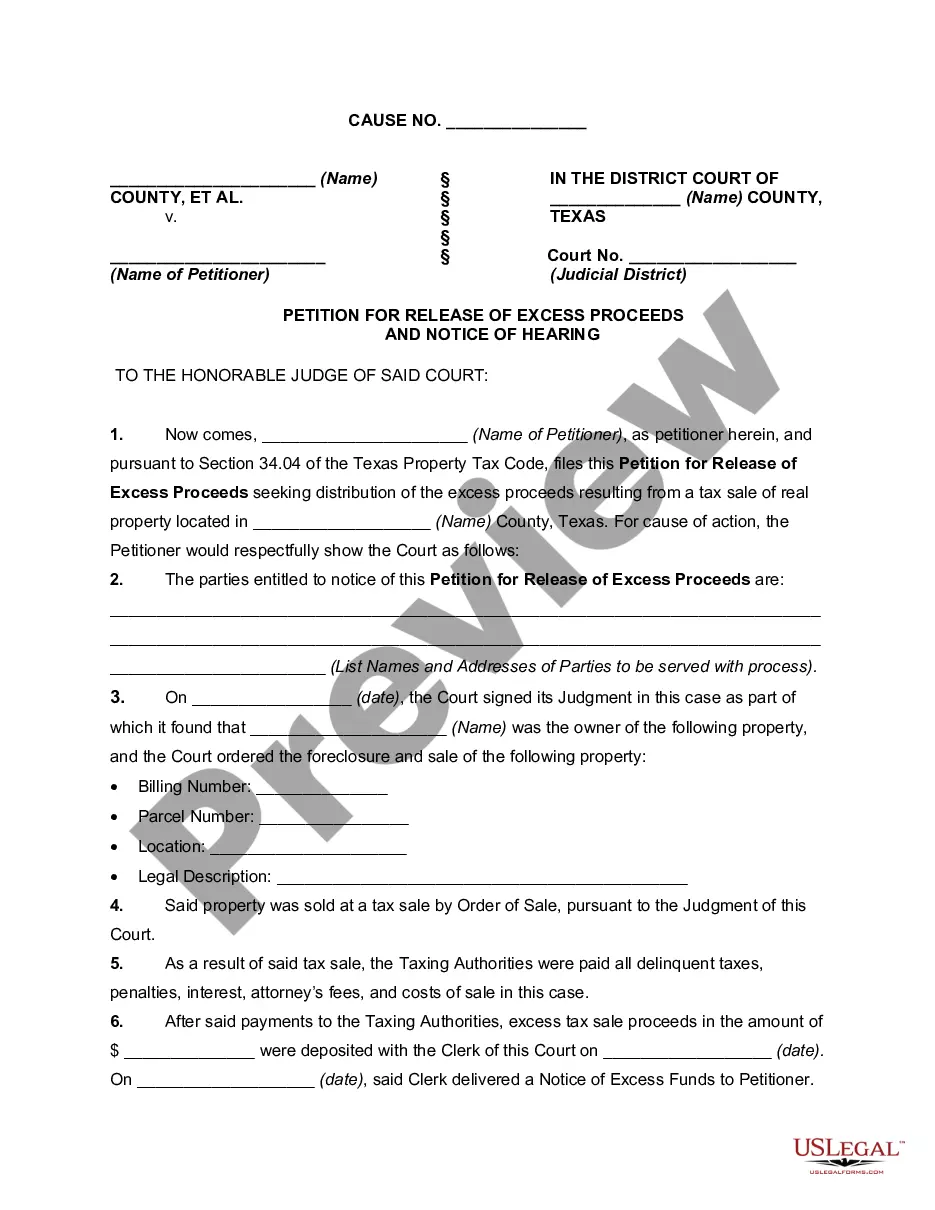

Sec. 34.04 of the Texas Tax Code provides in part as follows:

(a) A person, including a taxing unit, may file a petition in the court that ordered the seizure or sale setting forth a claim to the excess proceeds. The petition must be filed before the second anniversary of the date of the sale of the property. The petition is not required to be filed as an original suit separate from the underlying suit for seizure of the property or foreclosure of a tax lien on the property but may be filed under the cause number of the underlying suit.

(b) A copy of the petition shall be served, in the manner prescribed by Rule 21a, Texas Rules of Civil Procedure, as amended, or that rule's successor, on all parties to the underlying action not later than the 20th day before the date set for a hearing on the petition.

(c) At the hearing the court shall order that the proceeds be paid according to the following priorities to each party that establishes its claim to the proceeds:

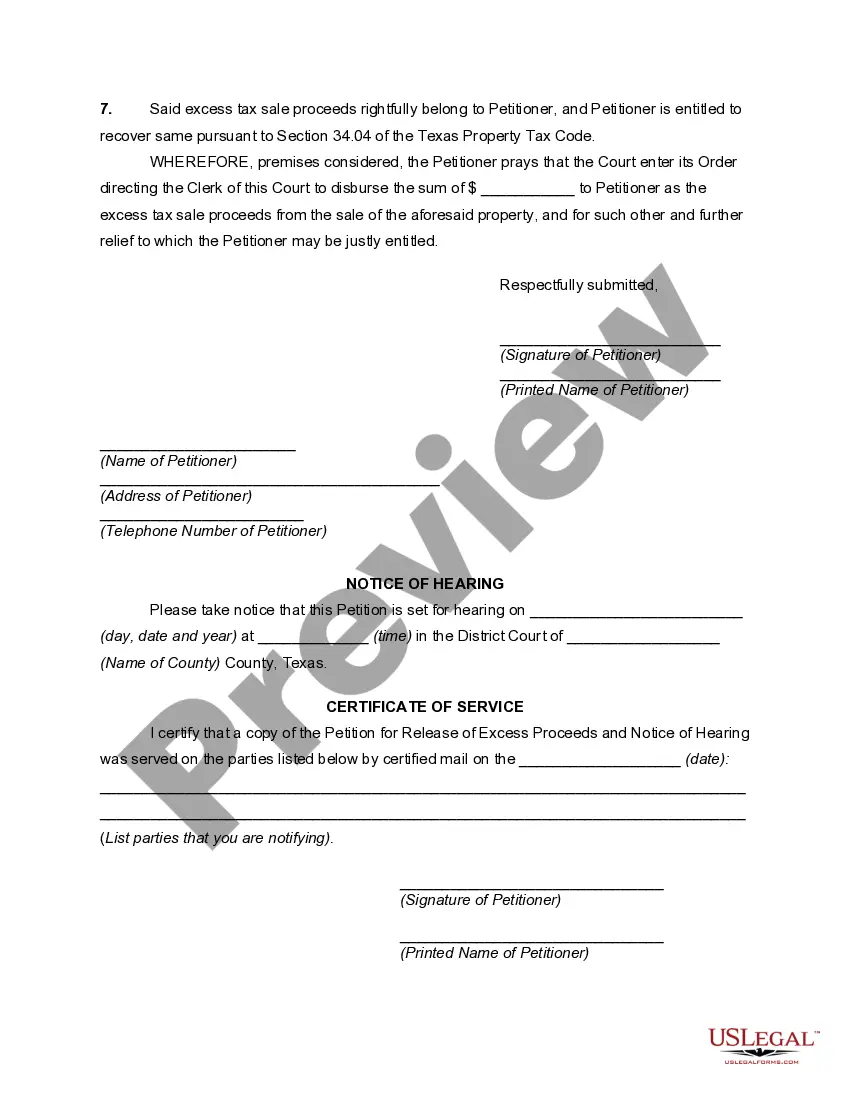

(1) to the tax sale purchaser if the tax sale has been adjudged to be void and the purchaser has prevailed in an action against the taxing units under Section 34.07(d) by final judgment;

(2) to a taxing unit for any taxes, penalties, or interest that have become due or delinquent on the subject property subsequent to the date of the judgment or that were omitted from the judgment by accident or mistake;

(3) to any other lienholder, consensual or otherwise, for the amount due under a lien, in accordance with the priorities established by applicable law;

(4) to a taxing unit for any unpaid taxes, penalties, interest, or other amounts adjudged due under the judgment that were not satisfied from the proceeds from the tax sale; and

(5) to each former owner of the property, as the interest of each may appear.

(d) Interest or costs may not be allowed under this section.

(e) An order under this section is appealable.

Laredo Texas Petition for Release of Excess Proceeds and Notice of Hearing

Description

How to fill out Laredo Texas Petition For Release Of Excess Proceeds And Notice Of Hearing?

If you are looking for a valid form template, it’s difficult to find a better service than the US Legal Forms website – one of the most extensive online libraries. Here you can find thousands of templates for business and individual purposes by types and states, or keywords. With the high-quality search option, discovering the newest Laredo Texas Petition for Release of Excess Proceeds and Notice of Hearing is as easy as 1-2-3. Moreover, the relevance of every record is proved by a group of skilled attorneys that regularly check the templates on our website and update them based on the latest state and county demands.

If you already know about our system and have a registered account, all you need to receive the Laredo Texas Petition for Release of Excess Proceeds and Notice of Hearing is to log in to your user profile and click the Download button.

If you use US Legal Forms the very first time, just follow the instructions below:

- Make sure you have discovered the form you need. Check its explanation and utilize the Preview function to check its content. If it doesn’t suit your needs, use the Search option at the top of the screen to discover the needed file.

- Confirm your selection. Click the Buy now button. After that, pick the preferred pricing plan and provide credentials to sign up for an account.

- Process the purchase. Use your credit card or PayPal account to finish the registration procedure.

- Obtain the form. Choose the file format and save it on your device.

- Make changes. Fill out, modify, print, and sign the obtained Laredo Texas Petition for Release of Excess Proceeds and Notice of Hearing.

Every form you save in your user profile does not have an expiration date and is yours forever. You always have the ability to gain access to them using the My Forms menu, so if you need to have an additional version for editing or printing, you may come back and export it once more at any time.

Make use of the US Legal Forms extensive collection to get access to the Laredo Texas Petition for Release of Excess Proceeds and Notice of Hearing you were looking for and thousands of other professional and state-specific templates in a single place!