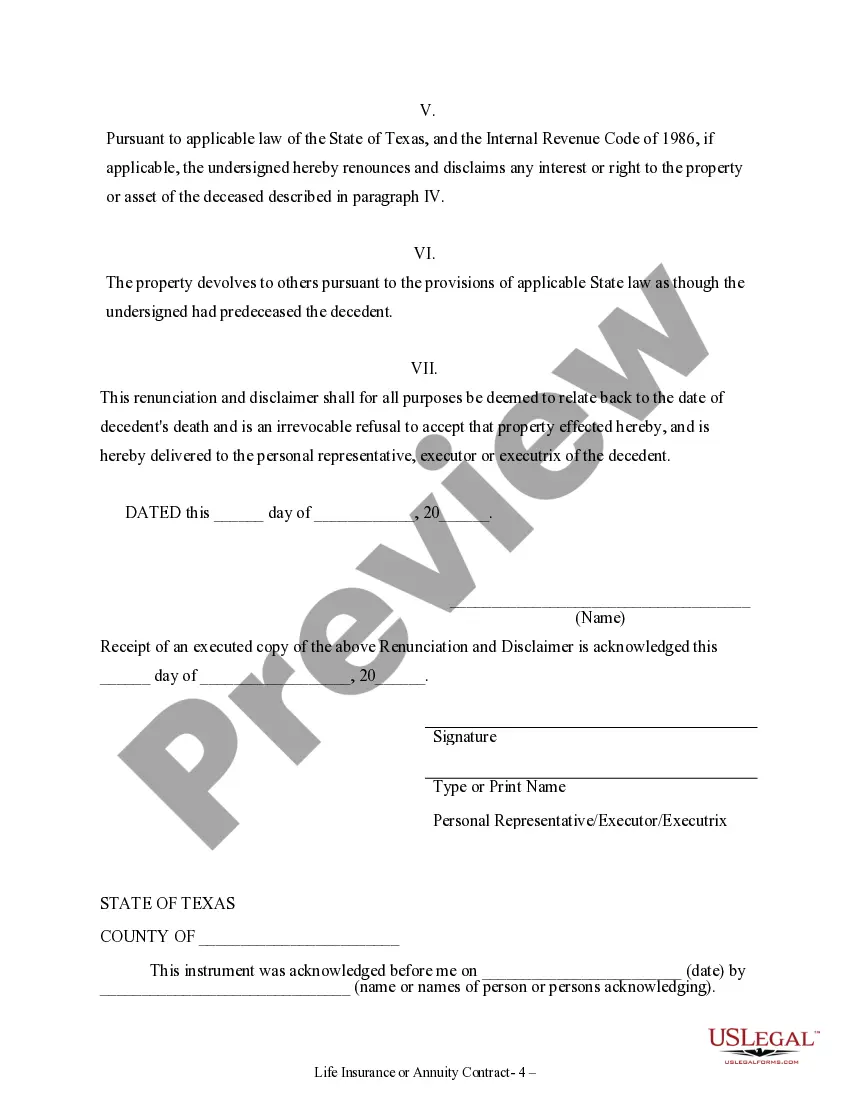

This form is a Renunciation and Disclaimer of Life Insurance or Annuity Contract proceeds, where the beneficiary gained an interest in the proceeds upon the death of the decedent, but, pursuant to the Texas Statutes, Chapter II, has decided to disclaim his/her interest in the proceeds. The beneficiary attests that he/she will file the disclaimer no later than nine months after the death of the decedent in order to secure the validity of the disclaimer. The form also contains a state specific acknowledgment and a certificate to verify the delivery of the document.

Title: Understanding the Dallas Texas Renunciation and Disclaimer of Property from Life Insurance or Annuity Contract Introduction: In Dallas, Texas, individuals have the option to renounce or disclaim their rights to property from life insurance or annuity contracts. This legal process allows beneficiaries or potential recipients to forfeit their claim and avoid any associated liabilities. Understanding the different types of renunciation and disclaimer options available can be crucial for ensuring the proper handling of such assets. This article provides a comprehensive description of the Dallas Texas Renunciation and Disclaimer of Property from Life Insurance or Annuity Contract, highlighting key keywords such as renunciation, disclaimer, property, life insurance, and annuity contract. 1. Renunciation and Disclaimer Explained: The renunciation and disclaimer process involves voluntarily relinquishing one's rights to property inherited from a life insurance or annuity contract. Renunciation is typically executed by beneficiaries who wish to decline their interest in the assets, thereby transferring entitlement to the next eligible individual. A disclaimer, on the other hand, is often utilized when a recipient wants to refuse inheritance altogether, redirecting the property to contingent beneficiaries or allowing it to pass through intestate succession. 2. Dallas Texas Renunciation Process: When renouncing property in Dallas, Texas, the renouncing party must follow certain legal requirements. Initially, a written statement explicitly expressing renunciation intentions must be provided to the concerned entity, such as the insurance company or annuity provider. This document should include all relevant details, such as the renouncing party's name, contact information, and a clear declaration of renouncing rights. 3. Dallas Texas Disclaimer Process: To disclaim property from a life insurance or annuity contract in Dallas, Texas, a disclaimer must be prepared in writing and delivered to the appropriate parties within a specified timeframe. The disclaimer should encompass crucial information such as the disclaiming party's identification, details of the property being disclaimed, and an explicit statement expressing the disclaimer of any interest in the property. 4. Different Types of Renunciation/Disclaimer Scenarios: a) Partial Renunciation/Disclaimer: In certain cases, beneficiaries or recipients may choose to renounce or disclaim only a portion of their inheritance. This option enables them to retain a designated fraction of the assets while relinquishing the remaining portion. b) Conditional Renunciation/Disclaimer: Conditional renunciation or disclaimer refers to situations where the act is executed under specific circumstances. For example, a beneficiary may renounce or disclaim their inheritance if certain conditions or requirements are not met. 5. Implications of Renunciation/Disclaimer: Renunciation or disclaimer of property from a life insurance or annuity contract in Dallas, Texas, can have important legal and financial implications. It is crucial for individuals considering such actions to consult with an attorney or financial advisor to fully understand the consequences, including potential tax implications, for both themselves and any subsequent beneficiaries. Conclusion: The Dallas Texas Renunciation and Disclaimer of Property from Life Insurance or Annuity Contract provide individuals in Dallas with the option to decline or forfeit their entitlement to inherited assets. By understanding the various processes, types of renunciation or disclaimer scenarios, and associated implications, individuals can make well-informed decisions regarding the handling of life insurance or annuity contract proceeds. Seeking professional advice is highly recommended ensuring compliance with local laws and fulfill all necessary legal obligations.Title: Understanding the Dallas Texas Renunciation and Disclaimer of Property from Life Insurance or Annuity Contract Introduction: In Dallas, Texas, individuals have the option to renounce or disclaim their rights to property from life insurance or annuity contracts. This legal process allows beneficiaries or potential recipients to forfeit their claim and avoid any associated liabilities. Understanding the different types of renunciation and disclaimer options available can be crucial for ensuring the proper handling of such assets. This article provides a comprehensive description of the Dallas Texas Renunciation and Disclaimer of Property from Life Insurance or Annuity Contract, highlighting key keywords such as renunciation, disclaimer, property, life insurance, and annuity contract. 1. Renunciation and Disclaimer Explained: The renunciation and disclaimer process involves voluntarily relinquishing one's rights to property inherited from a life insurance or annuity contract. Renunciation is typically executed by beneficiaries who wish to decline their interest in the assets, thereby transferring entitlement to the next eligible individual. A disclaimer, on the other hand, is often utilized when a recipient wants to refuse inheritance altogether, redirecting the property to contingent beneficiaries or allowing it to pass through intestate succession. 2. Dallas Texas Renunciation Process: When renouncing property in Dallas, Texas, the renouncing party must follow certain legal requirements. Initially, a written statement explicitly expressing renunciation intentions must be provided to the concerned entity, such as the insurance company or annuity provider. This document should include all relevant details, such as the renouncing party's name, contact information, and a clear declaration of renouncing rights. 3. Dallas Texas Disclaimer Process: To disclaim property from a life insurance or annuity contract in Dallas, Texas, a disclaimer must be prepared in writing and delivered to the appropriate parties within a specified timeframe. The disclaimer should encompass crucial information such as the disclaiming party's identification, details of the property being disclaimed, and an explicit statement expressing the disclaimer of any interest in the property. 4. Different Types of Renunciation/Disclaimer Scenarios: a) Partial Renunciation/Disclaimer: In certain cases, beneficiaries or recipients may choose to renounce or disclaim only a portion of their inheritance. This option enables them to retain a designated fraction of the assets while relinquishing the remaining portion. b) Conditional Renunciation/Disclaimer: Conditional renunciation or disclaimer refers to situations where the act is executed under specific circumstances. For example, a beneficiary may renounce or disclaim their inheritance if certain conditions or requirements are not met. 5. Implications of Renunciation/Disclaimer: Renunciation or disclaimer of property from a life insurance or annuity contract in Dallas, Texas, can have important legal and financial implications. It is crucial for individuals considering such actions to consult with an attorney or financial advisor to fully understand the consequences, including potential tax implications, for both themselves and any subsequent beneficiaries. Conclusion: The Dallas Texas Renunciation and Disclaimer of Property from Life Insurance or Annuity Contract provide individuals in Dallas with the option to decline or forfeit their entitlement to inherited assets. By understanding the various processes, types of renunciation or disclaimer scenarios, and associated implications, individuals can make well-informed decisions regarding the handling of life insurance or annuity contract proceeds. Seeking professional advice is highly recommended ensuring compliance with local laws and fulfill all necessary legal obligations.