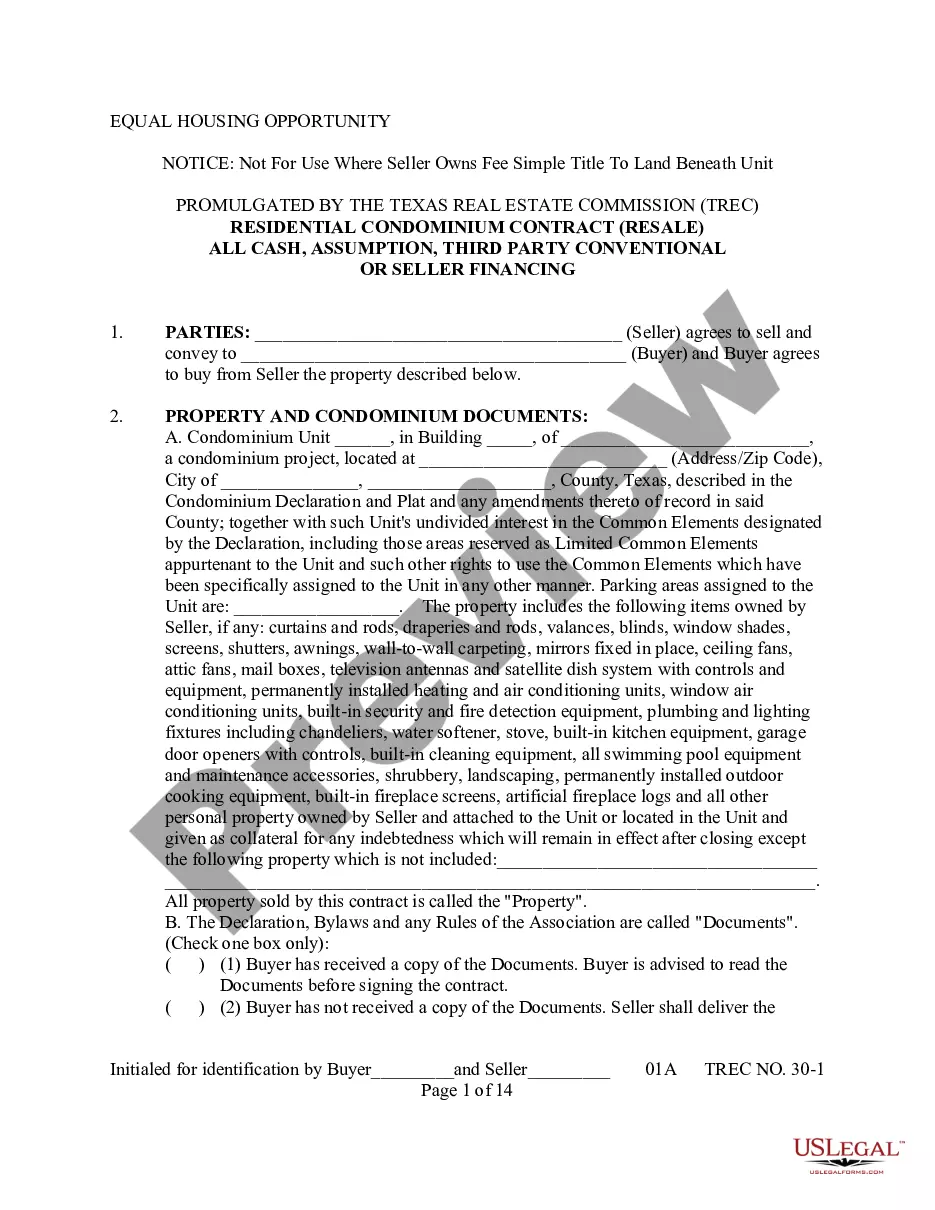

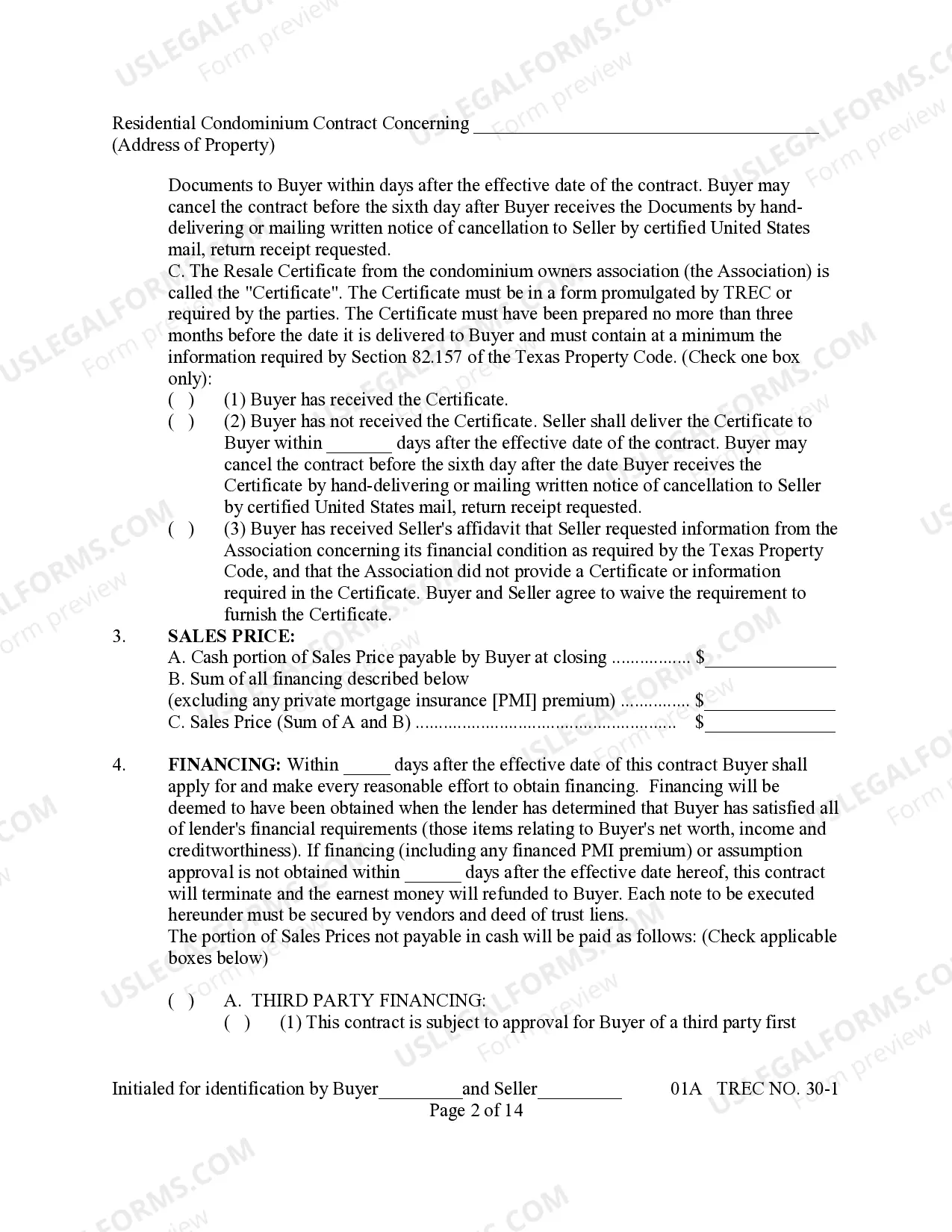

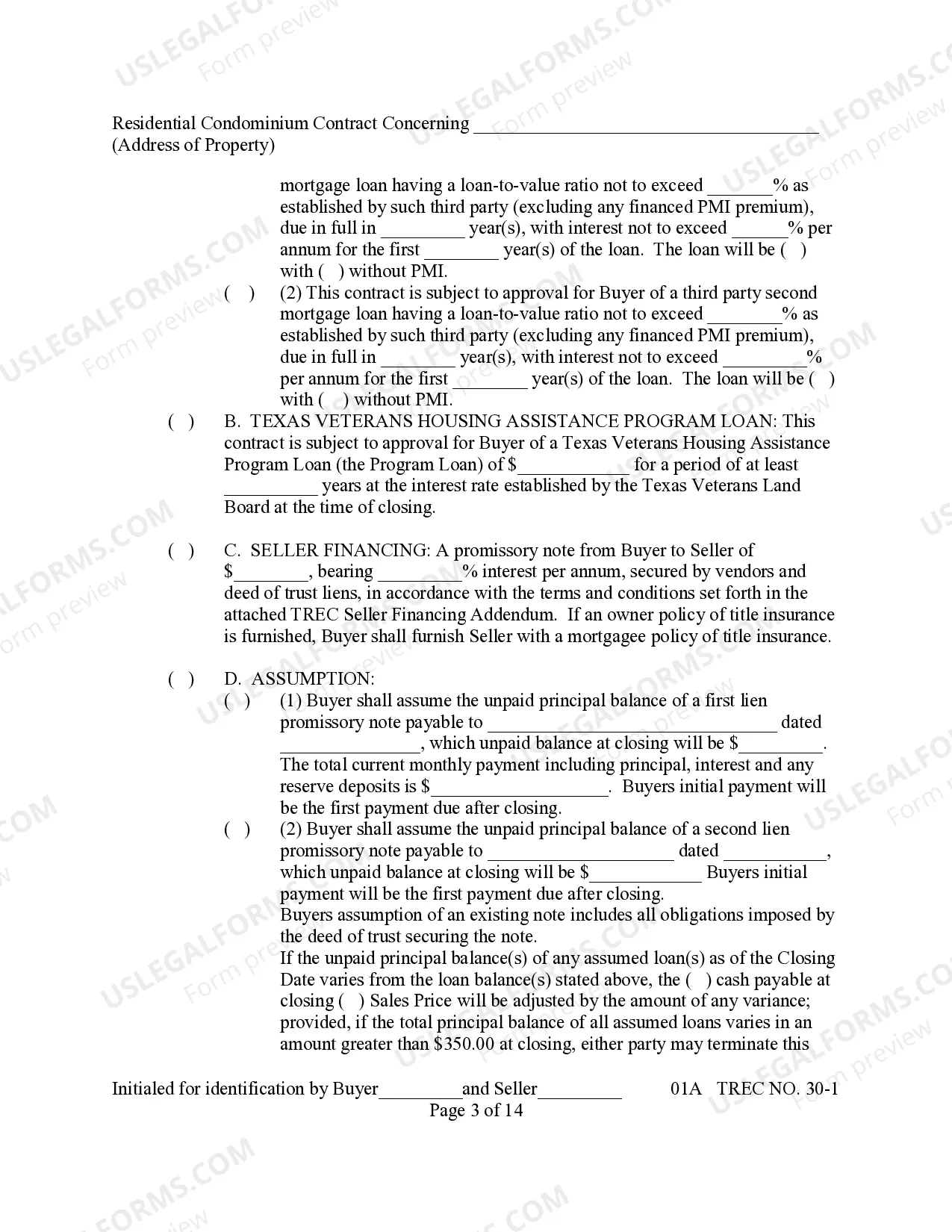

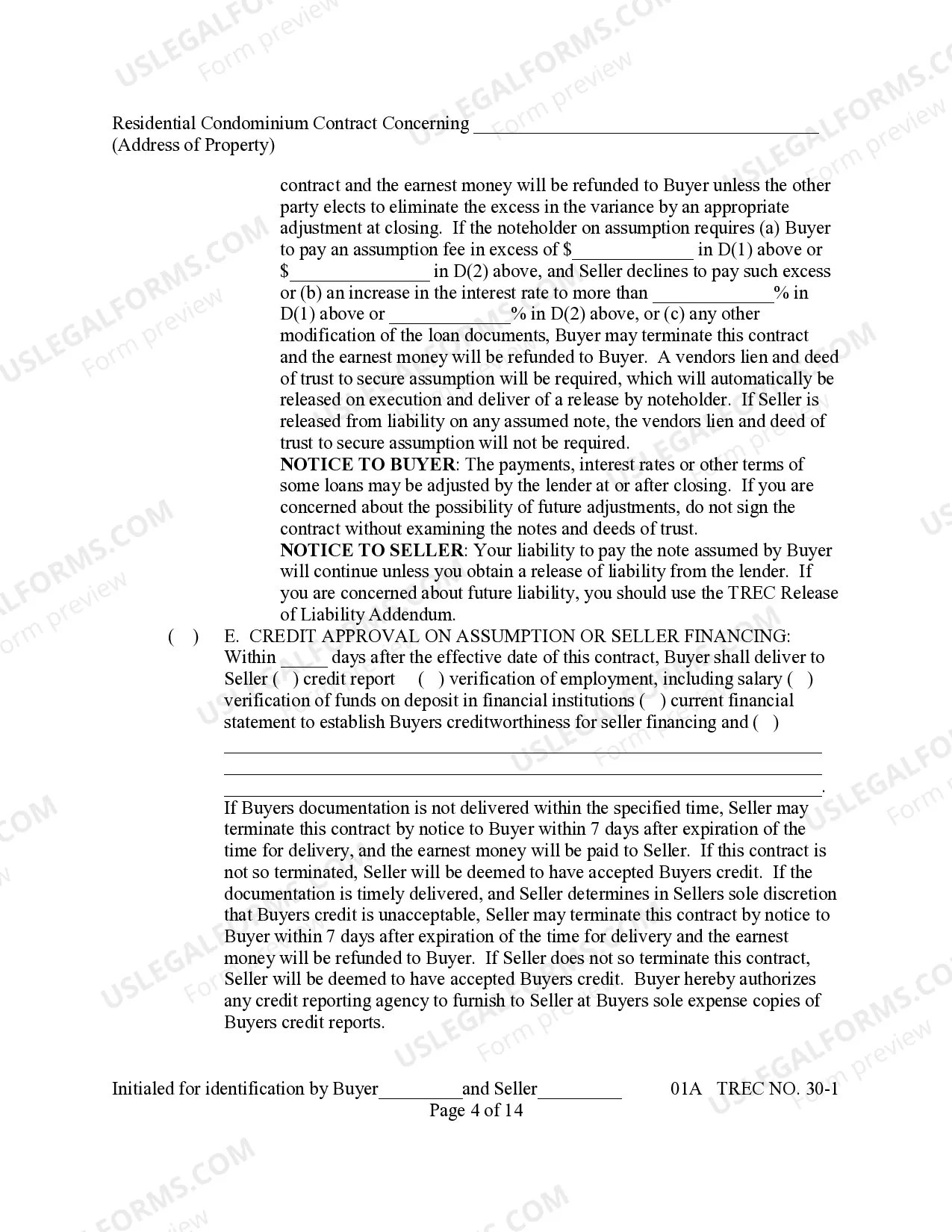

This detailed sample Conventional or Seller Financing Agreementcomplies with Texas law. Adapt the language to fit your facts and circumstances. Available in Word and Rich Text formats.

Frisco Texas Conventional Financing, also known as traditional financing, constitutes a mortgage loan offered by a bank or financial institution that adheres to the lending standards set by the government-sponsored enterprises (Uses) such as Fannie Mae and Freddie Mac. This type of financing requires the borrower to meet specific creditworthiness criteria, a stable income, and make a down payment typically ranging from 3% to 20% of the purchase price. Frisco Texas, a vibrant city within the Dallas-Fort Worth metropolitan area, provides numerous opportunities for homebuyers to explore conventional financing options. Conventional financing in Frisco Texas offers various advantages, including competitive interest rates, flexible loan terms, and wider property options. Borrowers with a strong credit history and a stable income find it easier to qualify for conventional loans. Moreover, Frisco Texas's flourishing housing market, with a multitude of single-family homes, townhouses, and condominiums, makes conventional financing an attractive option for potential homeowners. On the other hand, Seller Financing in Frisco Texas, also known as owner financing or purchase money mortgage, is an alternative financing option where the seller carries the mortgage themselves instead of a bank or financial institution. In this scenario, the seller acts as the lender, providing financing to the buyer for the purchase of the property. This type of financing often benefits buyers who may find it challenging to secure a traditional mortgage due to credit issues, self-employment, or insufficient down payment. Seller Financing in Frisco Texas offers several advantages for both buyers and sellers. Buyers can benefit from more relaxed credit requirements, flexible down payment options, and potentially faster closing times. Sellers can attract a larger pool of potential buyers, earn interest on the loan, and potentially sell their property faster. This type of financing can be structured in various ways, such as a land contract, contract for deed, or promissory note, depending on the agreement between the buyer and seller. In Frisco Texas, there may be variations and hybrid options related to both conventional and seller financing. Some examples include lease-to-own agreements, where a portion of the monthly rent is credited towards the eventual purchase of the property, and assumable mortgages, where a buyer takes over the existing mortgage from the seller. Additionally, Frisco Texas may have specific programs or incentives available to help first-time homebuyers or individuals with low to moderate incomes access conventional financing or seller financing. In conclusion, Frisco Texas provides homebuyers with a range of financing options that include conventional financing, adhering to the lending standards set by Uses, and seller financing, where the seller acts as the lender. Both financing methods boast various advantages and may cater to different circumstances. It is essential for interested parties to thoroughly understand the terms, conditions, and implications of each financing option before making a decision.Frisco Texas Conventional Financing, also known as traditional financing, constitutes a mortgage loan offered by a bank or financial institution that adheres to the lending standards set by the government-sponsored enterprises (Uses) such as Fannie Mae and Freddie Mac. This type of financing requires the borrower to meet specific creditworthiness criteria, a stable income, and make a down payment typically ranging from 3% to 20% of the purchase price. Frisco Texas, a vibrant city within the Dallas-Fort Worth metropolitan area, provides numerous opportunities for homebuyers to explore conventional financing options. Conventional financing in Frisco Texas offers various advantages, including competitive interest rates, flexible loan terms, and wider property options. Borrowers with a strong credit history and a stable income find it easier to qualify for conventional loans. Moreover, Frisco Texas's flourishing housing market, with a multitude of single-family homes, townhouses, and condominiums, makes conventional financing an attractive option for potential homeowners. On the other hand, Seller Financing in Frisco Texas, also known as owner financing or purchase money mortgage, is an alternative financing option where the seller carries the mortgage themselves instead of a bank or financial institution. In this scenario, the seller acts as the lender, providing financing to the buyer for the purchase of the property. This type of financing often benefits buyers who may find it challenging to secure a traditional mortgage due to credit issues, self-employment, or insufficient down payment. Seller Financing in Frisco Texas offers several advantages for both buyers and sellers. Buyers can benefit from more relaxed credit requirements, flexible down payment options, and potentially faster closing times. Sellers can attract a larger pool of potential buyers, earn interest on the loan, and potentially sell their property faster. This type of financing can be structured in various ways, such as a land contract, contract for deed, or promissory note, depending on the agreement between the buyer and seller. In Frisco Texas, there may be variations and hybrid options related to both conventional and seller financing. Some examples include lease-to-own agreements, where a portion of the monthly rent is credited towards the eventual purchase of the property, and assumable mortgages, where a buyer takes over the existing mortgage from the seller. Additionally, Frisco Texas may have specific programs or incentives available to help first-time homebuyers or individuals with low to moderate incomes access conventional financing or seller financing. In conclusion, Frisco Texas provides homebuyers with a range of financing options that include conventional financing, adhering to the lending standards set by Uses, and seller financing, where the seller acts as the lender. Both financing methods boast various advantages and may cater to different circumstances. It is essential for interested parties to thoroughly understand the terms, conditions, and implications of each financing option before making a decision.