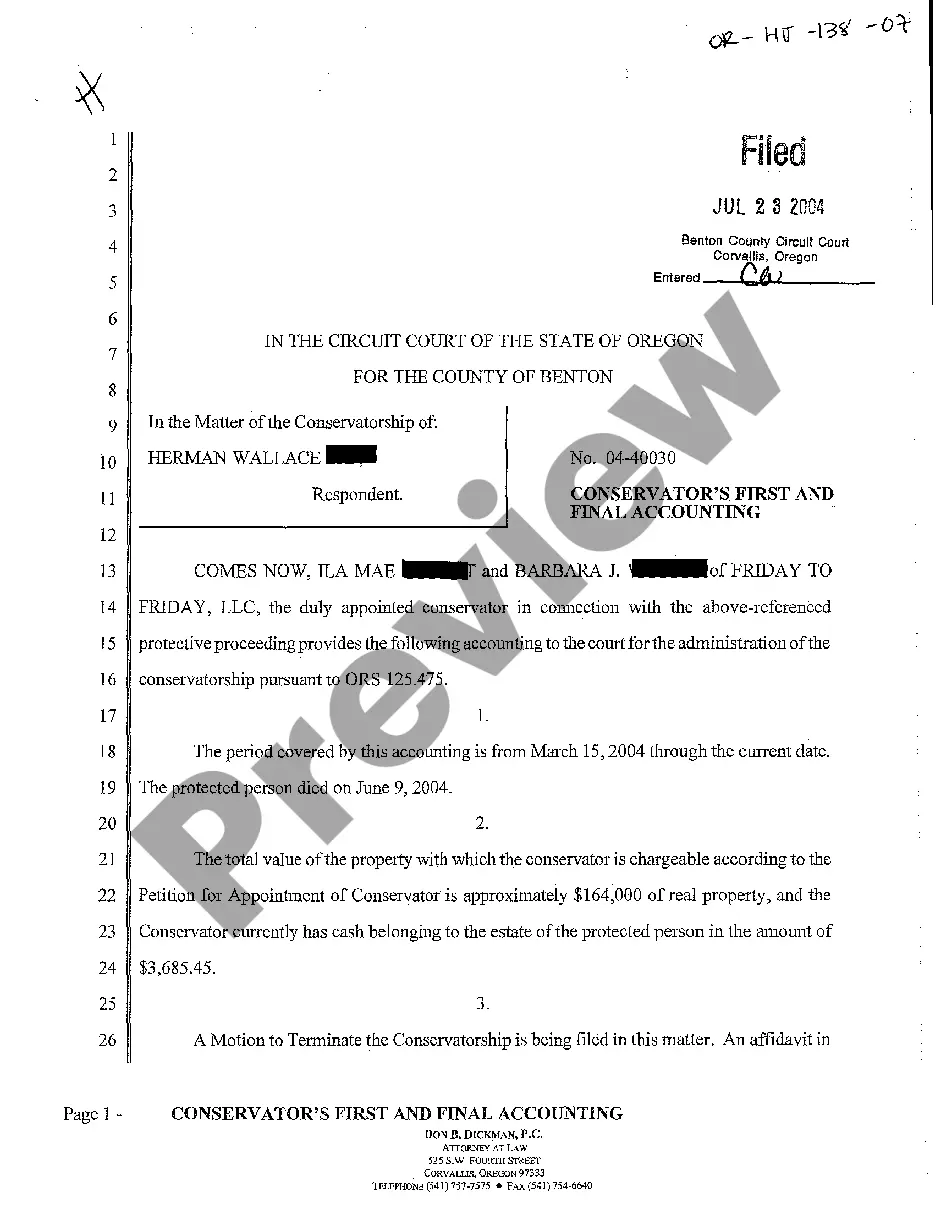

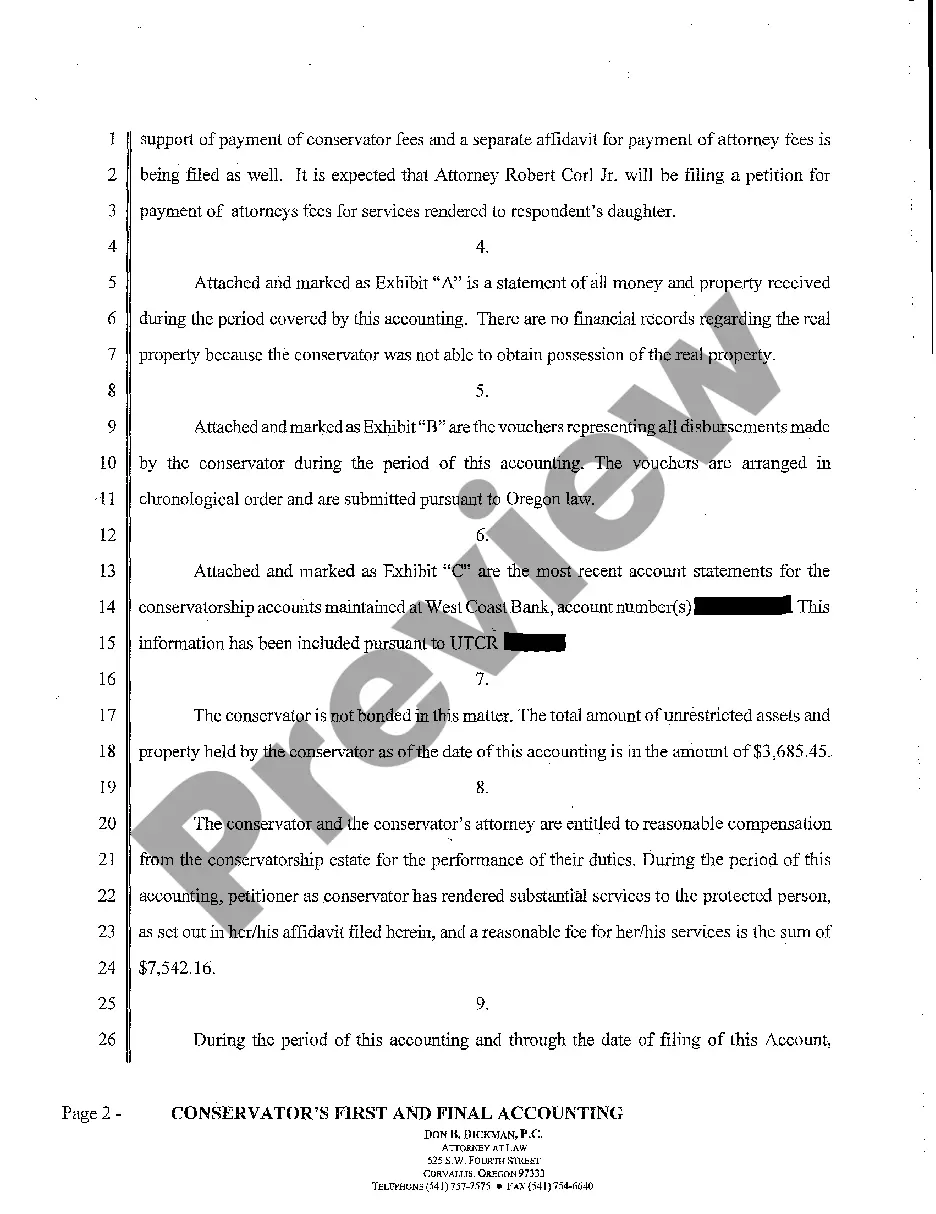

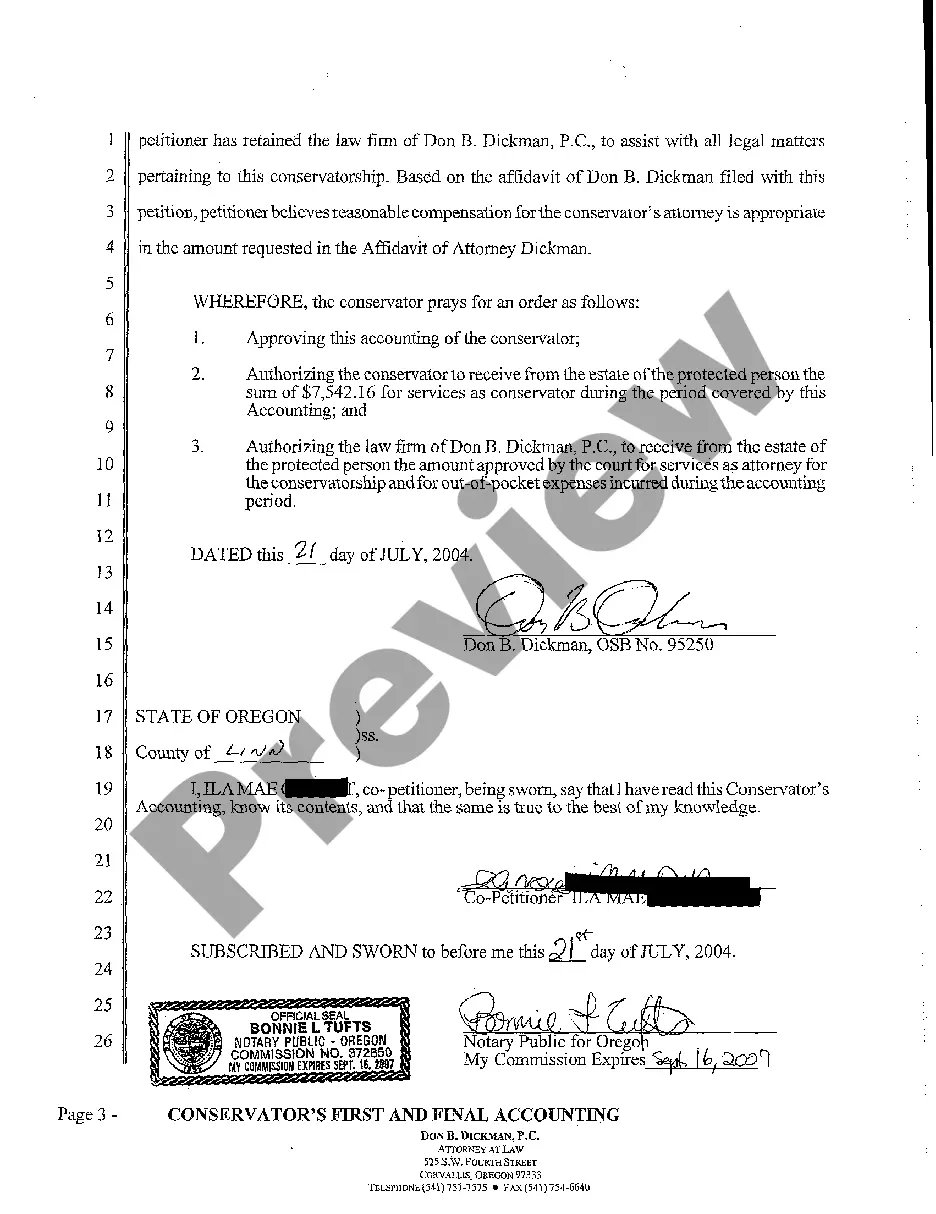

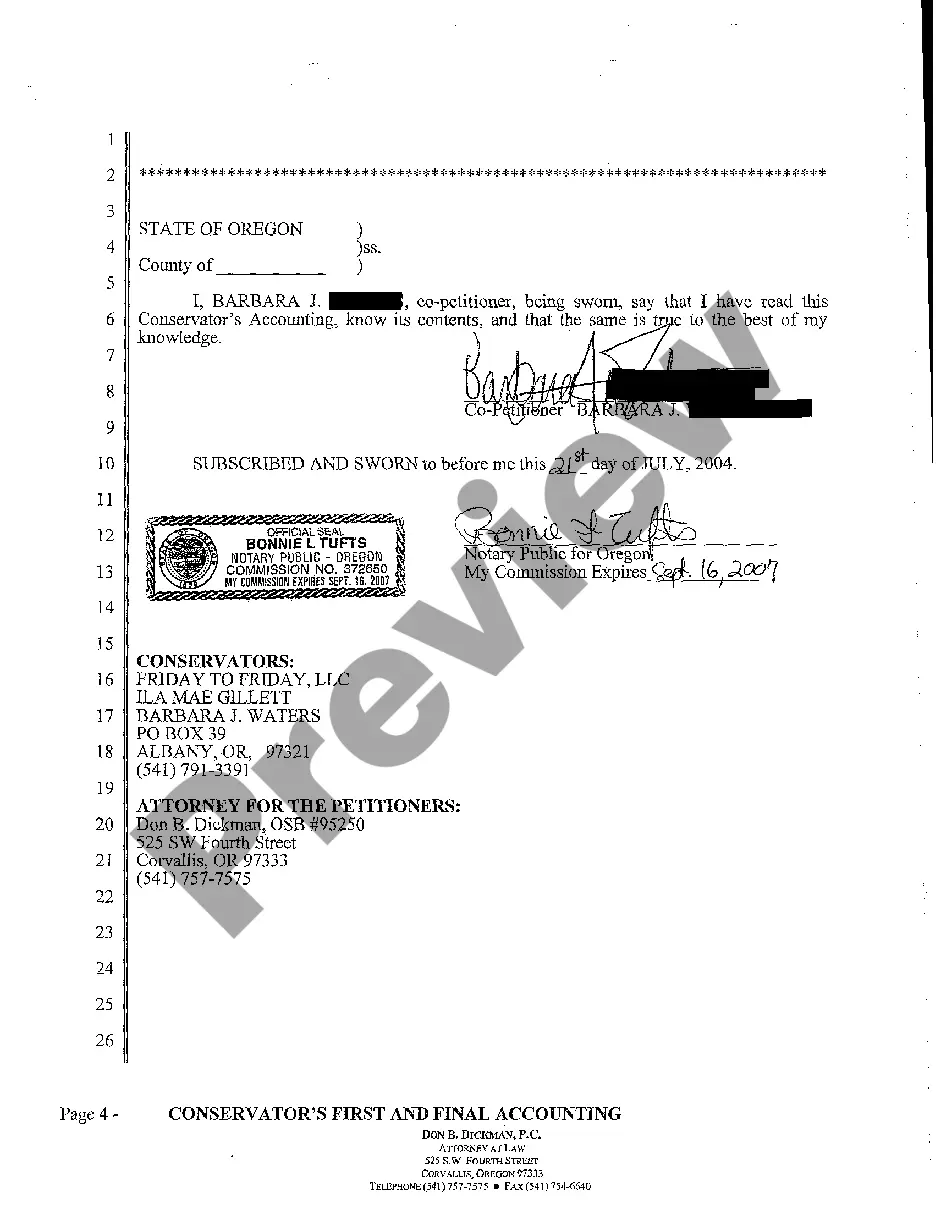

Hillsboro Oregon Conservator's First and Final Accounting is a crucial financial document that plays a significant role in the conservatorship process in Hillsboro, Oregon. This accounting serves to provide a transparent and detailed overview of the conservator's management of a protected person's assets and financial matters. Keywords: Hillsboro Oregon Conservator's First and Final Accounting, conservatorship process, financial document, protected person, assets, management, financial matters. There are different types of Hillsboro Oregon Conservator's First and Final Accounting, which can include: 1. Initial Accounting: This is the first accounting report submitted by the conservator, typically within a specified time frame after their appointment. It outlines the financial situation of the protected person's estate at the beginning of the conservatorship. 2. Interim Accounting: In cases where the conservatorship process is prolonged or spans several years, interim accounting may be required. These accounting provide periodic updates on the management of the protected person's assets and finances, ensuring transparency and accountability. 3. Final Accounting: As the name suggests, the final accounting marks the culmination of the conservatorship process. It contains a detailed summary of all financial transactions and decisions made by the conservator during their tenure. The final accounting requires the conservator to present a comprehensive picture of the protected person's estate, including income, expenses, investments, debts, and any changes made during their role. 4. Court-Approved Accounting: This accounting is submitted to the court overseeing the conservatorship for review and approval. It must meet specific legal requirements and follow any guidelines or instructions provided by the court. 5. Distribution Accounting: In cases where the conservatorship is ending due to various reasons, such as the protected person's recovery or passing, a distribution accounting may be necessary. This accounting entails the distribution of the estate's assets in accordance with applicable laws, wills, or court orders. Overall, Hillsboro Oregon Conservator's First and Final Accounting, along with its various types, acts as a critical tool to ensure that the conservator acts in the best interest of the protected person. By incorporating relevant keywords and understanding the different types, individuals can gain a better understanding of the accounting process and its significance within the Hillsboro, Oregon conservatorship system.

Hillsboro Oregon Conservator's First and Final Accounting

Description

How to fill out Hillsboro Oregon Conservator's First And Final Accounting?

Locating verified templates specific to your local regulations can be difficult unless you use the US Legal Forms library. It’s an online pool of more than 85,000 legal forms for both personal and professional needs and any real-life situations. All the documents are properly grouped by area of usage and jurisdiction areas, so locating the Hillsboro Oregon Conservator's First and Final Accounting gets as quick and easy as ABC.

For everyone already familiar with our service and has used it before, obtaining the Hillsboro Oregon Conservator's First and Final Accounting takes just a few clicks. All you need to do is log in to your account, choose the document, and click Download to save it on your device. This process will take just a couple of more actions to complete for new users.

Follow the guidelines below to get started with the most extensive online form collection:

- Look at the Preview mode and form description. Make certain you’ve selected the right one that meets your requirements and fully corresponds to your local jurisdiction requirements.

- Search for another template, if needed. Once you see any inconsistency, utilize the Search tab above to obtain the correct one. If it suits you, move to the next step.

- Buy the document. Click on the Buy Now button and select the subscription plan you prefer. You should create an account to get access to the library’s resources.

- Make your purchase. Give your credit card details or use your PayPal account to pay for the service.

- Download the Hillsboro Oregon Conservator's First and Final Accounting. Save the template on your device to proceed with its completion and get access to it in the My Forms menu of your profile whenever you need it again.

Keeping paperwork neat and compliant with the law requirements has major importance. Take advantage of the US Legal Forms library to always have essential document templates for any demands just at your hand!