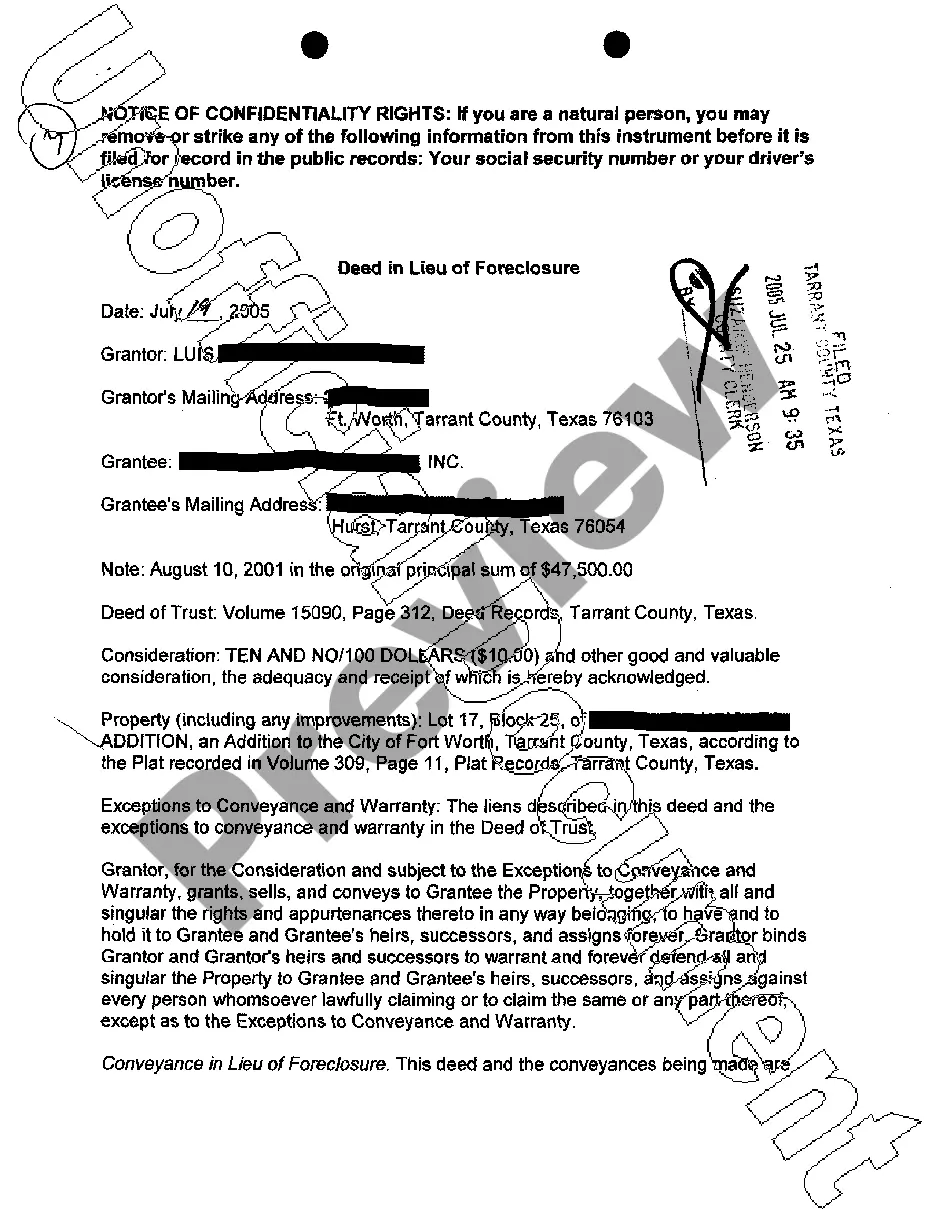

This detailed sample Deed in Lieu of Foreclosure complies with Texas law. Adapt the language to fit your facts and circumstances. Available in Word and Rich Text formats.

Harris Texas Deed in Lieu of Foreclosure

Category:

State:

Texas

County:

Harris

Control #:

TX-1046

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Texas Deed In Lieu Of Foreclosure?

Are you in search of a reliable and cost-effective provider of legal forms to acquire the Harris Texas Deed in Lieu of Foreclosure? US Legal Forms is your ideal choice.

Whether you require a simple contract to establish guidelines for living together with your partner, or a bundle of documents to facilitate your separation or divorce through the court, we've got you covered. Our platform offers over 85,000 current legal document templates for personal and business purposes. All templates that we provide access to are not generic and are tailored to meet the requirements of specific states and counties.

To obtain the form, you must Log In to your account, find the necessary form, and click the Download button next to it. Please remember that you can retrieve your previously bought document templates at any time in the My documents section.

Is this your first time visiting our site? No problem. You can set up an account in just a few minutes, but before you do that, make sure to follow these steps.

Now, you can create your account. Afterward, select a subscription plan and proceed with the payment. Once payment is completed, download the Harris Texas Deed in Lieu of Foreclosure in any format that is available. You can revisit the website whenever you want and redownload the form without incurring any additional fees.

Acquiring current legal forms has never been simpler. Try US Legal Forms today and stop wasting hours researching legal documents online.

- Verify that the Harris Texas Deed in Lieu of Foreclosure is compliant with the laws of your state and locality.

- Review the form's specifics (if available) to understand who and what the form is designed for.

- Conduct another search in case the form does not fit your legal needs.

Form popularity

FAQ

Processing a Harris Texas deed in lieu of foreclosure involves several steps that both homeowners and lenders should follow. First, the homeowner should contact their lender to express interest in executing a deed in lieu, as this initiates the conversation. Next, prepare the necessary documentation to transfer the property title, which may include financial disclosures and proof of ownership. Finally, complete the deed transfer by signing the document in the presence of a notary, and ensure that the lender records it to finalize the process.

The time it takes to record a deed in Texas can vary, but typically, it should be completed within a few business days. When you file your deed with the county clerk, they process it promptly. If you're dealing with a Harris Texas Deed in Lieu of Foreclosure, US Legal Forms can provide guidance on the necessary documentation and help ensure your deed is recorded correctly and efficiently.

In Harris County, you may obtain the deed to your house by accessing records online or by visiting the county clerk’s office. Your deed should be on file with them, reflecting all legal ownership. US Legal Forms can help streamline this process, especially if you’re navigating through a Harris Texas Deed in Lieu of Foreclosure. Their tools can assist you in understanding all necessary steps.

To obtain a copy of your property deed in Harris County, you can visit the Harris County Appraisal District website or contact their office directly. They maintain records of property deeds that are accessible to the public. Alternatively, you can use services like US Legal Forms, which can guide you in acquiring a Harris Texas Deed in Lieu of Foreclosure. This option simplifies the process and ensures you have the most accurate documentation.

Lenders often prefer a Harris Texas Deed in Lieu of Foreclosure because it is less costly and time-consuming than the foreclosure process. A deed in lieu typically results in a quicker resolution, reducing administrative resources and expenses. This option also helps maintain property values, which can be beneficial for lenders in a competitive market.

Lenders may accept a Harris Texas Deed in Lieu of Foreclosure because it minimizes the costs and time associated with foreclosures. Accepting a deed in lieu allows them to recover their investment more quickly without going through a lengthy legal process. Furthermore, lenders can avoid the costs of maintaining the property during the foreclosure process.

Yes, you can buy a house after a Harris Texas Deed in Lieu of Foreclosure, but there are important waiting periods to consider. Generally, many lenders require a waiting period ranging from two to four years before you can qualify for a new mortgage. Preparing your finances and improving your credit score during this period is essential for a smoother home-buying process.

A specific disadvantage of a Harris Texas Deed in Lieu of Foreclosure is that it requires lender approval. Not all lenders accept this option, which can limit your choices. Furthermore, a deed in lieu may not provide the same level of mortgage debt relief compared to a foreclosure, making it essential to assess your long-term financial goals.

Despite its benefits, one disadvantage of a Harris Texas Deed in Lieu of Foreclosure is that it may have tax implications. Homeowners could be responsible for paying taxes on any canceled debt. Additionally, a deed in lieu won’t eliminate all the obligations associated with your mortgage, especially if there are second liens involved.

When considering Harris Texas Deed in Lieu of Foreclosure, many people wonder if one option is worse than the other. Generally, foreclosure can appear worse on your credit report compared to a completed deed in lieu. A deed in lieu may allow for a faster resolution and can involve less stress for homeowners compared to the lengthy foreclosure process.