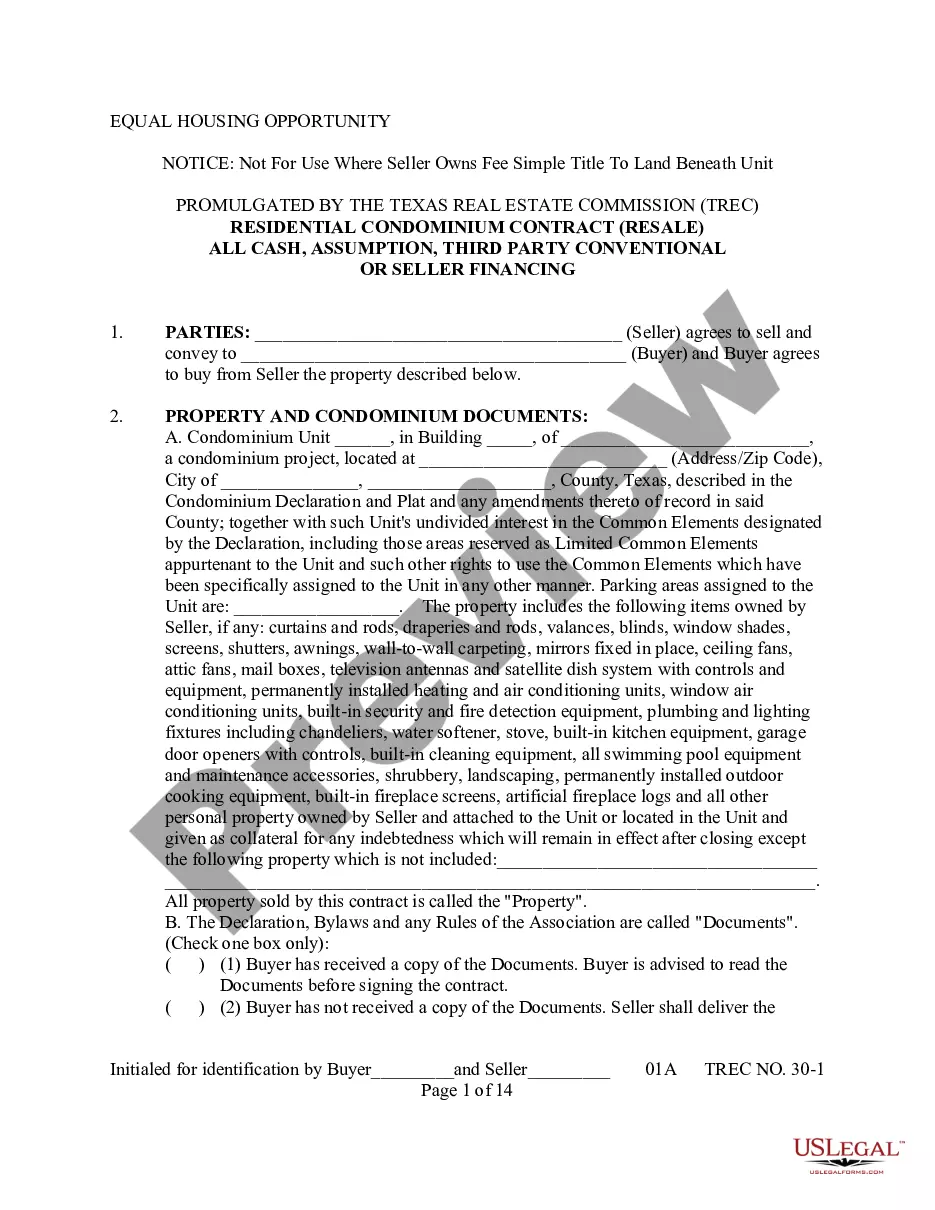

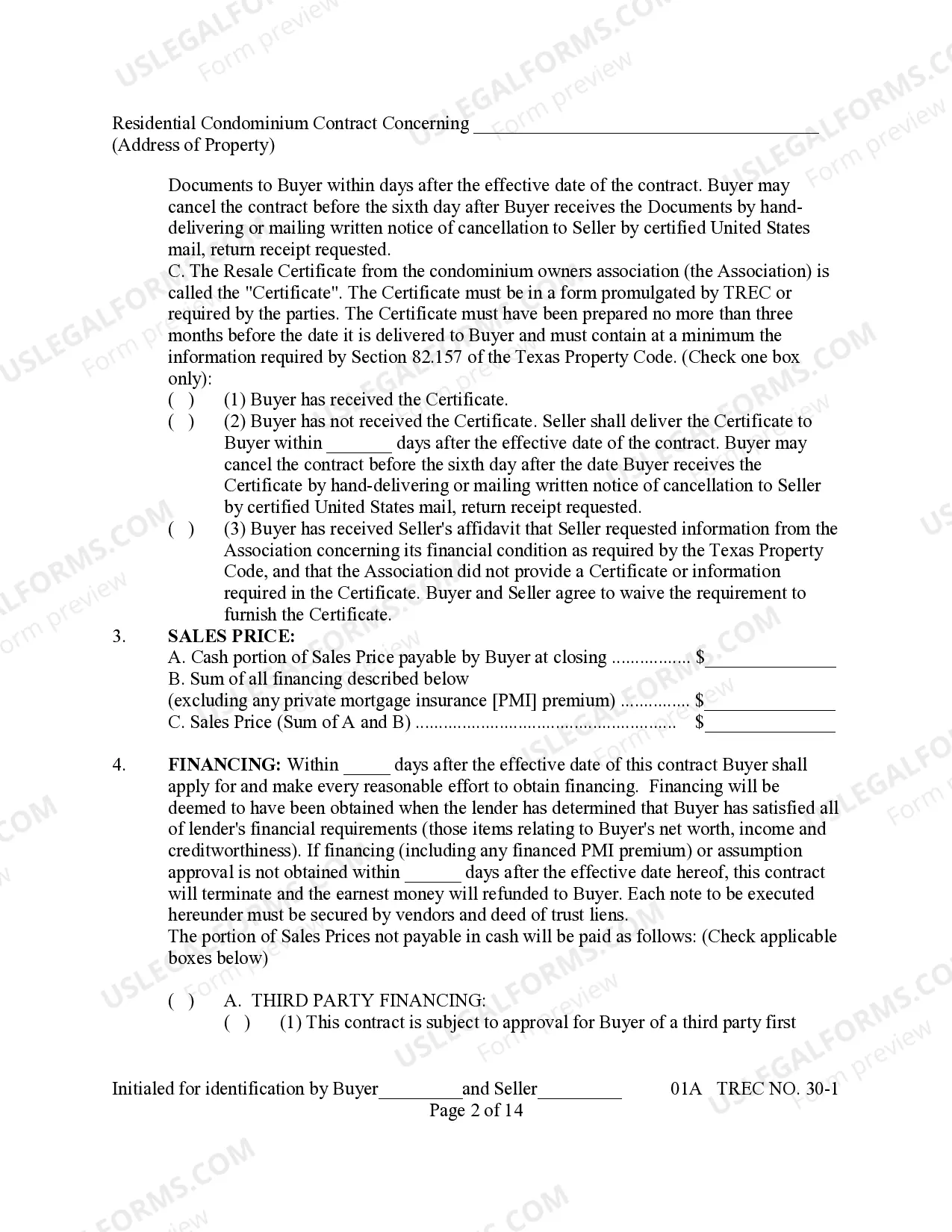

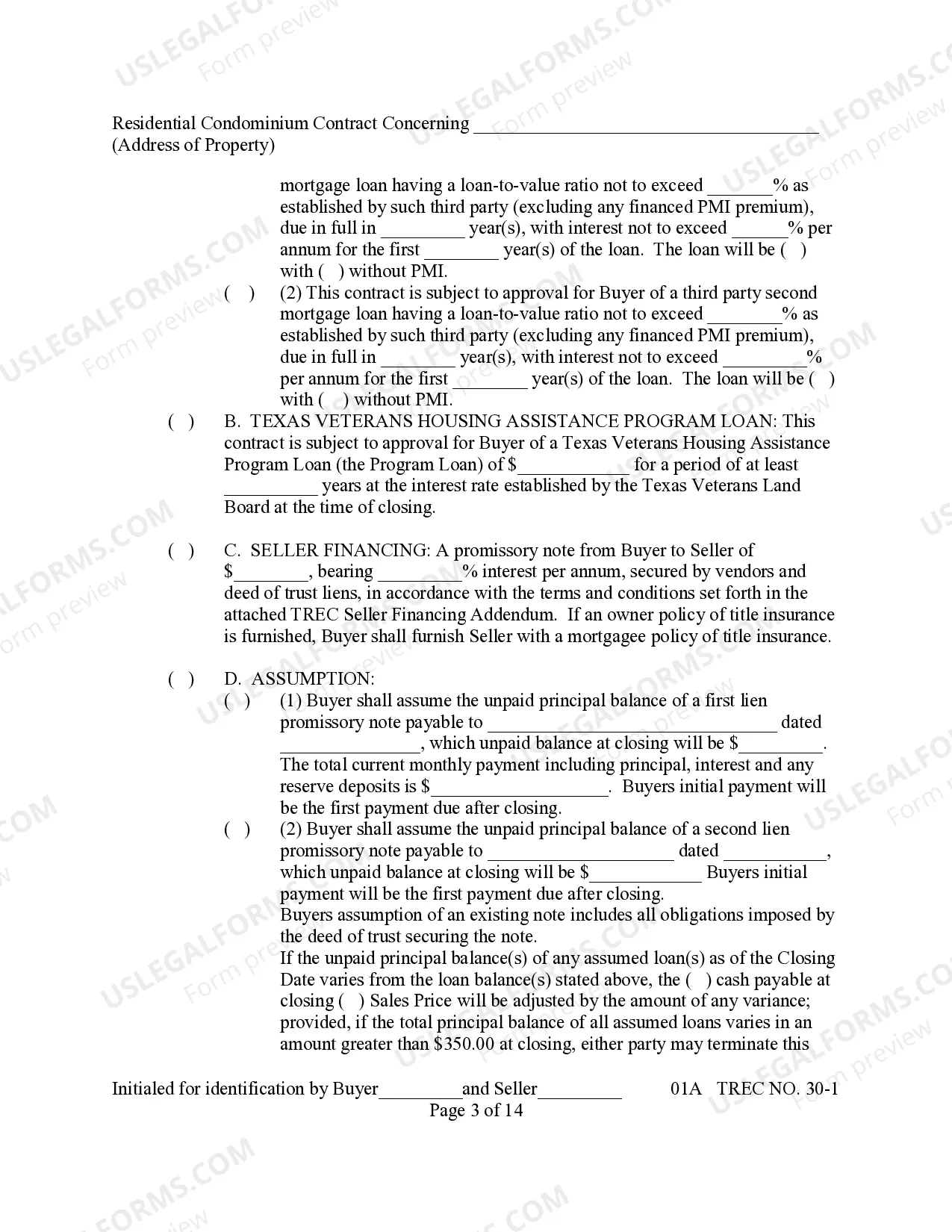

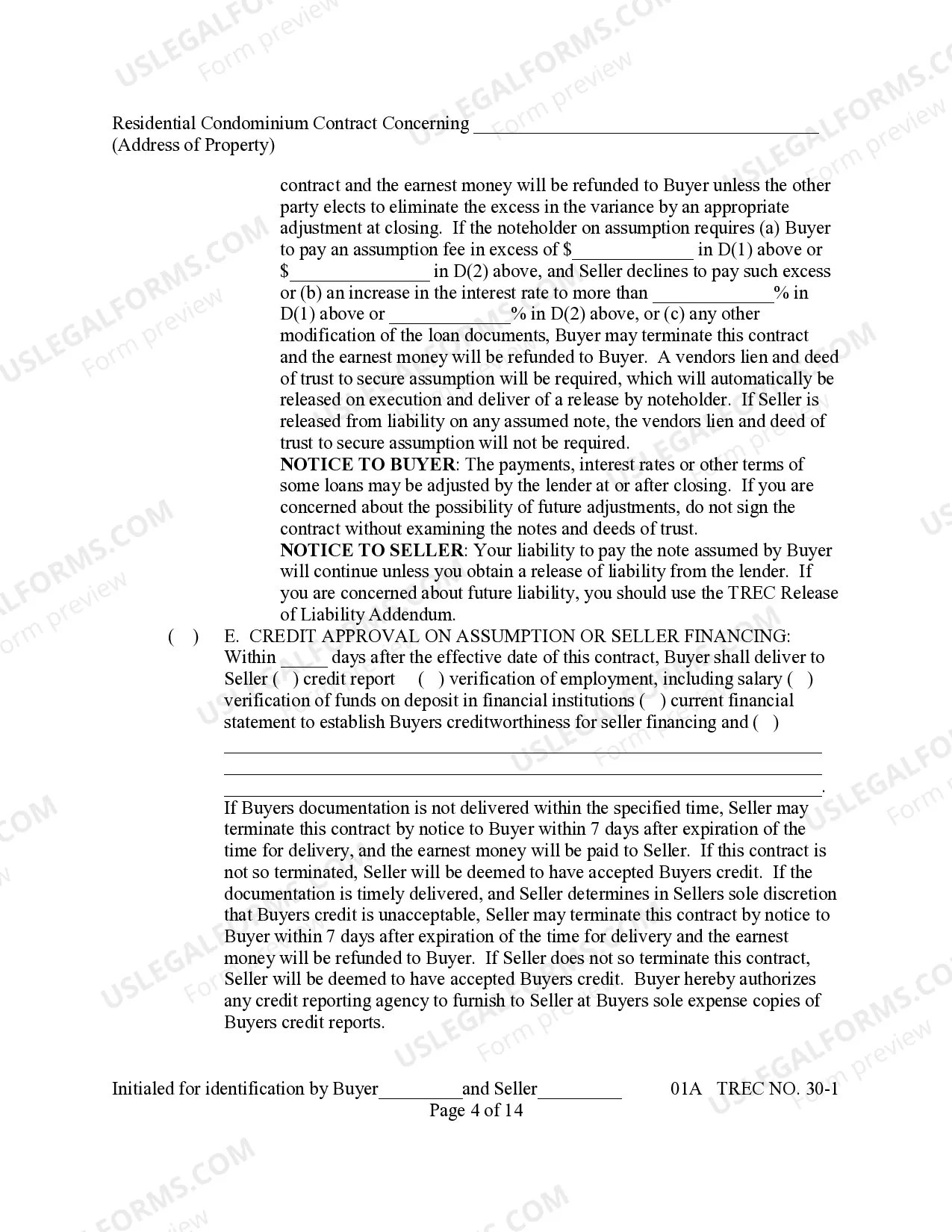

This detailed sample Conventional or Seller Financing Agreementcomplies with Texas law. Adapt the language to fit your facts and circumstances. Available in Word and Rich Text formats.

Mesquite Texas Conventional or Seller Financing: A Comprehensive Guide In the bustling city of Mesquite, Texas, there are various financing options available for potential homebuyers. Two popular methods are conventional financing and seller financing, each offering distinct advantages and considerations. This detailed description aims to shed light on these financing options and provide valuable insights to help buyers make informed decisions. Conventional Financing in Mesquite, Texas: Conventional financing refers to mortgage loans that are not insured or guaranteed by any governmental entity. These loans are originated and serviced by traditional lending institutions such as banks, credit unions, or mortgage companies. Conventional financing is based on a borrower's creditworthiness, income stability, employment history, and down payment capability. Key Features of Conventional Financing: 1. Credit Score: For conventional loans, generally a credit score of 620 or higher is required to qualify. However, some lenders may require a higher score for lower interest rates or more favorable terms. 2. Down Payment: Most conventional loans require a minimum down payment of 20% of the home's purchase price. However, there are loan programs available that allow for smaller down payments, such as 3% or 5% for first-time homebuyers. 3. Mortgage Insurance: If the down payment is less than 20%, private mortgage insurance (PMI) is typically required. PMI provides protection to the lender in case of default. 4. Loan Limits: In Mesquite, Texas, the conforming loan limit for conventional financing is $548,250 as of 2021. Borrowers seeking loans above this amount would be considered for jumbo loans. Seller Financing in Mesquite, Texas: Seller financing, also known as owner financing or purchase money mortgage, occurs when the property owner acts as the lender. In this arrangement, the seller holds a mortgage and receives monthly payments from the buyer instead of the buyer obtaining a loan from a traditional financial institution. Types of Seller Financing Options: 1. Contract for Deed/Land Contract: In this type of seller financing, the buyer agrees to make payments directly to the seller, who retains legal ownership until the terms of the contract are fulfilled. Once the agreement is complete, the seller transfers the property title to the buyer. 2. Lease Option: With a lease-option agreement, the buyer leases the property from the seller for a specific period, typically with an option to purchase at a later date. A portion of the monthly lease payment is often credited toward the purchase price. 3. Seller Carry back Mortgage: In such an arrangement, the seller acts as the lender, extending credit to the buyer. The buyer makes monthly payments that include principal and interest directly to the seller, who holds a mortgage on the property until it is paid off. 4. Wraparound Mortgage: This type of seller financing involves the buyer assuming the seller's existing mortgage while also receiving a second mortgage from the seller to cover the difference between the loan balance and the purchase price. Benefits and Considerations: — Conventional financing provides buyers with a wide range of loan options, access to competitive interest rates, and potential tax benefits. — Seller financing offers more flexibility, especially for those who have difficulty obtaining a traditional mortgage due to credit or financial constraints. — However, buyers considering seller financing should be cautious and conduct due diligence, such as verifying property title and examining the terms of the agreement. In conclusion, Mesquite, Texas, provides potential homeowners with multiple financing options. Conventional financing provides the benefits of traditional lending, while seller financing offers more flexibility. Understanding the key features and considerations of each option will help buyers make an informed decision that aligns with their financial goals and circumstances.Mesquite Texas Conventional or Seller Financing: A Comprehensive Guide In the bustling city of Mesquite, Texas, there are various financing options available for potential homebuyers. Two popular methods are conventional financing and seller financing, each offering distinct advantages and considerations. This detailed description aims to shed light on these financing options and provide valuable insights to help buyers make informed decisions. Conventional Financing in Mesquite, Texas: Conventional financing refers to mortgage loans that are not insured or guaranteed by any governmental entity. These loans are originated and serviced by traditional lending institutions such as banks, credit unions, or mortgage companies. Conventional financing is based on a borrower's creditworthiness, income stability, employment history, and down payment capability. Key Features of Conventional Financing: 1. Credit Score: For conventional loans, generally a credit score of 620 or higher is required to qualify. However, some lenders may require a higher score for lower interest rates or more favorable terms. 2. Down Payment: Most conventional loans require a minimum down payment of 20% of the home's purchase price. However, there are loan programs available that allow for smaller down payments, such as 3% or 5% for first-time homebuyers. 3. Mortgage Insurance: If the down payment is less than 20%, private mortgage insurance (PMI) is typically required. PMI provides protection to the lender in case of default. 4. Loan Limits: In Mesquite, Texas, the conforming loan limit for conventional financing is $548,250 as of 2021. Borrowers seeking loans above this amount would be considered for jumbo loans. Seller Financing in Mesquite, Texas: Seller financing, also known as owner financing or purchase money mortgage, occurs when the property owner acts as the lender. In this arrangement, the seller holds a mortgage and receives monthly payments from the buyer instead of the buyer obtaining a loan from a traditional financial institution. Types of Seller Financing Options: 1. Contract for Deed/Land Contract: In this type of seller financing, the buyer agrees to make payments directly to the seller, who retains legal ownership until the terms of the contract are fulfilled. Once the agreement is complete, the seller transfers the property title to the buyer. 2. Lease Option: With a lease-option agreement, the buyer leases the property from the seller for a specific period, typically with an option to purchase at a later date. A portion of the monthly lease payment is often credited toward the purchase price. 3. Seller Carry back Mortgage: In such an arrangement, the seller acts as the lender, extending credit to the buyer. The buyer makes monthly payments that include principal and interest directly to the seller, who holds a mortgage on the property until it is paid off. 4. Wraparound Mortgage: This type of seller financing involves the buyer assuming the seller's existing mortgage while also receiving a second mortgage from the seller to cover the difference between the loan balance and the purchase price. Benefits and Considerations: — Conventional financing provides buyers with a wide range of loan options, access to competitive interest rates, and potential tax benefits. — Seller financing offers more flexibility, especially for those who have difficulty obtaining a traditional mortgage due to credit or financial constraints. — However, buyers considering seller financing should be cautious and conduct due diligence, such as verifying property title and examining the terms of the agreement. In conclusion, Mesquite, Texas, provides potential homeowners with multiple financing options. Conventional financing provides the benefits of traditional lending, while seller financing offers more flexibility. Understanding the key features and considerations of each option will help buyers make an informed decision that aligns with their financial goals and circumstances.