership transfers or transactions. 2. Partial Discharge of Estate Tax Lien: In some cases, the estate tax liabilities may only be partially satisfied, and the lien is released accordingly. This type of release of lien acknowledges partial payment and may still impose restrictions on the property until the remaining amount is settled. 3. Conditional Release of Estate Tax Lien: A conditional release of lien is granted when certain conditions are met, allowing for a temporary or limited release of the lien. This could occur when an estate tax payment plan is agreed upon between the taxpayer and the taxing authority, ensuring regular installment payments are made over a specified period. 4. Release of Lien Pending Payment: If a taxpayer contests the estate tax liability, a release of lien pending payment may be issued. This allows for the release of the lien while the case is being resolved or pending further assessment. It provides temporary relief from the lien's encumbrance, but the final outcome may require the lien to be reinstated or discharged based on the assessment results. Keywords: Full Discharge, Partial Discharge, Conditional Release, Pending Payment, estate tax liabilities, temporary relief, assessment results, contests.

Syracuse New York Release of Lien of Estate Tax

Description

How to fill out Syracuse New York Release Of Lien Of Estate Tax?

Do you need a reliable and inexpensive legal forms provider to buy the Syracuse New York Release of Lien of Estate Tax? US Legal Forms is your go-to option.

No matter if you require a simple arrangement to set regulations for cohabitating with your partner or a package of forms to advance your separation or divorce through the court, we got you covered. Our platform provides more than 85,000 up-to-date legal document templates for personal and business use. All templates that we offer aren’t generic and framed in accordance with the requirements of separate state and county.

To download the document, you need to log in account, find the required form, and hit the Download button next to it. Please take into account that you can download your previously purchased document templates at any time from the My Forms tab.

Are you new to our platform? No worries. You can set up an account with swift ease, but before that, make sure to do the following:

- Find out if the Syracuse New York Release of Lien of Estate Tax conforms to the regulations of your state and local area.

- Read the form’s description (if available) to find out who and what the document is intended for.

- Start the search over in case the form isn’t good for your specific scenario.

Now you can register your account. Then choose the subscription option and proceed to payment. Once the payment is completed, download the Syracuse New York Release of Lien of Estate Tax in any available file format. You can return to the website when you need and redownload the document free of charge.

Finding up-to-date legal forms has never been easier. Give US Legal Forms a go now, and forget about wasting your valuable time learning about legal paperwork online once and for all.