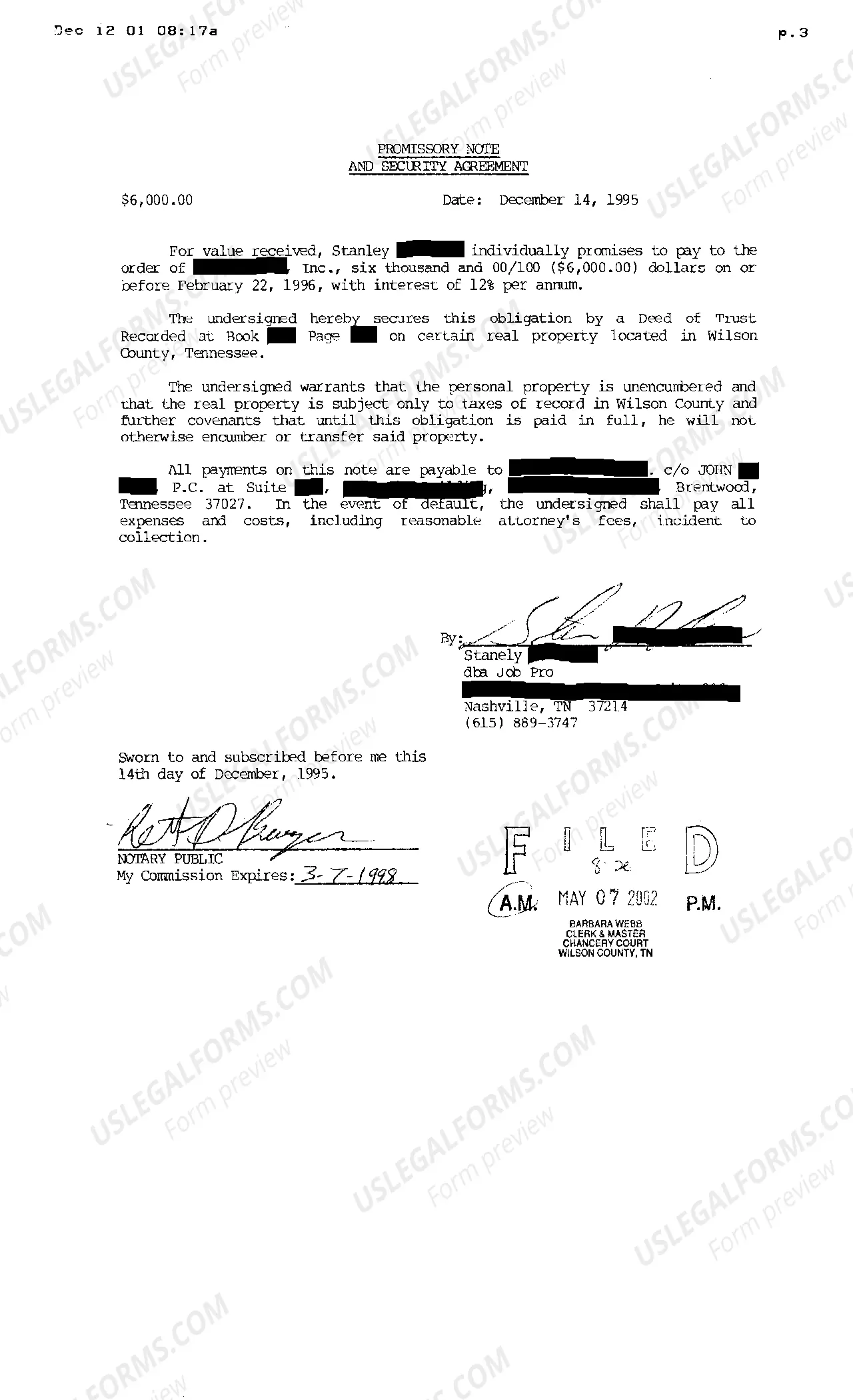

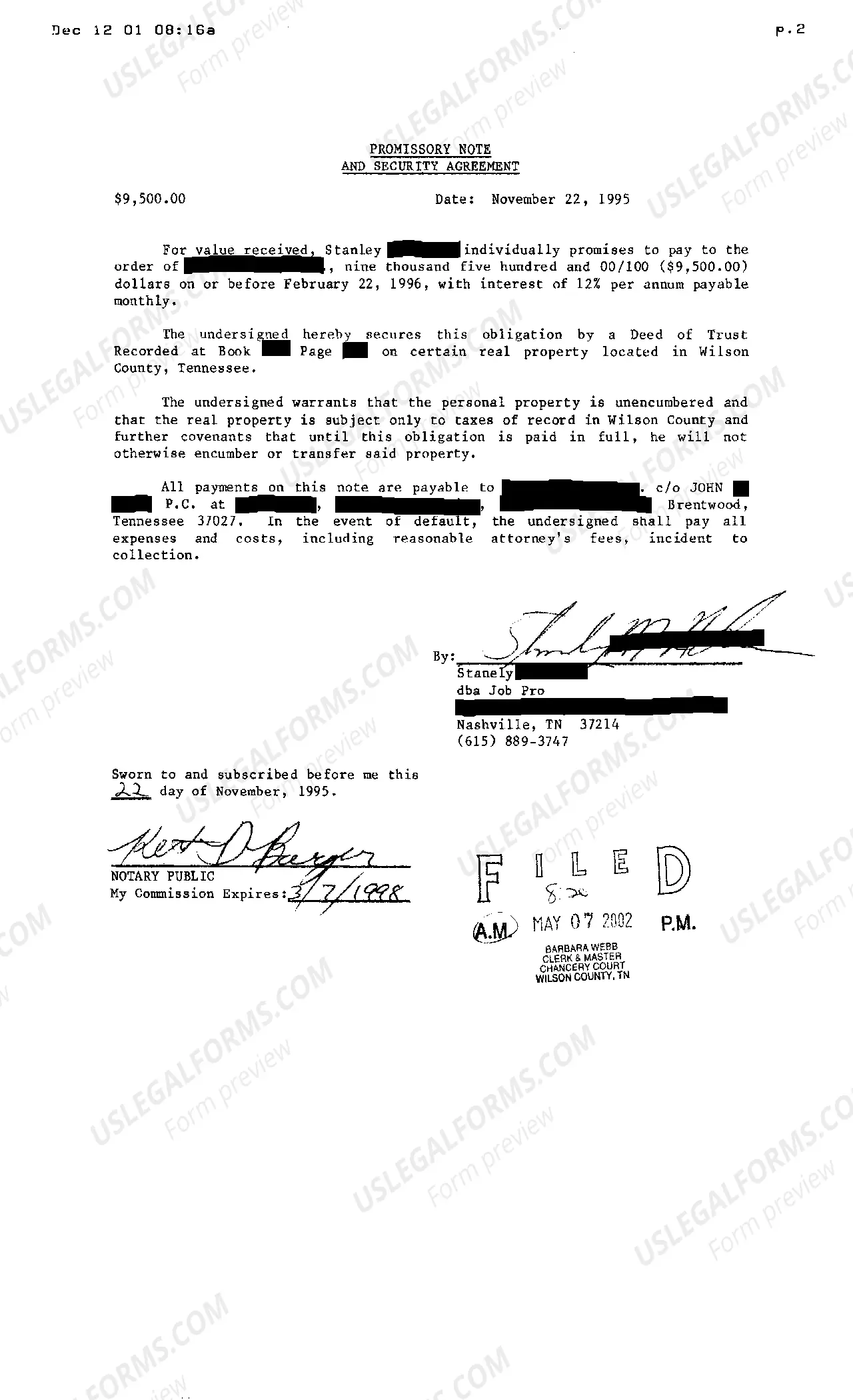

Title: Resolving Murfreesboro Tennessee Issues On Appeal To Set Aside Tax Sale Introduction: Murfreesboro, Tennessee, like any other city, faces certain issues related to tax sales. One such challenge involves disputes requiring an appeal to set aside a tax sale. This article provides a comprehensive overview of the Murfreesboro Tennessee issues on appeal to set aside tax sale, highlighting key aspects, legal considerations, and potential types of appeals. 1. Understanding Tax Sales in Murfreesboro, Tennessee: — Definition and purpose of tax sales: Tax sales are carried out to recover unpaid taxes from property owners. — Tax sale process in Murfreesboro: Outlines the typical steps involved in a tax sale, including notice requirements, bidding process, and redemption period. 2. Common Issues Identified in Tax Sales: — Inadequate notice: Discusses instances where property owners may claim lack of proper notice regarding the tax sale. — Failure to comply with legal requirements: Highlights scenarios where the tax sale process fails to meet statutory obligations, potentially leading to an appeal. — Procedural errors: Examines situations where errors or omissions in the tax sale process can be grounds for an appeal. 3. Appealing a Tax Sale in Murfreesboro, Tennessee: — Initiating the appeal process: Explores the steps property owners must take to appeal a tax sale. — Legal grounds for an appeal: Discusses the different legal arguments that can be presented to set aside a tax sale, such as insufficient notice, improper procedures, or defects in the sale process. — Filing deadlines and requirements: Provides information on the specific deadlines and documentation necessary for filing an appeal. 4. Types of Appeals to Set Aside Tax Sales: While the specific types of appeals depend on individual circumstances, some common appeal types in Murfreesboro include: — Appeal based on lack of notice: Property owners argue that proper notice was not provided as required by law. — Appeal due to procedural errors: Challenges the validity of the tax sale based on errors made during the process. — Appeal based on unconstitutional action: Alleges that the tax sale violated constitutional rights. — Appeal citing excessive tax lien: Property owners claim that the amount owed was mistakenly inflated. 5. Legal Considerations and Possible Outcomes: — Role of the court: Explains how the court evaluates tax sale appeals and decides whether to set aside the sale. — Evidence and burden of proof: Describes the evidence required to support an appeal and the property owner's burden of proving that a tax sale should be set aside. — Potential outcomes: Discusses the possible results of an appeal, such as setting aside the sale, retroactively reinstating ownership, or compensating the property owner for damages. Conclusion: Resolving Murfreesboro Tennessee issues on appeal to set aside tax sale requires a clear understanding of the legal framework, specific appeal types, and potential outcomes. It is crucial for property owners to navigate the process with legal expertise to ensure a fair resolution and protect their rights in such cases.

Murfreesboro Tennessee Issues On Appeal To Set Aside Tax Sale

Description

How to fill out Murfreesboro Tennessee Issues On Appeal To Set Aside Tax Sale?

Make use of the US Legal Forms and obtain instant access to any form sample you need. Our useful website with a huge number of document templates simplifies the way to find and get almost any document sample you will need. You are able to save, fill, and sign the Murfreesboro Tennessee Issues On Appeal To Set Aside Tax Sale in a couple of minutes instead of surfing the Net for many hours seeking an appropriate template.

Utilizing our library is a wonderful way to increase the safety of your record submissions. Our professional legal professionals regularly check all the records to make sure that the forms are relevant for a particular region and compliant with new acts and regulations.

How can you get the Murfreesboro Tennessee Issues On Appeal To Set Aside Tax Sale? If you already have a subscription, just log in to the account. The Download button will be enabled on all the documents you look at. Moreover, you can get all the earlier saved documents in the My Forms menu.

If you haven’t registered a profile yet, follow the instructions listed below:

- Open the page with the form you require. Make certain that it is the template you were seeking: check its title and description, and take take advantage of the Preview option if it is available. Otherwise, utilize the Search field to look for the appropriate one.

- Launch the downloading process. Click Buy Now and choose the pricing plan you prefer. Then, sign up for an account and process your order with a credit card or PayPal.

- Save the file. Choose the format to obtain the Murfreesboro Tennessee Issues On Appeal To Set Aside Tax Sale and edit and fill, or sign it for your needs.

US Legal Forms is probably the most extensive and reliable document libraries on the internet. We are always ready to assist you in any legal case, even if it is just downloading the Murfreesboro Tennessee Issues On Appeal To Set Aside Tax Sale.

Feel free to make the most of our form catalog and make your document experience as efficient as possible!