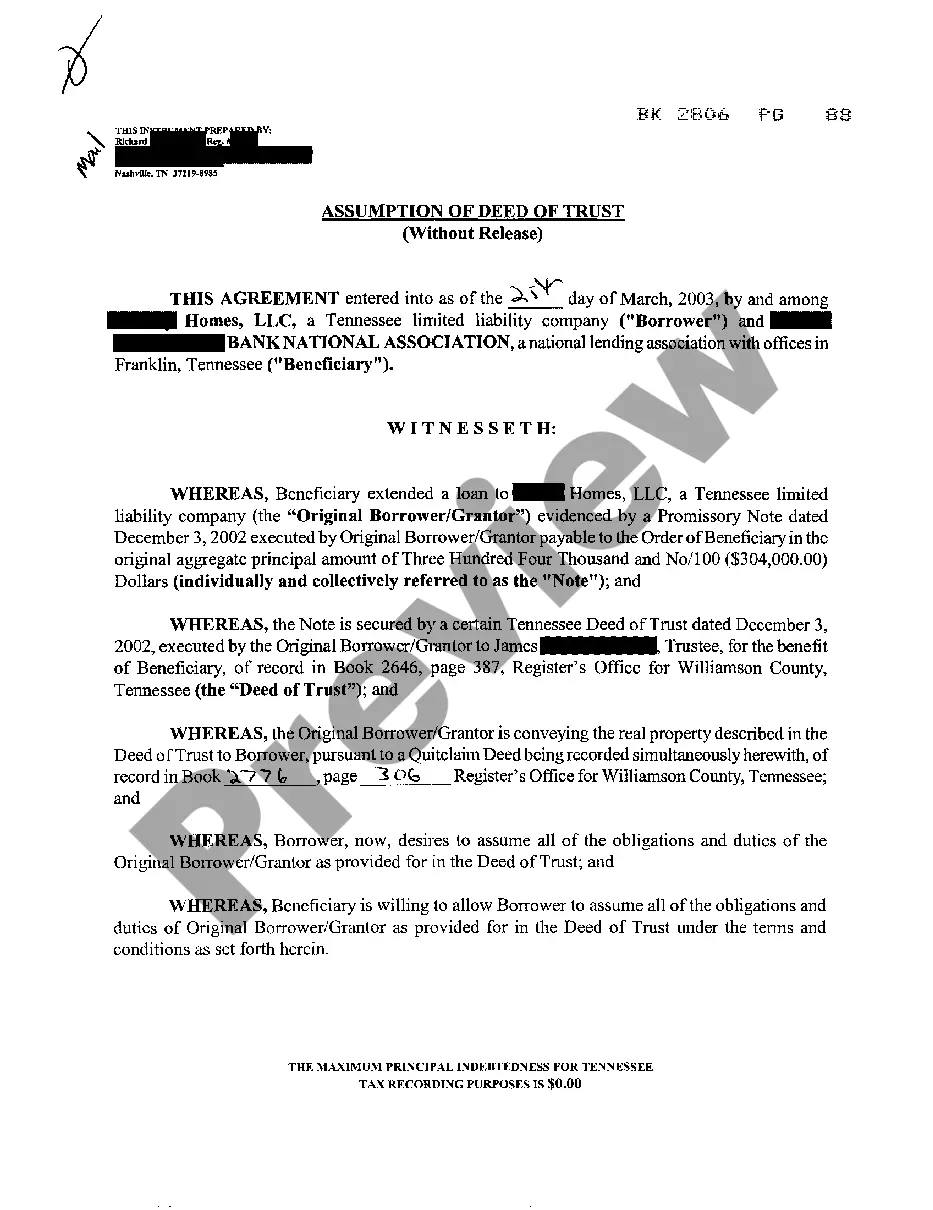

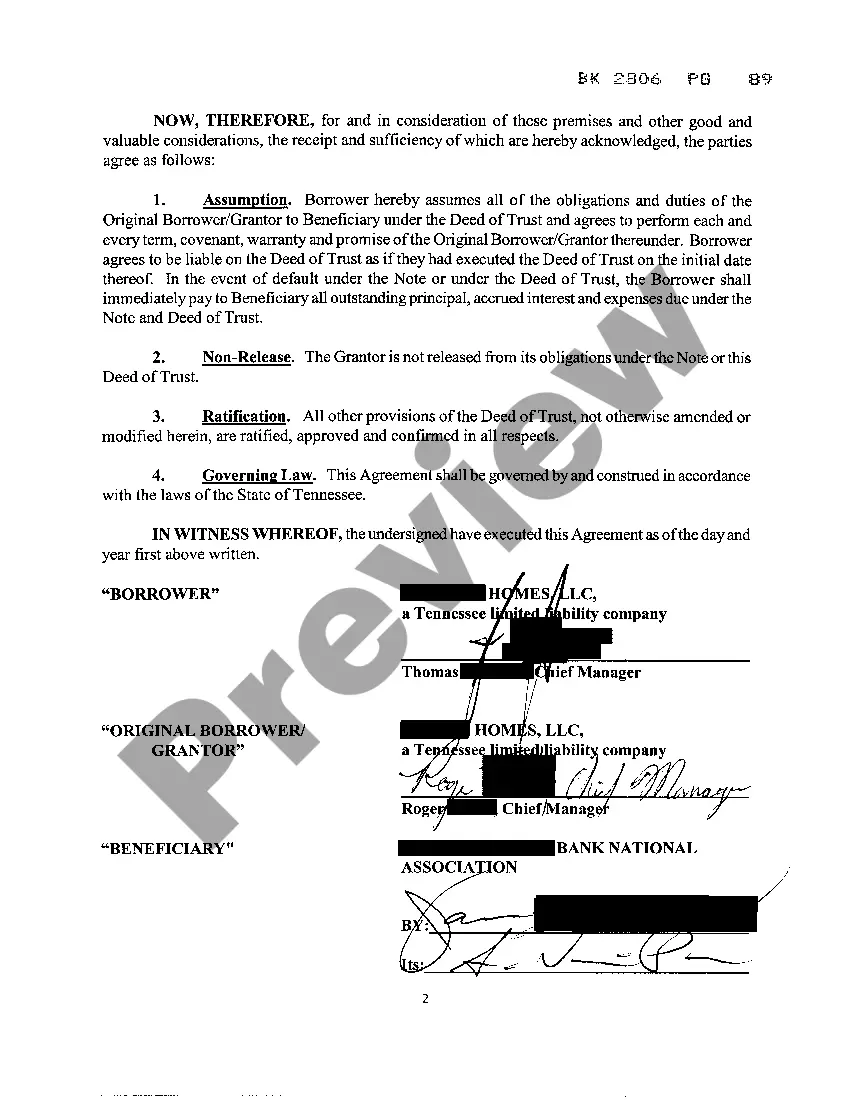

The Memphis Tennessee Assumption of Deed of Trust refers to a legal process in which a borrower transfers their mortgage obligations to another party, known as the assumption or the new borrower. This arrangement typically occurs when the original borrower wants to sell the property but wishes to avoid paying off the existing mortgage. The assumption of deed of trust is an agreement signed by the original borrower, the assumption, and the lender. It outlines the terms and conditions under which the assumption takes over the mortgage, including their obligations to make regular payments and abide by the original loan terms. There are different types of Memphis Tennessee Assumption of Deed of Trust, which vary depending on the specific circumstances and parties involved. Some common types include: 1. General Assumption: In this type, the assumption takes over the entire mortgage and becomes responsible for all the remaining payments and obligations specified in the original loan agreement. 2. Subject to Assumption: Here, the assumption takes over the mortgage payments but does not become personally liable for the loan. The original borrower remains legally responsible for the loan, and any default by the assumption could still impact the original borrower's creditworthiness. 3. Novation Assumption: This type involves the cancellation of the original loan and the creation of a new loan agreement between the lender and the assumption. The assumption takes over the property and assumes a new mortgage with potentially revised terms. It's important to note that the Memphis Tennessee Assumption of Deed of Trust must comply with the laws and regulations specific to the state of Tennessee, including any additional requirements set by the local Memphis authorities. The details and requirements may vary depending on the lender and the specifics of the original loan. The purpose of the Memphis Tennessee Assumption of Deed of Trust is to facilitate the transfer of ownership and financial responsibility for a property between parties, while ensuring that the lender's interests are protected. It can provide a solution for borrowers who are unable or unwilling to pay off their mortgage in full before selling their property, while also allowing a new buyer to avoid the process of securing a new loan.

Memphis Tennessee Assumption of Deed of Trust

Description

How to fill out Memphis Tennessee Assumption Of Deed Of Trust?

Getting verified templates specific to your local regulations can be difficult unless you use the US Legal Forms library. It’s an online collection of more than 85,000 legal forms for both individual and professional needs and any real-life scenarios. All the documents are properly grouped by area of usage and jurisdiction areas, so searching for the Memphis Tennessee Assumption of Deed of Trust gets as quick and easy as ABC.

For everyone already familiar with our service and has used it before, obtaining the Memphis Tennessee Assumption of Deed of Trust takes just a few clicks. All you need to do is log in to your account, select the document, and click Download to save it on your device. The process will take just a few additional steps to make for new users.

Adhere to the guidelines below to get started with the most extensive online form catalogue:

- Check the Preview mode and form description. Make sure you’ve picked the correct one that meets your requirements and fully corresponds to your local jurisdiction requirements.

- Search for another template, if needed. Once you see any inconsistency, use the Search tab above to find the right one. If it suits you, move to the next step.

- Purchase the document. Click on the Buy Now button and choose the subscription plan you prefer. You should register an account to get access to the library’s resources.

- Make your purchase. Give your credit card details or use your PayPal account to pay for the subscription.

- Download the Memphis Tennessee Assumption of Deed of Trust. Save the template on your device to proceed with its completion and obtain access to it in the My Forms menu of your profile anytime you need it again.

Keeping paperwork neat and compliant with the law requirements has significant importance. Take advantage of the US Legal Forms library to always have essential document templates for any demands just at your hand!