Queens New York Building Loan Agreement is a legal document that outlines the terms and conditions agreed upon by the borrower and the lender for obtaining a loan specifically for building or renovating properties in Queens, New York. This agreement is crucial in the construction or renovation process as it helps facilitate the financial aspects of real estate development in Queens. The primary purpose of a Queens New York Building Loan Agreement is to set forth the loan amount, interest rate, repayment terms, and any additional fees or charges involved in securing the loan. It provides clarity and protection for both parties involved, ensuring that each party fulfills their responsibilities in accordance with the agreement. Within Queens, New York, there are several types of building loan agreements that cater to different needs and situations: 1. Residential Construction Loan Agreement: This agreement is specifically designed for individuals or developers seeking financial support to build or renovate residential properties in Queens, New York. It includes details such as construction timelines, project milestones, and disbursement schedules to ensure efficient project management. 2. Commercial Construction Loan Agreement: This type of agreement targets businesses or developers who require funding for constructing or expanding commercial properties, such as office buildings, retail spaces, or industrial complexes in Queens, New York. The terms and conditions of this agreement may differ from residential construction loans due to the complexities associated with commercial projects. 3. Renovation Loan Agreement: This agreement focuses on borrowers who wish to renovate existing properties in Queens, New York. It allows homeowners or investors to secure funds for renovations, repairs, or upgrades, enabling them to enhance the value and functionality of their properties. When entering into a Queens New York Building Loan Agreement, both borrowers and lenders need to carefully review and understand the terms and conditions, interest rates, repayment schedules, and any penalties or defaults specified in the document. Consulting with legal professionals and financial advisors specialized in real estate is highly advised to ensure compliance with local regulations and to mitigate any potential risks involved in the loan agreement.

Queens New York Building Loan Agreement

State:

New York

County:

Queens

Control #:

NY-LR042T

Format:

Word;

Rich Text

Instant download

Description

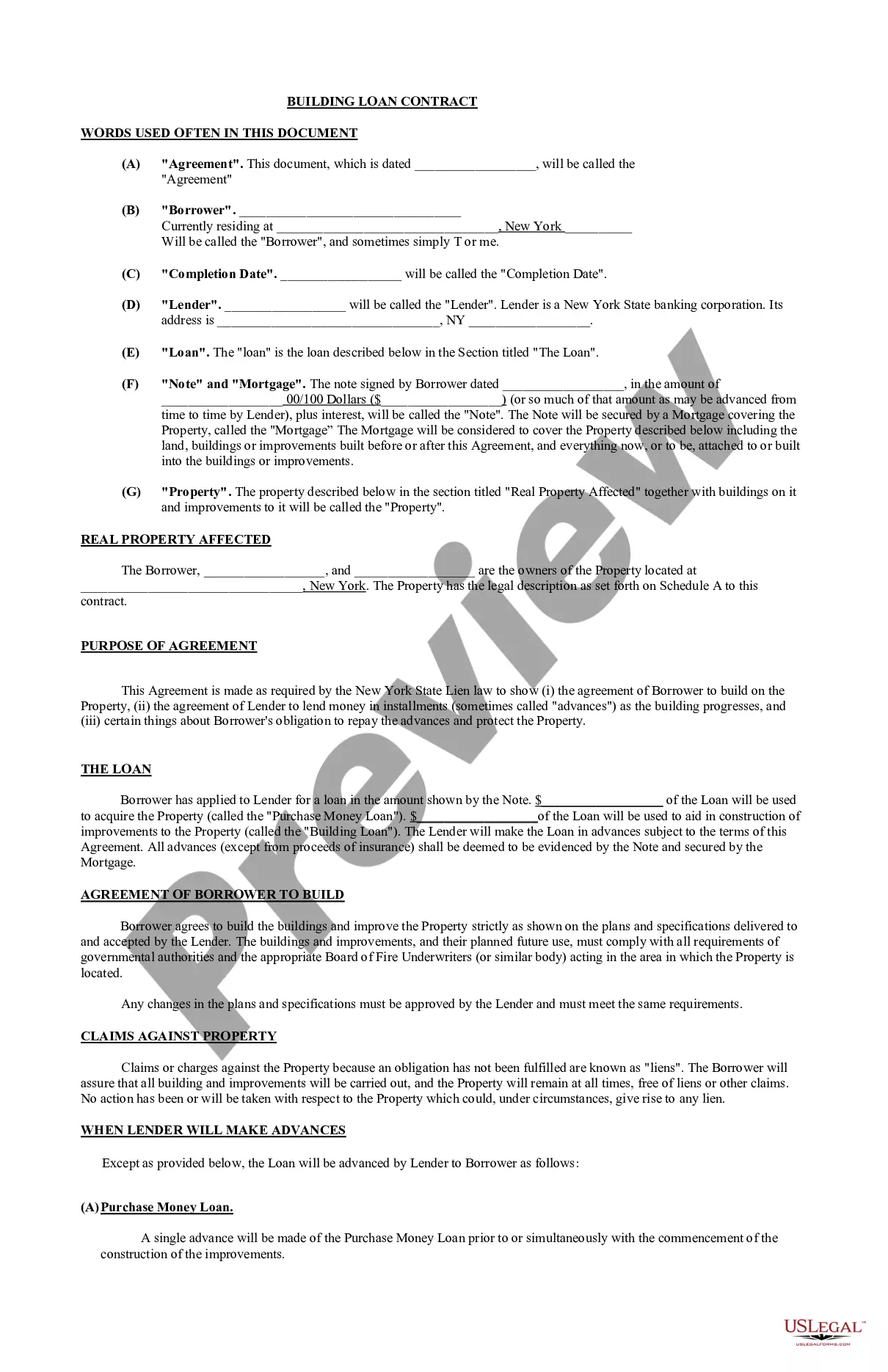

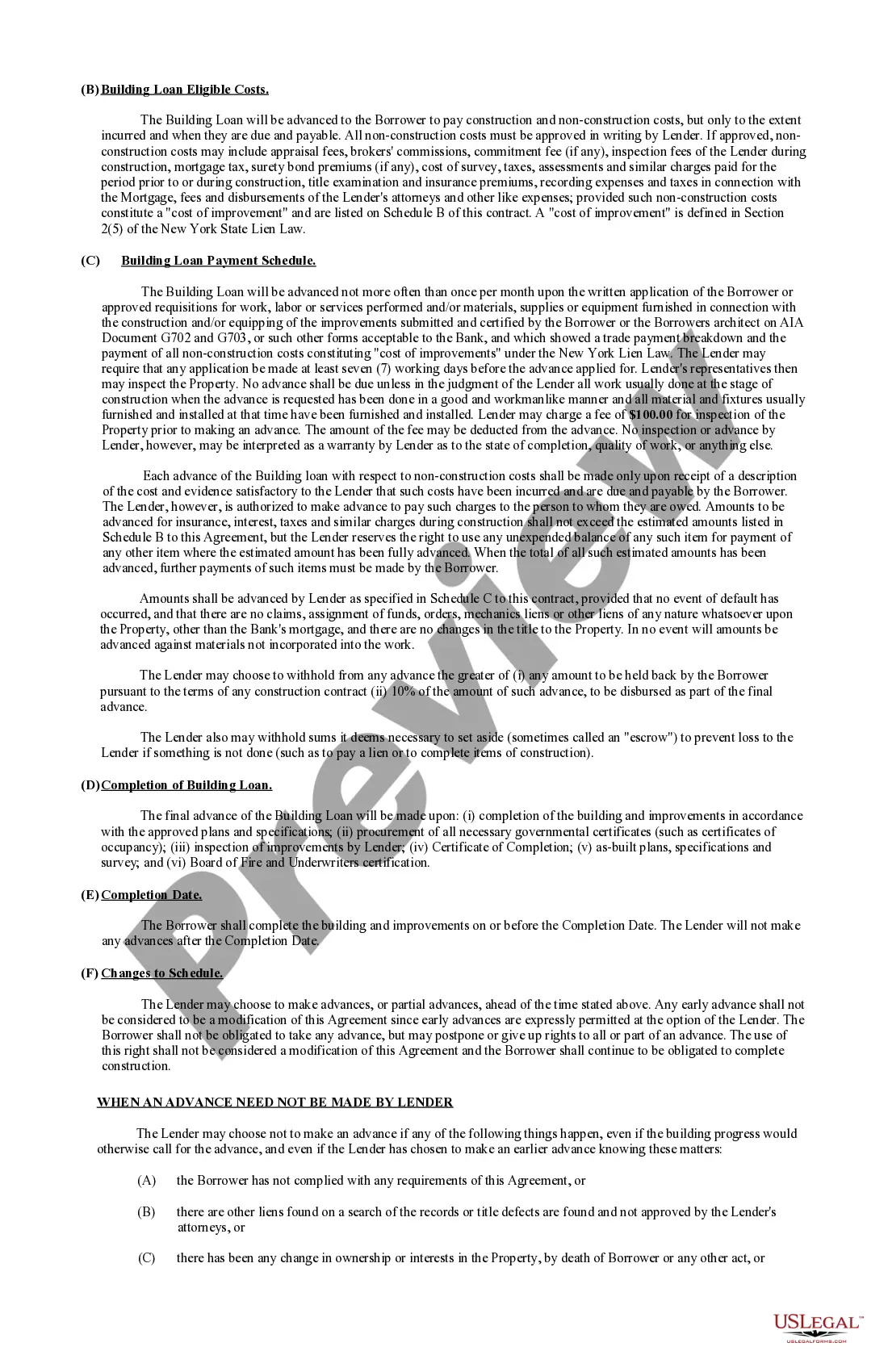

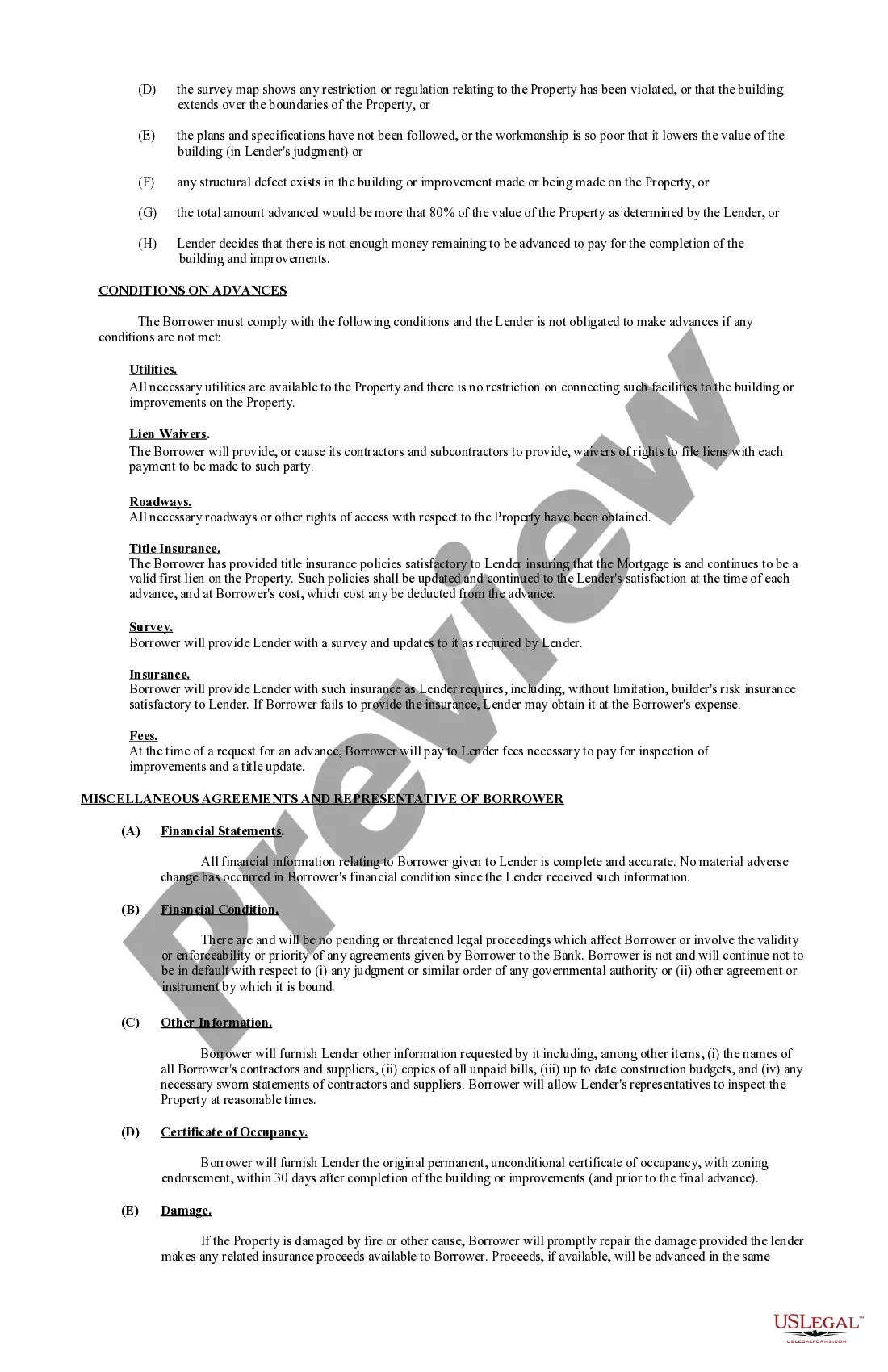

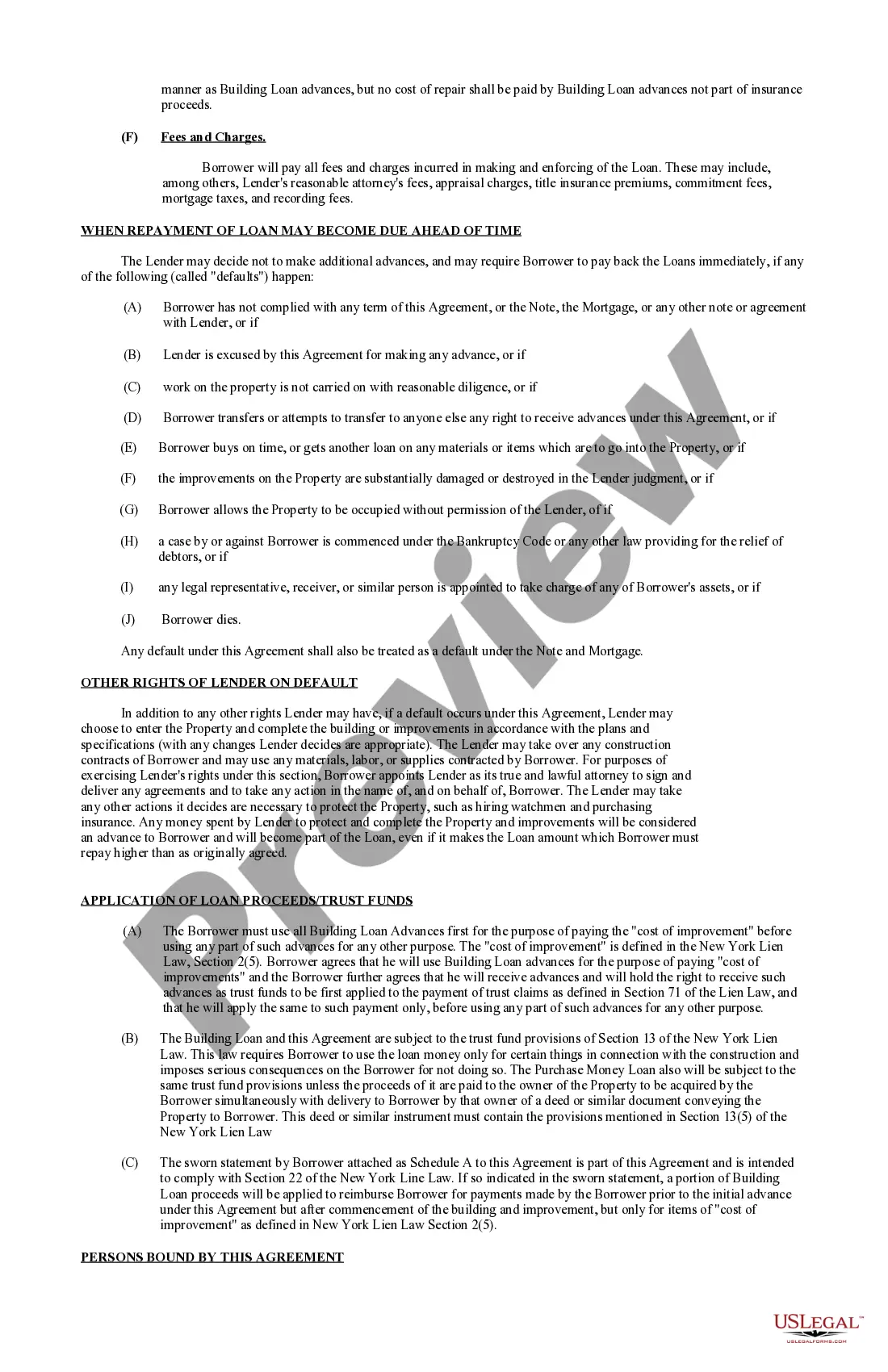

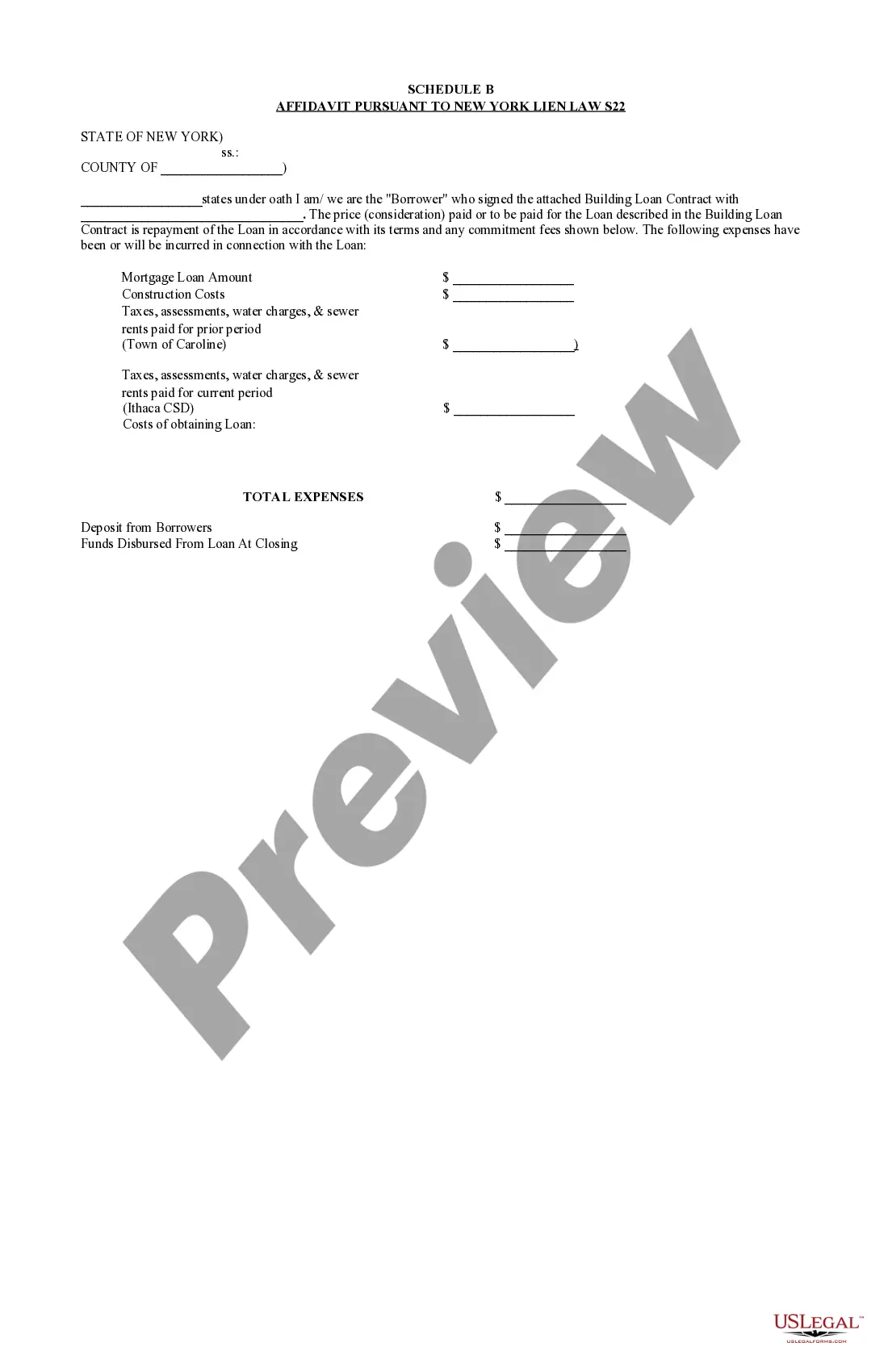

This building loan agreement is an agreement by which the lender advances money to an owner at fixed stages of construction.

Queens New York Building Loan Agreement is a legal document that outlines the terms and conditions agreed upon by the borrower and the lender for obtaining a loan specifically for building or renovating properties in Queens, New York. This agreement is crucial in the construction or renovation process as it helps facilitate the financial aspects of real estate development in Queens. The primary purpose of a Queens New York Building Loan Agreement is to set forth the loan amount, interest rate, repayment terms, and any additional fees or charges involved in securing the loan. It provides clarity and protection for both parties involved, ensuring that each party fulfills their responsibilities in accordance with the agreement. Within Queens, New York, there are several types of building loan agreements that cater to different needs and situations: 1. Residential Construction Loan Agreement: This agreement is specifically designed for individuals or developers seeking financial support to build or renovate residential properties in Queens, New York. It includes details such as construction timelines, project milestones, and disbursement schedules to ensure efficient project management. 2. Commercial Construction Loan Agreement: This type of agreement targets businesses or developers who require funding for constructing or expanding commercial properties, such as office buildings, retail spaces, or industrial complexes in Queens, New York. The terms and conditions of this agreement may differ from residential construction loans due to the complexities associated with commercial projects. 3. Renovation Loan Agreement: This agreement focuses on borrowers who wish to renovate existing properties in Queens, New York. It allows homeowners or investors to secure funds for renovations, repairs, or upgrades, enabling them to enhance the value and functionality of their properties. When entering into a Queens New York Building Loan Agreement, both borrowers and lenders need to carefully review and understand the terms and conditions, interest rates, repayment schedules, and any penalties or defaults specified in the document. Consulting with legal professionals and financial advisors specialized in real estate is highly advised to ensure compliance with local regulations and to mitigate any potential risks involved in the loan agreement.

Free preview

How to fill out Queens New York Building Loan Agreement?

If you’ve already utilized our service before, log in to your account and save the Queens New York Building Loan Agreement on your device by clicking the Download button. Make sure your subscription is valid. If not, renew it according to your payment plan.

If this is your first experience with our service, adhere to these simple steps to get your file:

- Make certain you’ve found an appropriate document. Read the description and use the Preview option, if any, to check if it meets your needs. If it doesn’t suit you, use the Search tab above to get the proper one.

- Purchase the template. Click the Buy Now button and select a monthly or annual subscription plan.

- Create an account and make a payment. Use your credit card details or the PayPal option to complete the transaction.

- Get your Queens New York Building Loan Agreement. Choose the file format for your document and save it to your device.

- Complete your sample. Print it out or take advantage of professional online editors to fill it out and sign it electronically.

You have constant access to every piece of paperwork you have bought: you can locate it in your profile within the My Forms menu whenever you need to reuse it again. Take advantage of the US Legal Forms service to quickly find and save any template for your individual or professional needs!