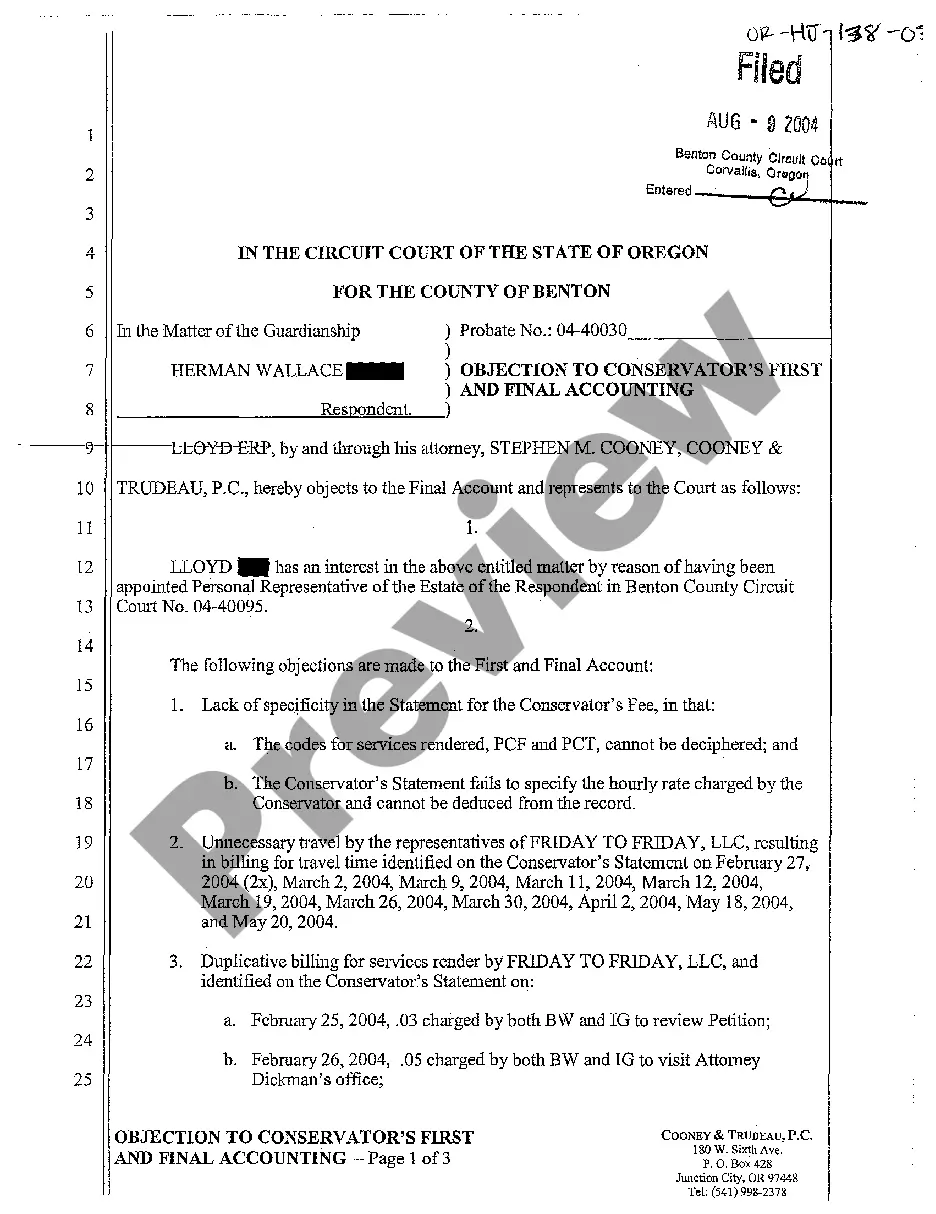

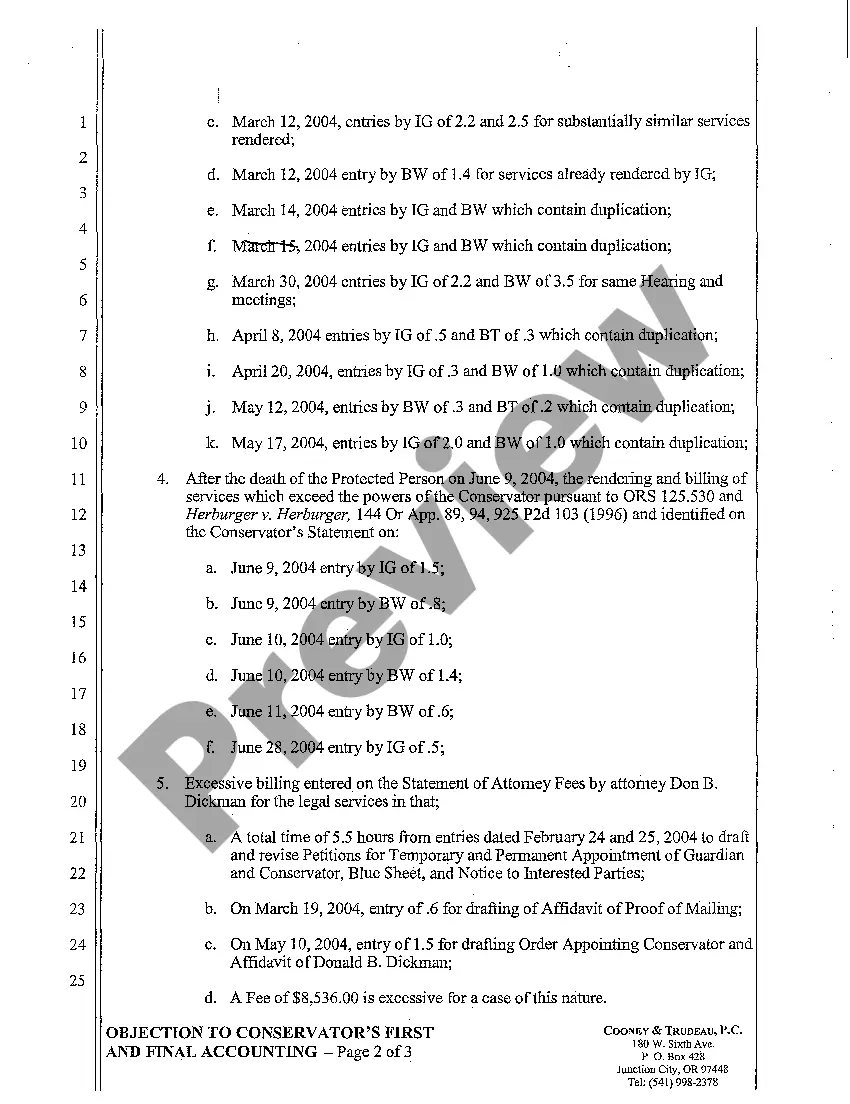

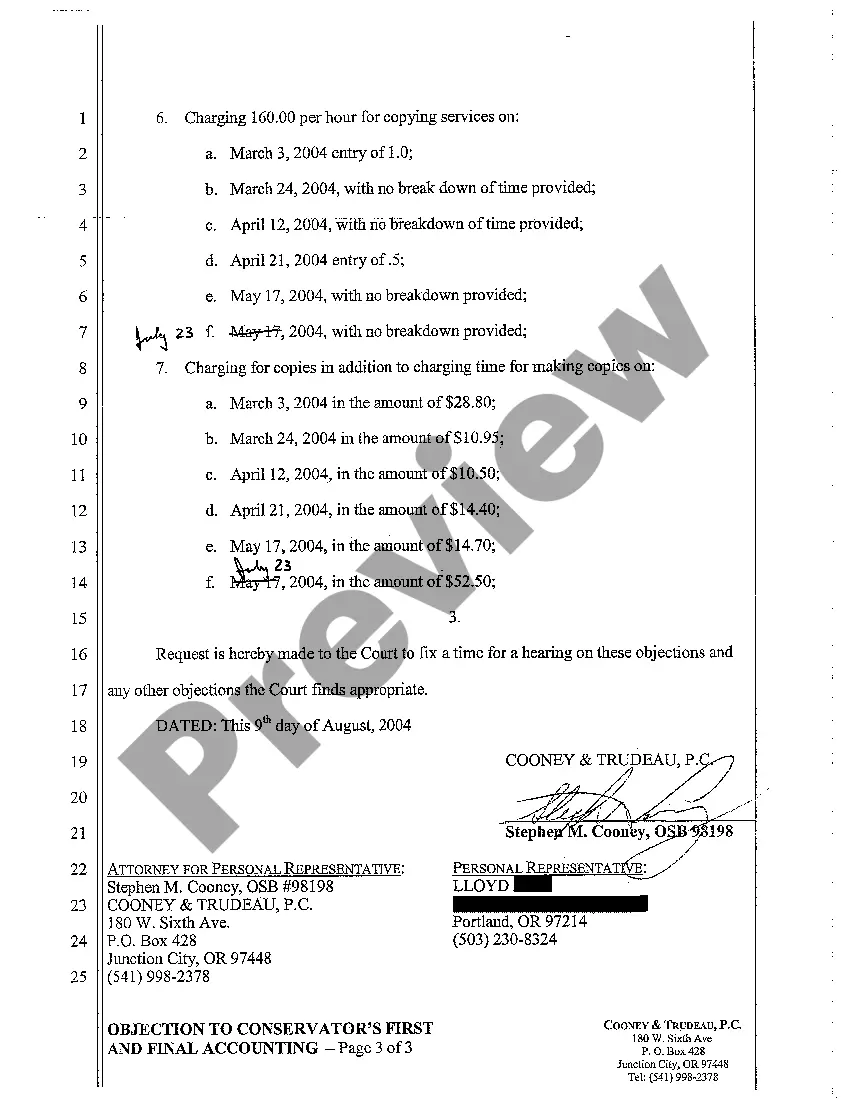

Gresham Oregon Objection to Conservator's First and Final Accounting refers to the legal process in Gresham, Oregon, where an individual or interested party challenges or raises concerns regarding a conservator's initial and final financial report. This objection may arise due to various circumstances and can occur in different situations. One type of objection to the conservator's first and final accounting could be based on discrepancies or errors in the financial records presented. If the accounting seems inaccurate, incomplete, or fails to adhere to relevant laws or regulations, an objection can be raised. Another type of objection may revolve around the mismanagement or mishandling of funds by the conservator. This objection occurs if there is evidence of unauthorized expenses, misuse of assets, or if the conservator fails to demonstrate proper financial stewardship. Additionally, objections can arise if there are suspicions of fraud or financial impropriety on the part of the conservator. This could include instances where the conservator engages in self-dealing, conflicts of interest, or unjust enrichment. Other common grounds for objections may include concerns over inadequate documentation, failure to provide supporting evidence or invoices, improper distribution of assets, failure to notify interested parties, or a lack of transparency in the accounting process. It is important to note that each objection is unique and must be supported by relevant evidence and legal reasoning. The objection process typically involves filing a formal written objection with the appropriate court, outlining the specific concerns and requesting a hearing to present evidence and arguments. Overall, the Gresham Oregon Objection to Conservator's First and Final Accounting occurs when interested parties question the accuracy, transparency, and appropriateness of a conservator's financial report or actions. By raising objections, individuals aim to ensure that the conservator is fulfilling their fiduciary duty and acting in the best interests of the protected person or estate.

Gresham Oregon Objection to Conservator's First and Final Accounting

Description

How to fill out Gresham Oregon Objection To Conservator's First And Final Accounting?

No matter what social or professional status, filling out legal documents is an unfortunate necessity in today’s world. Too often, it’s practically impossible for someone with no law education to draft such paperwork cfrom the ground up, mostly because of the convoluted jargon and legal subtleties they involve. This is where US Legal Forms can save the day. Our platform provides a massive library with over 85,000 ready-to-use state-specific documents that work for almost any legal situation. US Legal Forms also serves as a great asset for associates or legal counsels who want to save time using our DYI tpapers.

No matter if you want the Gresham Oregon Objection to Conservator's First and Final Accounting or any other paperwork that will be good in your state or county, with US Legal Forms, everything is on hand. Here’s how you can get the Gresham Oregon Objection to Conservator's First and Final Accounting quickly using our trustworthy platform. If you are already an existing customer, you can go ahead and log in to your account to get the appropriate form.

However, if you are new to our platform, make sure to follow these steps prior to obtaining the Gresham Oregon Objection to Conservator's First and Final Accounting:

- Be sure the template you have found is suitable for your area since the regulations of one state or county do not work for another state or county.

- Preview the document and go through a quick outline (if available) of scenarios the document can be used for.

- In case the form you picked doesn’t meet your requirements, you can start again and look for the needed document.

- Click Buy now and pick the subscription option you prefer the best.

- with your login information or register for one from scratch.

- Choose the payment method and proceed to download the Gresham Oregon Objection to Conservator's First and Final Accounting as soon as the payment is completed.

You’re good to go! Now you can go ahead and print the document or fill it out online. Should you have any problems getting your purchased documents, you can easily access them in the My Forms tab.

Whatever case you’re trying to sort out, US Legal Forms has got you covered. Give it a try today and see for yourself.