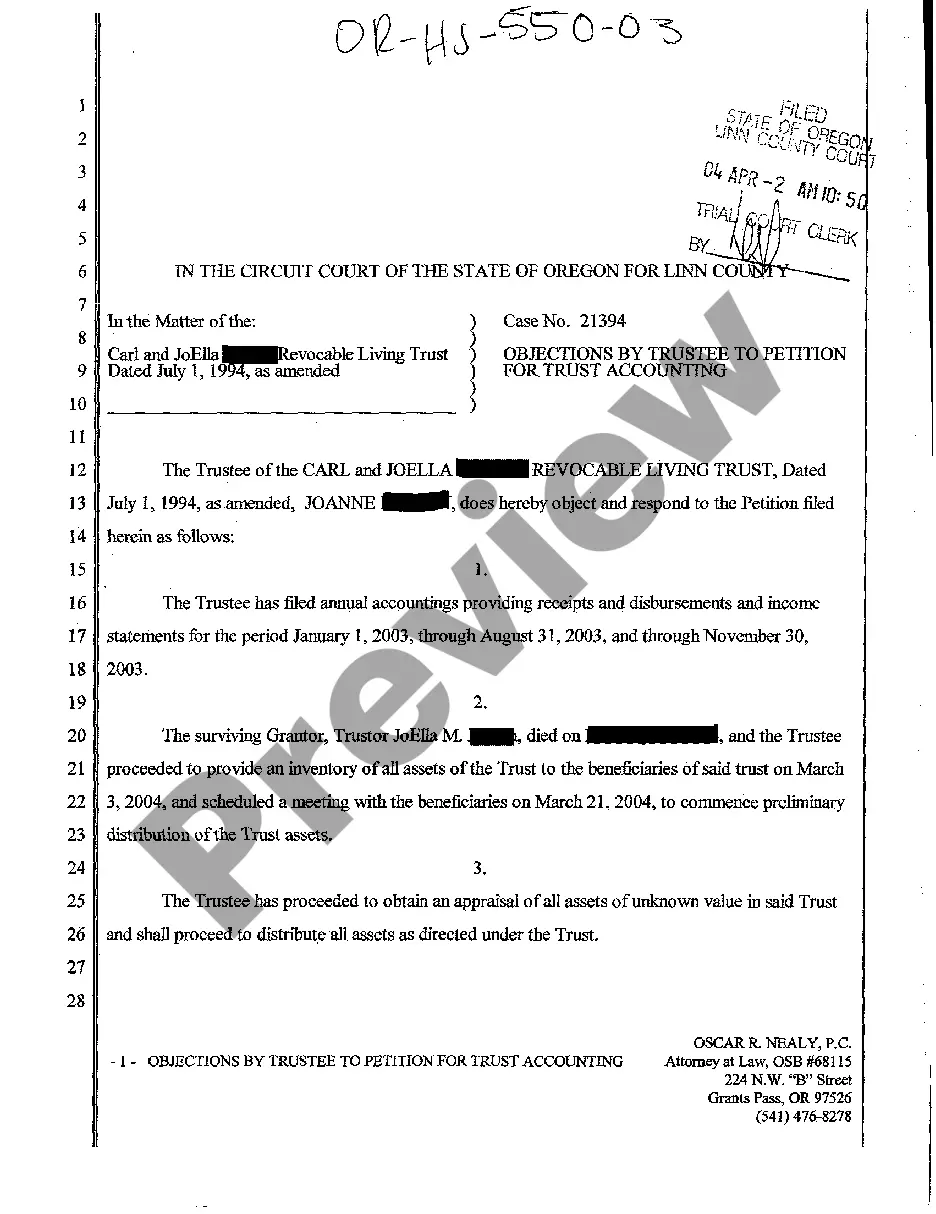

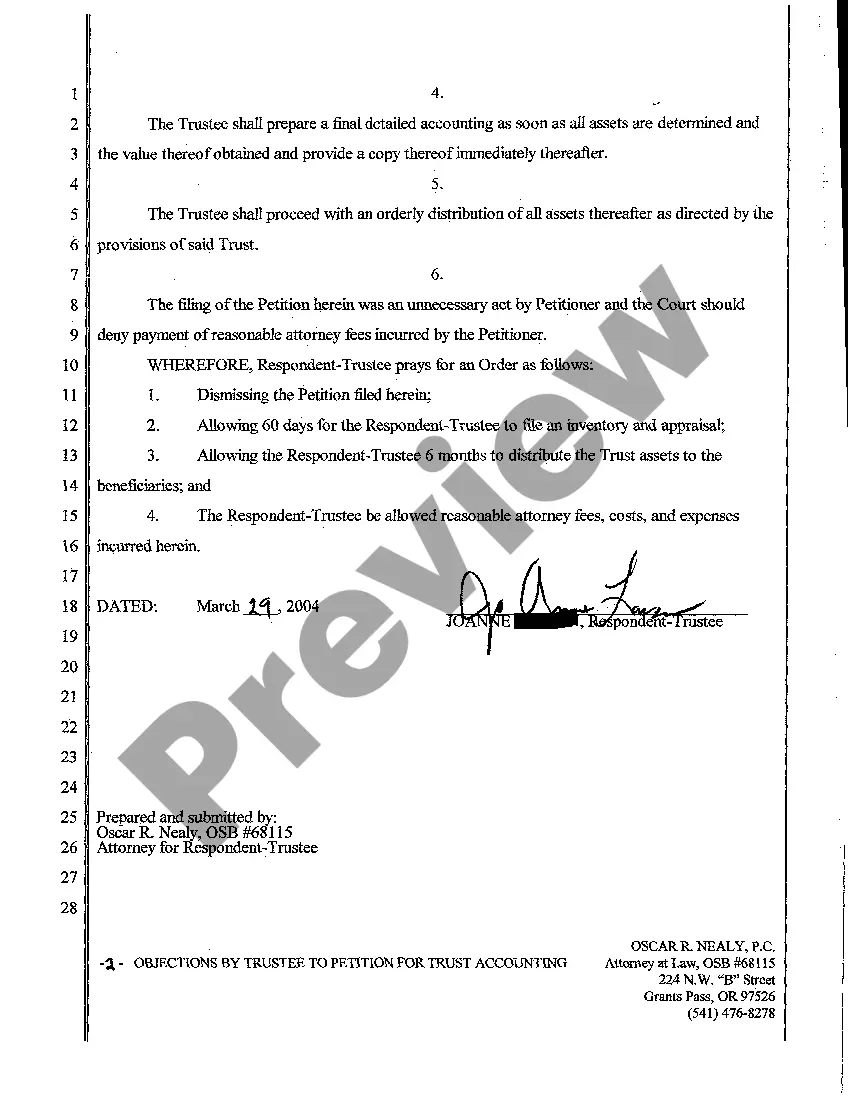

Title: Understanding Gresham Oregon Objections by Trustee to Petition for Trust Accounting: Types and Detailed Explanation Introduction: In Gresham, Oregon, objections by a trustee to a petition for trust accounting are possible in cases where a trustee disagrees with a request for a trust accounting or believes that the request is not supported by valid reasons. This article aims to provide a detailed description of Gresham Oregon objections by trustees to petitions for trust accounting, covering different types of objections and their implications. Keywords: — GreshamOregongo— - Objections by trustee — Petition for trusaccountingin— - Trustee objections — Trust accountinrequestes— - Valid reasons — Trustee's duties - Trustee's responsibilities Types of Gresham Oregon Objections by Trustee to Petition for Trust Accounting: 1. Lack of Substantial Reason: A trustee may object to a petition for trust accounting if they believe there is a lack of substantial reason to warrant accounting. In this case, the trustee may argue that the request does not provide sufficient grounds to justify the time, effort, and cost associated with producing a trust accounting report. 2. Untimeliness: Trustees may object to a petition for trust accounting on grounds of untimeliness. If the request does not align with the specific timelines outlined in the trust instrument or applicable state laws, the trustee may argue that the petition is premature or untimely, thereby objecting to its consideration. 3. Insufficient Beneficiary Interest: The trustee may object to a petition for trust accounting if they believe the beneficiary's interest in the trust is insufficient to warrant an accounting. This objection occurs when the trustee may argue that the cost of providing a trust account and the potential invasion of privacy outweigh the beneficiary's claim for accounting. 4. Prior Accounting or Disclosure: Trustees may object to a petition for trust accounting if they can demonstrate that a prior accounting or disclosure was previously provided to the beneficiaries. In this case, the trustee may argue that another accounting request is unnecessary or redundant, as adequate transparency has already been afforded to the beneficiaries. 5. Privacy and Confidentiality: Trustees may object to a petition for trust accounting by invoking concerns over privacy and confidentiality. They may argue that disclosing certain trust information would violate the privacy rights of beneficiaries or third parties, particularly if the information is not relevant to the case at hand. Conclusion: Gresham Oregon objections by trustees to petitions for trust accounting can arise due to various reasons, including lack of substantial reason, untimeliness, insufficient beneficiary interest, prior accounting or disclosure, and concerns over privacy and confidentiality. Understanding these objections requires careful consideration of the trustee's duties and responsibilities, as well as the specific circumstances of the trust arrangement.

Gresham Oregon Objections by Trustee to Petition for Trust Accounting

Description

How to fill out Gresham Oregon Objections By Trustee To Petition For Trust Accounting?

We always want to minimize or prevent legal issues when dealing with nuanced legal or financial affairs. To accomplish this, we sign up for attorney services that, as a rule, are extremely costly. However, not all legal issues are equally complex. Most of them can be taken care of by ourselves.

US Legal Forms is an online catalog of up-to-date DIY legal forms covering anything from wills and powers of attorney to articles of incorporation and petitions for dissolution. Our library helps you take your affairs into your own hands without the need of using services of a lawyer. We offer access to legal document templates that aren’t always publicly accessible. Our templates are state- and area-specific, which considerably facilitates the search process.

Benefit from US Legal Forms whenever you need to find and download the Gresham Oregon Objections by Trustee to Petition for Trust Accounting or any other document quickly and securely. Simply log in to your account and click the Get button next to it. If you happened to lose the document, you can always re-download it in the My Forms tab.

The process is just as easy if you’re new to the website! You can create your account within minutes.

- Make sure to check if the Gresham Oregon Objections by Trustee to Petition for Trust Accounting complies with the laws and regulations of your your state and area.

- Also, it’s imperative that you go through the form’s description (if provided), and if you notice any discrepancies with what you were looking for in the first place, search for a different template.

- Once you’ve ensured that the Gresham Oregon Objections by Trustee to Petition for Trust Accounting is proper for you, you can select the subscription plan and proceed to payment.

- Then you can download the document in any available format.

For more than 24 years of our existence, we’ve helped millions of people by offering ready to customize and up-to-date legal forms. Take advantage of US Legal Forms now to save time and resources!